thmTheorem \newtheoremreplemmaLemma \newtheoremrepconjectureConjecture \newtheoremreppropProposition \newtheoremrepcorCorollary \newtheoremrepexampleExample

Bounds and Heuristics for Multi-Product Personalized Pricing

Abstract

We present tight bounds and heuristics for personalized, multi-product pricing problems. Under mild conditions we show that the best price in the direction of a positive vector results in profits that are guaranteed to be at least as large as a fraction of the profits from optimal personalized pricing. For unconstrained problems, the fraction depends on the factor and on optimal price vectors for the different customer types. For constrained problems the factor depends on the factor and a ratio of the constraints. Using a factor vector with equal components results in uniform pricing and has exceedingly mild sufficient conditions for the bound to hold. A robust factor is presented that achieves the best possible performance guarantee. As an application, our model yields a tight lower-bound on the performance of linear pricing relative to optimal personalized non-linear pricing, and suggests effective non-linear price heuristics relative to personalized solutions. Additionally, our model provides guarantees for simple strategies such as bundle-size pricing and component-pricing with respect to optimal personalized mixed bundle pricing. Heuristics to cluster customer types are also developed with the goal of improving performance by allowing each cluster to price along its own factor. Numerical results are presented for a variety of demand models that illustrate the tradeoffs between using the economic factor and the robust factor for each cluster, as well as the tradeoffs between using a clustering heuristic with a worst case performance of two and a machine learning clustering algorithm. In our experiments economically motivated factors coupled with machine learning clustering heuristics performed best.

1 Literature Review and Summary of Contributions

Studies of pricing and demand estimation go back to 17th century Davenant (1699) with significant work done in the 19th century by Cournot (1838) and others economists of that era. Optimal pricing continues to attract researchers and practitioners to develop a deeper understanding and make price optimization more practical. Personalized pricing, a form of third degree price discrimination has emerge as more data is available, computing power becomes cheaper, and more transactions are done electronically enabling firms to charge different prices to different customer types. One key question is how much better is personalized pricing over non-personalized pricing. Another is to develop practical heuristics that perform well in practice and have a tight worst-case performance guarantee relative to more sophisticated pricing policies.

For the single product case, Bergemann et al. (2020) present a worst case bound of two for the ratio of personalized to uniform pricing, when the profit function for each customer type is concave and the demand functions take positive values over a common compact set. Malueg and Snyder (2006) under more mild assumptions obtain a bound equal to number of types. Elmachtoub et al. (2020) obtains tight and robust bounds that depends on summary statistics of the aggregate demand distribution. Gallego and Topaloglu (2019) provide bounds and heuristics for specific families of demand distributions including linear, exponential and logistic demand functions. They also include robust procedures to cluster customers types. Chen et al. (2019) present results for single-product distribution-free pricing.

In this paper we provide bounds and heuristics for the multi-product pricing problem including bounds for optimal pricing under a single factor (with uniform pricing as a special case) and show how our results can be used to bound the performance of linear-pricing versus non-linear pricing for the single product case. Our work can be seen as a generalization of results in Berbeglia and Joret (2020) that provide performance guarantee of uniform pricing for a subset of multi-product demand pricing problems known as envy-free pricing. Besides extending the performance guarantees of uniform pricing to a much broader class of single factor models, and to linear versus non-linear pricing, our performance guarantees are also stronger because they hold with respect to the optimal personalized pricing profit rather than the optimal non-personalized profit.

2 Single Factor versus Personalized Pricing

Consider a firm with products and customers types. Let denote the demand for product for customer type at price vector . We assume that all demand functions are non-negative. The profit function333After a simple transformation and if there is a non-zero unit cost vector . for type customers is given by . Denote by the maximum profit for type customers and let be distribution of the customer types, so . Then is the optimal profit from personalized pricing, also known as third-degree price discrimination. Let be the profit over all types at price and let . We will refer to as the optimal profit from non-personalized pricing. Solving for may be difficult even when solving for is easy. This is because the aggregate demand function may be significantly more complex than the underlying demands for the customer types. As a result, heuristics are often used. Here we consider a class of single factor heuristics (or pricing policies) where pricing is done along a positive vector , with . This is a single dimensional optimization problem that can be solved numerically. Notice that , the vector of ones, results in the uniform pricing policy with the optimal profit under uniform pricing. Clearly with equality holding if . Several questions arise from this setting, including finding tight bounds of the form (1) that provide performance guarantees for simple heuristics (including uniform pricing) for non-personalized pricing, or (2) to assess the benefit of personalized over non-personalized pricing. While both of these questions have been partially answered for specific pricing models, no tight bounds of type (1) and (2) are known for general pricing models with more than one product. To answer these questions simultaneously we will provide a tight upper-bound of the form which implies the former bounds on account of .

Brief preview our results: Let be an optimal price vector for type . If there are positive scalers and a such that for all , then under mild conditions . For the special case , if for some , then . A sufficient condition for is that the products are week substitute and have the connected substitute property for each , see Berry et al. (2013). The bounds work verbatim if prices are constrained to the stated intervals.

Assumption 0 (A0): We assume that optimal prices are positive and finite.

Assumption 0 (A0) holds for virtually all practical pricing problems as few firms price their goods at zero when optimizing profits and there is no demand at infinite prices. In our analysis we will first obtain a bound for the unconstrained case assuming that we are able to solve the pricing problem for each market segment. We then consider the case where prices are constrained to compact sets of the form for exogenously given .

Let is a vector of optimal prices for . Define if and otherwise. Let be the vector with components and consider

Then is the -weighted demand at the personalized optimal solution filtering out combinations for which , so some combinations are dropped as increases. On the other hand consider

be the -weighted demand at price vector . We are now ready to state our main assumption:

Assumption 1 (A1): for all .

For any given , the LHS of A1 accumulates the -weighted demands at optimal personalized pricing for combinations with whereas the RHS is the -weighted demand over all products and market segments at price vector . In many cases the inequality holds even if we filter terms on the right hand side by . Later we will provide sufficient conditions for A1, but we state here the weaker A1 to highlight the generality of our results.

To gain intuition of how this inequality will be used, define for and notice that . Multiplying by and adding over we conclude that . Notice that for all and for all , where and . This implies that

Finally, notice that . We are now ready to state our main result. {thm} Suppose that A0 and A1 hold. Then where . Moreover, the bound is tight.

Proof.

where the first equality follows form for ; the first inequality follows from due to A1. The second inequality follows from .

We now address the tightness of the bound. Suppose there are a continuum of types with willingness to pay in the interval for some . Assume that tail of the distribution of types is given by over with and , so that it integrates to one. Then, personalized pricing results in expected profit , so . For uniform pricing, any price in the interval is optimal, resulting in expected profit . Clearly so the bound is tight.

∎

Suppose the firm imposes the constraint for exogenously given , and for some . If A0-A1 hold then where is the maximum personalized profit subject to the stated constraints and is the optimal price along constrained to .

Proof.

The result follows directly from Theorem 2 since resulting in . Consequently . ∎

We remark that Theorem 1 also holds for continuous customer types as long as is bounded away from zero and is finite. Slightly sharper bounds can be obtained if the set of allowable prices is a finite set bounded away from zero. As an example, if with strictly decreasing in , we obtain where for convenience we set . It is also possible to prove that the sharpened bound is tight regardless of the number of customer types. The proof follows the same logic replacing sums with integrals and changing the order of summation and is omitted for brevity.

The following two properties are sufficient conditions for A.

-

P1

is increasing444We use the terms increasing and decreasing in the weak sense unless otherwise stated. in for all , for all .

-

P2

is decreasing in for all and all .

We remark that A1 need only hold at so conditions P1 and P2 are much stronger than needed. If , then P1 and P2 together state that the products are weak substitutes and have the connected substitute property, see Berry et al. (2013). These properties are satisfied by most pricing models studied in the literature including linear demand models, MNL models, Exponomial choice models (Alptekinoğlu and Semple, 2016), envy-free pricing models (Rusmevichientong et al., 2006) and any mixture of them. Moreover, P1 and P2 are also satisfied in pricing models for which even finding a price vector that guarantees some (positive) constant fraction of the optimal non-personalized profit is -hard555Consider a demand model where each customer type has a preference list. Assume further that consumers remove product from the list if its price is higher than , and then select their top choice from the remaining products, if any. This model satisfies P1 and P2 for and it is equivalent to an assortment optimization problem in which is the profit for product . Thus, the strongest negative result to date about the inapproximability of assortment optimization (-hardness to approximate to within a factor of for every (Aouad et al., 2018)) carries over to the pricing models studied in this paper.. If is differentiable in for all , then the aggregate demand is also differentiable. Then P2 implies that where is the Jacobian matrix. By P1, for all , so together P1 and P2 imply that is a P-matrix. As a result, its inverse exists and is non-negative and the demand function is injective. For a given we can transform the demand function via and one can verify that the test of weak substitution and connected substitute properties are are equivalent to P1 and P2 above. Details of the proof can be found in the Appendix.

We next show how to construct reasonable choices of when is hard to find and the firm knows . An economically motivated choice is with weights . For such , is called the Economic single factor profit. While the economic factor works well in practice, it does not minimize among all possible vectors . To find a robust , let , . Define the robust factor by , and the Robust single factor profit by . Let , and .

. Moreover, is attained by .

Proof.

Let be any positive vector. Then for any

Since this holds for all , it follows that . We next show that is attained by . By construction, with the two bounds attained. Consequently, , and and . Clearly the product that attains the maximum in also attains the minimum in , so . ∎

3 Clustering Consumer Types

Suppose that is large and the price vectors are dissimilar resulting in a large and therefore a poor performance guarantee. The firm can potentially improve the worst case performance if it can partition into collectively exhaustive and mutually exclusive clusters, so . We have already dealt with the case , while corresponds to personalized pricing. The problem is interesting for .

For a given partition, and a given positive vector for cluster , the worst case performance is where is the corresponding worst case ratio for cluster and factor and is the minimal ratio corresponding to the robust factor for cluster . More formally, , where , , and . We define the clustering problem as finding a partition to .

This problem is known in the literature as that of minimizing the maximum inter-cluster distance in the context of graphs (Gonzalez, 1985) and also as the bottleneck problem (Hoschbaum and Shmoys, 1986). To see that equivalence, consider a graph with vertices for all and . There are edges between any two nodes that share the same product, say and . The distance between the two adjacent nodes in the network is given by . The reader can confirm that the maximum distance for a graph , is equal to , and that the distance satisfies the triangle inequality.

Fortunately, there is a 2-factor approximation polynomial time algorithm for this problem, which is the best possible unless , see Gonzalez (1985) and Hoschbaum and Shmoys (1986). We also used the -means clustering heuristic and compare their performance. We remark that once the clusters are formed, each cluster will price along a positive vector which may or may not be the robust choice for that cluster. This is because frequently the economic factor performs better than the robust factor even though the robust factor gives the best performance guarantee.

4 Applications

In this section we discuss several applications to our results, including linear demands, the latent class MNL, and Non-Linear Pricing.

4.1 Linear Demands

We first briefly review the representative consumer problem that results in the linear demand model. The task of the representative consumer is to solve the problem where is the vector of gross utilities, is the vector of net utilities, and is a positive definitive matrix. The solution that ignores the non-negativity constraints yields where and . Notice that by construction is symmetric and positive definitive. Let . We assume that has positive components. Then for all . Maximizing yields , and , so . For , the solution to the representative consumer’s problem is equivalent to solving the linear complementarity problem , , and , see Gallego and Topaloglu (2019).

Suppose that for all , for . where and are positive vectors, and is a symmetric positive definitive matrix. Then is in , and can be computed without problems.

Suppose that has non-positive off-diagonal elements for all . Then Therorem 2 holds for positive vectors such that for all . Moreover, if is an M-matrix for all then the Theorem 2 holds for all positive .

Proof.

From the assumptions of the corollary, P1 and P2 holds for all . Since P1 and P2 are sufficient for A1, the result of Theorem 2 hold. Moreover, if is an M-matrix then has positive components. This implies that the vector has positive components that can be made arbitrarily small, so for any vector positive vector we can find an such that have . Multiplying both sides by shows that . ∎

At this point we know that where and are interpreted as and where and . The caveat is that optimal solutions to this problems, say and , may be outside for some resulting in negative demands for some products for some customer types. This cast as question of whether the profits from pricing at or at will actually satisfy the guarantees of Theorem 2. We will show that and continue to hold even after the adjustments required to ensure that all demands are non-negative. To see this in a generic form, we will argue that the actual profit when has negative components is at least as large as . {prop} The profit under the representative consumer model is equal to when .

Proof.

The expected profit associated with a vector is given by where and . The complementary slackness condition can be written as . By the symmetry of , . The inequality follows from and since is positive definitive. ∎

We can now apply the result to each customer type that has negative demands at . In particular, if there is a customer type with negative demands at , then the firm will see profits from type customers, so is a lower bound on the aggregate profit over all customer types at . Consequently, the profit from the single factor model is at least . In a similar way, is a lower bound of the aggregate profits at , so the profit under is at least . One must be aware, however, that for multiple customer types, is not necessarily optimal if there are customer types with negative demands at this price vector. To find a true optimal solution to the problem the firm needs to solve subject to and for all . The solution together with the corresponding s that solve the linear complementarity problem for market segments with negative demands is only a heuristic for this problem, so our results continue to hold if the more complex problem is solved, with a similar more sophisticated program for pricing along a factor .

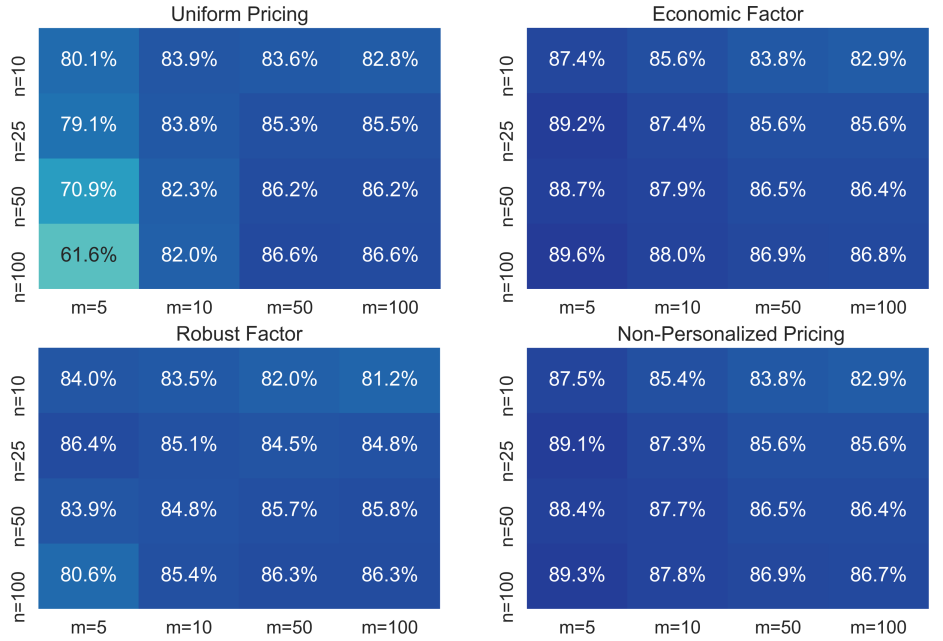

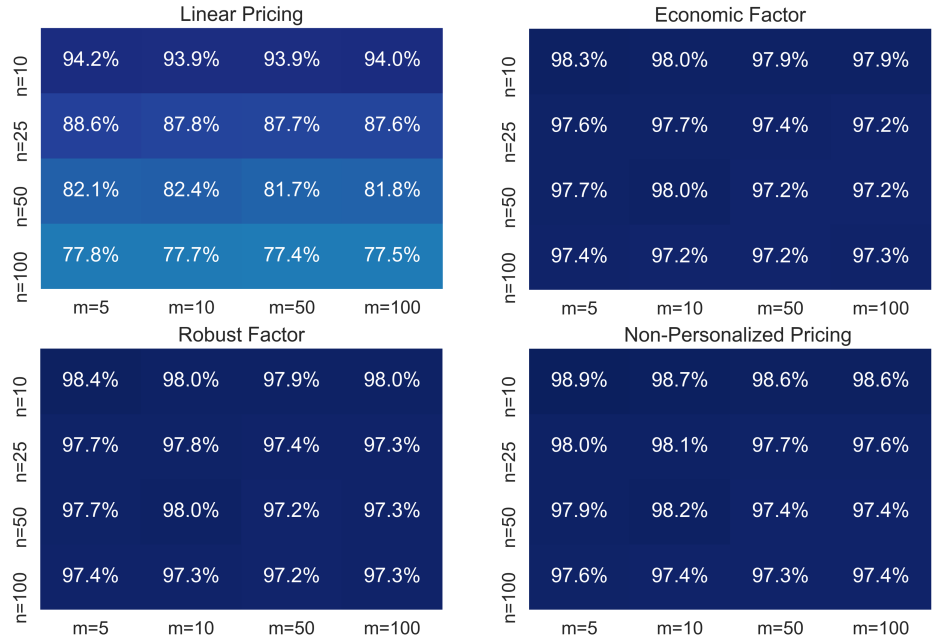

Figure 1 reports a series computational results in order to evaluate the performance of different pricing strategies. For each value of and , we generated 20 random instances and we reported the average profit as a percentage of the maximum profit that can be obtained using personalized pricing. The weight of each segment was set to where each is a uniform random number between 0 and 1. For each segment we randomly generated the matrix ensuring it is symmetric and positive definitive and satisfies P1 and P2. The vector was generated uniformly random from . The percentages shown are the average percentage of the profit obtained with respect to the best personalized pricing strategy. As we can see, the economic factor outperformed the robust factor, and both performed significantly better than uniform pricing based on . The lower right-hand table for the optimal price uses the heuristic adjusting demands by solving the complementary slackness for customer types with negative demands. It performance is similar to that of the economic factor.

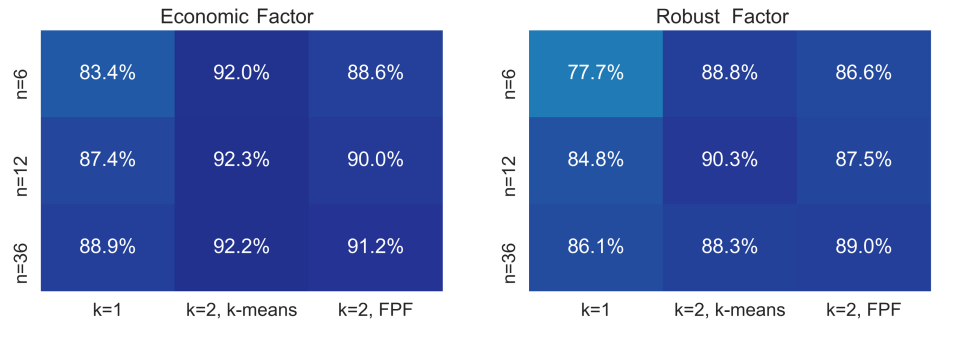

Figure 2 reports another set of experiments to quantify the advantages of clustering consumer segments into two clusters () under the economic and the robust pricing strategies. Two clustering algorithms were implemented. The first one is the standard k-means algorithm in which each segment was assigned the price vector as its representative point in an -dimensional space. The second is the farthest point first (FPF) proposed by gonzalez1985clustering where the distance matrix is set as described in Section 3. For these experiments the number of consumer segments was set to . As can be seen, the best combination was the economic factor coupled with -means and the worse was the robust factor with FPF.

4.2 Latent Class MNL

Suppose that is the expected demand from an MNL model, so

The matrix of partial derivatives is given by . Since the off-diagonal elements are non-negative we see that is increasing in and P1 holds. P2 hold for all positive vectors such that , or equivalently for all positive vectors such that for all . We can scale without loss of generality so that , which reduces the condition to . This clearly holds for on account of . For any positive the condition reduces to for all . We remark that A1 requires the condition to hold only at , for . We know that for each consumer type the optimal price is of the form where is the adjusted markup for product type consumers, so the condition is easy to check. In particular, if for each , and , then both the economic and the robust factors can be taken to be equal to .

For the LC-MNL without any further conditions since P1 and P2 hold for for all MNL models with arbitrary price sensitivities. In addition, if the is independent of for each , then the economic and the robust factors are equivalent to . Finally, holds for all positive vectors such that for all .

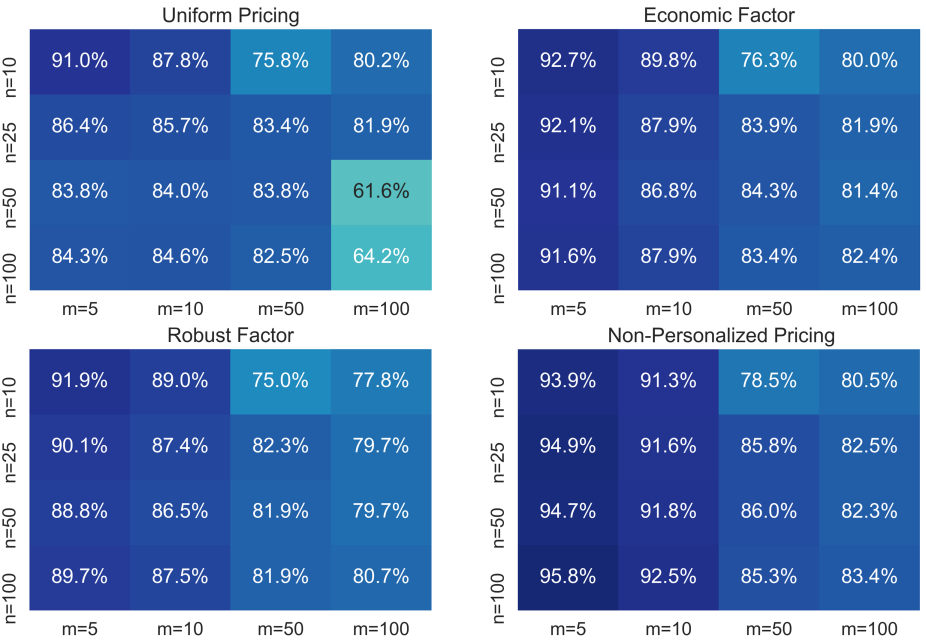

We tested the performance of the different heuristics under the LC-MNL model and reported the results in Figure 3. The percentages shown are the average percentage of the profit obtained with respect to the best personalized pricing strategy. For each value and value reported, we generated 20 random instances with products and segments. The mean utility of product to consumer segment is where the intrinsic product utility were randomly chosen following a procedure proposed by rusmevichientong2014assortment 666Specifically, the intrinsic utility of product for consumer segment is defined as with probability and otherwise. The values and are realizations from a uniform distribution and respectively. and the (segment and product dependent) price sensitivities were randomly chosen from a symmetric triangular distribution between 0 and 2. We can observe that while uniform pricing does relatively well (obtaining between 60.6% to 91% of the optimal personalized profit) it is surpassed by the Economic and Robust strategies with get at least 76.3% and 75% respectively. The values for the non-personalized pricing are not necessarily the optimal ones 777This is an NP-hard problem. since they were obtained using a multi-variable non-linear solver in Python. This strategy requires much broader computational resources than the other three methods which simply rely on a single variable optimization. For example, when the solver took on average over 22 times more time than any of the other 3 strategies.

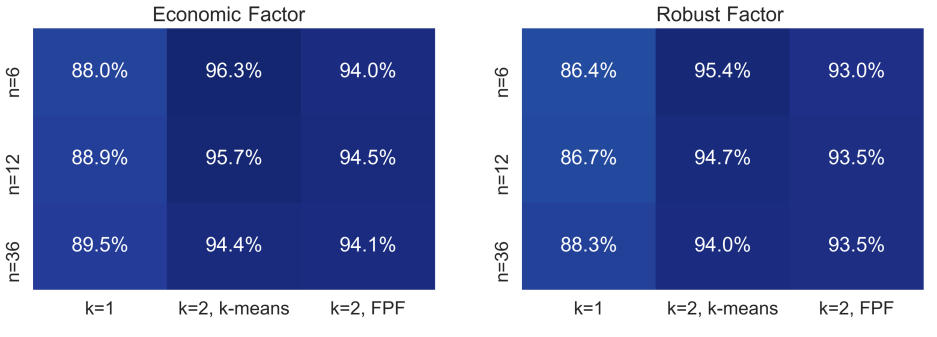

Similarly to the clustering results for the linear demand model, Figure 4 reports computational results that quantify and compare the benefits of clustering consumer segments using k-means and FPF under the Economic single factor and the Robust single factor pricing strategies. The values represent the average percentage of the profit obtained with respect to the best personalized pricing strategy. As in the linear demand model, for all these experiments. As can be seen, the best combination was the economic factor coupled with -means and the worse was the robust factor with FPF.

4.3 Linear Pricing Versus Non-Linear Personalized Pricing

We now consider the non-linear pricing scheme where the firm sells a single product in different bundle sizes- for a broad overview of non-linear pricing see wilson1993nonlinear and oren2012nonlinear. Let be the price of a size bundle and is the demand for a size bundle at the price vector . Let yielding an optimal non-linear price schedule. Let be a vector with components . Then corresponds to the linear price schedule . Theorem 2 holds if is increasing in , and if is decreasing in . We remark that is the total number of units demanded at price , so the condition is that the total number of units demanded goes down if the price of any bundle is increased.

As an example, suppose that and is an -matrix, then for all and in particular for . Let . Then . If is increasing concave then and resulting in .

To our knowledge this is the first result that gives a performance guarantee for linear versus non-linear pricing, but we can go further as Theorem 2 works for the personalized version as well. More precisely, if is the demand vector for bundles of size for every , is increasing in for all , and is decreasing in for all then Theorem 2 applies and bounds how much better personalized non-linear pricing can be relative to linear pricing. Theorem 2 can also be used to bound the performance of non-personalized non-linear pricing schemes relative to personalized non-linear pricing schemes. We summarize the results for personalized non-linear pricing here.

If represent the demand for bundles of size in market segment where is the price of a size bundle, is decreasing in and is decreasing in for all , then

where is the profit from the optimal non-personalized non-linear pricing policy and is the optimal under non-personalized linear pricing policy.

We remark that here was selected as for the purpose of comparing a common linear price schedule for all customer types to optimal personalized non-linear pricing. One can instead use the robust or the economic to obtain a potentially better common (non-linear) price schedule.

Figure 5 reports a computational results about the performance of different pricing strategies for a non-linear pricing problem as described above. Each consumer segment follows a linear model as explained in Section 4.1. The matrix associated to segment was generated in the same way as for the experiments of Section 4.1 whereas instead of generating a random vector , we produced a random vector of utilities satisfying that and for all . We generated 20 instances for each value of and each maximum bundle size (). As can be seen from the tables, linear pricing performance relatively well for but deteriorates as the maximum bundle size increases achieving only about 77% of optimal personalized non-linear pricing. The results do not seem to be sensitive to the number of customer types. The robust factor slightly outperforms the economic factor, and the non-personalized non-linear pricing strategy is very close to the optimal personalized strategy with little need for clustering types.

4.4 Bundle-size pricing as an approximation to mixed bundling

Consider a set of products that can be sold as bundles. Suppose that given prices for each of the non-trivial bundles, the firm can obtain the demand for each of the bundles. Selecting the bundle prices to maximize profits is know as the mixed bundle problem. Suppose that is an optimal solution to the mixed bundle problem. We may wonder about the performance of several pricing strategies relative to mixed bundling. The simplest strategy is to use uniform pricing. This gives rise to . A second strategy, known as component pricing is to set where is the price of component . Finally, we can have a non-linear function where is an increasing non-linear function. Notice this form yields the same price factor for all bundles of size . This is known as bundle-size pricing and contains uniform pricing as a special case if . In all cases, the firm will find and optimal for the pricing strategy for size bundles, ChenLeslieSoren2011bunde shows through extensive numerical studies that bundle-size pricing can do a good job of approximating the benefits of the more complicated mixed bundling strategy but to our knowledge there are no theoretical work on tight bounds. Let and . Under mild conditions on the demand function for bundles (A0 and A1, or A0 together with P1 and P2) we obtain performance guarantees where here is the optimal profit under mixed bundling and is the optimal pricing along the vector , where where . As an example, if then the non-trivial bundles are and where is the th unit vector in . If and and we use and for bundles of size 1 and 2, then and so and . The theory also holds if there are multiple types and the firm uses personalized mixed pricing for each type. The only difference is that the definition of and has to be over all bundles and all types. It is also possible to fit a robust or an economic mixed bundle strategy and as long as the conditions A0 and A1 hold the bound from Theorem 1 holds. If the model is linear or latent class MNL we will get similar numerical results with the exception that the bundles are interpreted as products and the vector is either the bundle size or either the economic or robust factor in the case of multiple market segments.

5 Conclusions and Future Research

This paper presents tight performance guarantees for multi-product single factor pricing relative to personalized pricing with applications to a variety of demand models. The results apply to , where is the demand vector for firm at price vector given that competitors offer price for their own goods provided A1 or P1 and P2 hold for fixed . This opens the door to study competition under a variety of pricing scenarios.

6 Appendix

Proof.

For convenience, we first consider the single customer type case dropping the index . Let and for and otherwise. Since , P2 implies that

The move from to decreases the price of products for which . By P1 this has a negative effect on the demand of products for which . Thus,

Consequently,

Moreover, moving from to decreases the prices of products for which , so by P1

Multiplying by , adding and collecting the inequalities we obtain

This completes the proof for a single customers type, and implies under the stated assumptions that

Multiplying by the weights and adding over yields which is A. ∎

Acknowledgements

We would like to thank Adam Elmachtoub, Pin Gao, Wentau Lu, Preston McAfee, Shmuel Oren, and Zhuodong Tang for their help and suggestions, as well as Daniel Aloise for pointing us to the minimax diameter clustering problem and the FPF heuristic used in this paper.

References

- Alptekinoğlu and Semple [2016] Aydın Alptekinoğlu and John H Semple. The exponomial choice model: A new alternative for assortment and price optimization. Operations Research, 64(1):79–93, 2016.

- Aouad et al. [2018] Ali Aouad, Vivek Farias, Retsef Levi, and Danny Segev. The approximability of assortment optimization under ranking preferences. Operations Research, 66(6):1661–1669, 2018.

- Berbeglia and Joret [2020] Gerardo Berbeglia and Gwenaël Joret. Assortment optimisation under a general discrete choice model: A tight analysis of revenue-ordered assortments. Algorithmica, 82(4):681–720, 2020.

- Bergemann et al. [2020] Dirk Bergemann, Francisco Castro, and Gabriel Y Weintraub. Uniform pricing versus third-degree price discrimination. Cowles Foundation Discussion Paper, 2020.

- Berry et al. [2013] Steven Berry, Ami Gandhi, and Phillip Haile. Connected substitutes and invertibility of demand. Econometrica, 81(5):2087–2111, 2013.

- Chen et al. [2019] Hongqiao Chen, Ming Hu, and Georgia Perakis. Distribution-free pricing. Available at SSRN 3090002, 2019.

- Chenghuan Sean Chu and Sorensen [2001] Phillip Leslie Chenghuan Sean Chu and Alan Sorensen. Bunndle-size pricing as an approximation to mixed bundling. The American Economic Review, 101(1):263–303, 2001.

- Cournot [1838] A. A. Cournot. Researches into the Mathematical Principles of the Theory of Wealth. The Macmillan Company, New York, 1838.

- Davenant [1699] C. Davenant. An essay upon the probable methods of making a people gainers in the balance of trade. James Knapton, London, 1699.

- Elmachtoub et al. [2020] Adam N Elmachtoub, Vishal Gupta, and Michael Hamilton. The value of personalized pricing. Management Science (forthcoming), 2020.

- Gallego and Topaloglu [2019] Guillermo Gallego and Huseyin Topaloglu. Revenue Management and Pricing Analytics. Springer Verlag, New York, NY, 2019.

- Gonzalez [1985] Teofilo F Gonzalez. Clustering to minimize the maximum intercluster distance. Theoretical Computer Science, 38:293–306, 1985.

- Hoschbaum and Shmoys [1986] D. S Hoschbaum and D. B Shmoys. A unified approach to approximation algorithms for bottleneck problems. J. ACM, 33, 1986.

- Malueg and Snyder [2006] David A Malueg and Christopher M Snyder. Bounding the relative profitability of price discrimination. International Journal of Industrial Organization, 24(5):995–1011, 2006.

- Oren [2012] Shmuel S Oren. Nonlinear pricing. In The Oxford Handbook of Pricing Management. 2012.

- Rusmevichientong et al. [2006] Paat Rusmevichientong, Benjamin Van Roy, and Peter W Glynn. A nonparametric approach to multiproduct pricing. Operations Research, 54(1):82–98, 2006.

- Rusmevichientong et al. [2014] Paat Rusmevichientong, David Shmoys, Chaoxu Tong, and Huseyin Topaloglu. Assortment optimization under the multinomial logit model with random choice parameters. Production and Operations Management, 23(11):2023–2039, 2014.

- Wilson [1993] Robert B Wilson. Nonlinear pricing. Oxford University Press on Demand, 1993.