Closed-form approximations in multi-asset market making

Abstract

A large proportion of market making models derive from the seminal model of Avellaneda and Stoikov. The numerical approximation of the value function and the optimal quotes in these models remains a challenge when the number of assets is large. In this article, we propose closed-form approximations for the value functions of many multi-asset extensions of the Avellaneda-Stoikov model. These approximations or proxies can be used (i) as heuristic evaluation functions, (ii) as initial value functions in reinforcement learning algorithms, and/or (iii) directly to design quoting strategies through a greedy approach. Regarding the latter, our results lead to new and easily interpretable closed-form approximations for the optimal quotes, both in the finite-horizon case and in the asymptotic (ergodic) regime.

keywords:

Algorithmic trading, Market making, Stochastic optimal control, Closed-form approximations, Monte-Carlo methods.MSC:

[2010] 91G99, 93E20, 91G60.1 Introduction

Since the publication of the paper [1] by Avellaneda and Stoikov, who revisited the paper [24] by Ho and Stoll (see also [25]), there has been an extensive literature on optimal market making.111There is an economic literature on market making, for instance the seminal paper [16] by Grossman and Miller. The results in this literature are, however, more interesting for understanding the price formation process than for building market making algorithms. Guéant, Lehalle, and Fernandez-Tapia provided in [20] a rigorous analysis of the stochastic optimal control problem introduced by Avellaneda and Stoikov and proved that, under inventory constraints, the problem reduces to a system of linear ordinary differential equations in the case of exponential intensity functions suggested by Avellaneda and Stoikov. They also studied the asymptotics when the time horizon tends to , proposed closed-form approximations, and introduced extensions to include a drift in the price dynamics and market impact / adverse selection. Cartea and Jaimungal, along with their various coauthors, contributed substantially to the literature and added many features to the initial models: alpha signals, ambiguity aversion, etc. (see [8, 10, 11] – see also their book [9]). They also considered a different objective function: the expected PnL minus a running penalty to avoid holding a large inventory instead of the Von Neumann-Morgenstern expected CARA (constant absolute risk aversion) utility of [1] and [20]. Many features have also been added by various authors: general dynamics for the price in [14], general intensities and partial information [7], persistence of the order flow in [26], several requested sizes in [5], client tiering and access to a liquidity pool in [4], etc.

In spite of the focus of initial papers on stock markets,222There was also from the very beginning a focus on options markets – see for instance [29] (cf. [2] and [12] for more recent papers). the models derived from that of Avellaneda and Stoikov have been more useful to build market making algorithms in quote-driven markets: corporate bond markets based on requests for quotes, FX markets based on requests for quotes and requests for stream, etc. For stock markets or, more generally, order-driven markets with relatively low bid-ask spread to tick size ratio, many models have been proposed that depart from the original framework of Avellaneda and Stoikov in that the limit order book is modeled. Instances of papers proposing this type of models include those of Guilbaud and Pham [22, 23], that of Kühn and Muhle-Karbe [27], that of Fodra and Pham [15] or the more recent papers by Lu and Abergel [28] and Baradel, Bouchard, Evangelista, and Mounjid [3].

Most of the literature on optimal market making deals with single-asset models. However, because market making algorithms are typically built for entire portfolios, single-asset models are not sufficient to build operable algorithms, except under the unrealistic assumption that asset prices are uncorrelated. Multi-asset extensions of the Avellaneda-Stoikov model have been proposed. A paper by Guéant and Lehalle [19] touches upon this extension and a complete analysis for the various objective functions present in the literature can be found in [18] (see also the book [17]) or in [5] in which multiple trade sizes are also considered.

Although their mathematical characterization has been known for years, computing the value function and the optimal quotes is complicated in the multi-asset case whenever the prices of the assets are correlated. The grid methods that are classically used to tackle the single-asset case suffer indeed from the curse of dimensionality and do not scale up to many practical multi-asset cases. Bergault and Guéant proposed in [5] a factor method to reduce the dimensionality of the problem. Guéant and Manziuk proposed in [21] a numerical method based on reinforcement learning techniques (an actor-critic approach in fact). In spite of these recent advances, the computational cost of most numerical schemes will still be prohibitive for practical use for some asset classes.

Instead of computing a numerical approximation of the value function (from which one traditionally deduces a numerical approximation of the optimal quotes), we propose in this paper a method for building a closed-form proxy for the value function. The idea behind the approach is that the value function associated with many market making problems is the solution of a Hamilton-Jacobi equation that can be “approximated” by another Hamilton-Jacobi equation for which the solution can be computed in closed form. Of course, such closed-form formula does not define a solution to the initial Hamilton-Jacobi equation, but it has similar properties and should capture most of the relevant financial effects.

Having a proxy of a value function is known to be useful in the community of reinforcement learning (see [30] and [31] for a reference to the reinforcement learning terminology). An important use of a closed-form proxy of a value function is as a heuristic evaluation function. Heuristic evaluation functions are mainly used in game-playing computer programs to evaluate the probability to win the game given the current state – usually the current board in board games – but they can be used as terminal values in many Monte-Carlo-based reinforcement learning techniques. Also, such a proxy can be used as a starting point for many iterative algorithms based on value functions: value iteration algorithm, actor-critic approaches, etc. The last application we highlight – which was also our initial motivation – is that one can build from a proxy of a value function a quoting strategy by using what is called in the reinforcement literature the greedy strategy associated with that proxy (i.e. the strategy that makes the locally optimal choice if at each time step the value function associated with the tail problem is replaced by its proxy in the dynamic programming equation). Having such a strategy in closed form has numerous advantages. First, it can be used directly by market practitioners as a quoting strategy. Second, it can be used as a starting point in iterative algorithms based on policy functions: policy iteration algorithm, actor-critic approaches, etc. Third, it has the advantage of being easily interpretable and gives insights on the true optimal strategy such as the identification of the leading factors and the sensitivity to changes in model parameters.333For market making, the influence of the parameters has already been studied in [20] (one-asset case) and [18] (multi-asset case).

The method we propose is first applied to the multi-asset market making models of [18]. Then we generalize the framework in several directions to cover many important practical cases: (i) drift in prices, (ii) client tiering, (iii) several request sizes for each asset and each tier, and (iv) fixed transaction costs for each asset and each tier. The drift in prices models the views of the market maker. Client tiering is a common practice in OTC markets, justified by the large spectrum of needs and behaviors in the set of clients to be served. The introduction of several request sizes for each asset and each tier reflects the reality that request sizes are not in control of the market makers, but rather of their clients. The fixed transaction costs can model extra costs associated with the market making business, for instance related to trading platforms.

We end this introduction by outlining our paper. In Section 2 we recall the multi-asset extensions of the Avellaneda-Stoikov model proposed in [18], present the system of ordinary differential equations (the Hamilton-Jacobi equation) characterizing the value function, and state the main results regarding the optimal quotes. In Section 3, we present our approach and compute a closed-form proxy for the value function. We deduce from that proxy an approximation of the optimal quotes in closed form. In Section 4, we use a perturbation approach to propose a correction term that can easily be computed thanks to Monte-Carlo simulations. In Section 5, we extend our results to a more general multi-asset market making model with drift in prices, client tiering, several requested sizes for each asset and each tier, and fixed transaction costs for each asset and each tier. Numerical examples are presented in Section 6. They illustrate the quality of our closed-form approximations.

2 The multi-asset market making model

2.1 Model setup

We fix a probability space equipped with a filtration satisfying the usual conditions. In what follows, we assume that all stochastic processes are defined on . In all this paper, denotes the set of nonnegative real numbers, and denotes the set of positive real numbers.

For , the reference price of asset is modeled by a process with dynamics

where is a -dimensional Brownian motion with correlation matrix adapted to the filtration – hereafter we denote by the variance-covariance matrix associated with the process .

The market maker chooses at each point in time the price at which she is ready to buy/sell each asset: for , we let her bid and ask quotes for asset be modeled by two stochastic processes, respectively denoted by and .

For , we denote by and the two point processes modeling the number of transactions at the bid and at the ask, respectively, for asset . We assume in this section that the transaction size for asset is constant and denoted by . The inventory process of the market maker for asset , denoted by , has therefore the dynamics

and we denote by the (column) vector process .

For each , we denote by and the intensity processes of and , respectively. We assume that the market maker stops proposing a bid (respectively ask) price for asset when her position in asset following the transaction would exceed a given threshold (respectively ).444 is assumed to be a multiple of . It corresponds to the risk limit of the market maker for asset .

Formally, we assume that the intensities verify

where the processes and are defined by555It is often assumed in the literature that the point processes are independent of the Brownian motions. In that case, the quote processes and have to be independent of prices. In fact, the optimal control problem can be written in a weak form to show that this assumption is not necessary – see A for more details on the construction of the processes in that case.

Moreover, we assume that the functions and satisfy the following properties:

-

1.

and are twice continuously differentiable,

-

2.

and are decreasing, with , and ,

-

3.

,

-

4.

Finally, the process modelling the amount of cash on the market maker’s cash account has the following dynamics:

2.2 The optimization problems

We can consider two different optimization problems for the market maker. Following the initial model proposed by Avellaneda and Stoikov in [1], we can assume that she maximizes the expected value of a CARA utility function (with risk aversion parameter ) applied to the mark-to-market value of her portfolio at a given time . This mark-to-market value is the sum of the amount on the cash account and the mark-to-market value of the assets remaining in the portfolio at date .666In the literature there is sometimes a penalty function applied to the inventory at terminal time to “force” liquidation. Here, as we shall focus on the asymptotic regime of the optimal quotes, there is no point considering such a penalty. However, it is noteworthy that most of our non-asymptotic results could be generalized to the case of a quadratic terminal penalty. More precisely, her optimization problem writes

where is the set of predictable processes bounded from below. We call Model A our model with this first objective function.

Alternatively, as proposed by Cartea et al. in [10], we can consider a risk-adjusted expectation for the objective function of the market maker. In that case, the optimization problem writes

We call Model B our model with this second objective function.

2.3 The Hamilton-Jacobi-Bellman and Hamilton-Jacobi equations

Let be the canonical basis of . The Hamilton-Jacobi-Bellman equation associated with Model A is

| (1) | |||||

for all ,777Given a positive number , denotes the set of multiples of , i.e. with terminal condition

The Hamilton-Jacobi-Bellman equation associated with Model B is

| (2) | |||||

for all with terminal condition

For each and let us define two Hamiltonian functions888It is noteworthy that our definition of and differs from that of [18] (by a factor ). The alternative definition we use in this paper is also that of [5] for . and by

| (3) |

and

| (4) |

Using the ansatz introduced in [18] for the two functions and , i.e.

we see that solving the Hamilton-Jacobi-Bellman equations (1) and (2) boils down to finding the solution of the following Hamilton-Jacobi equation with in the case of Model A and in the case of Model B:

In both cases, the terminal condition simply boils down to

| (6) |

2.4 Existing theoretical results

From [18, Theorem 5.1], for a given there exists a unique , in time, solution of Eq. (2.3) with terminal condition (6).

Moreover (see [18, Theorems 5.2 and 5.3]), a classical verification argument enables to go from to optimal controls for both Model A and Model B. The optimal quotes as functions of are recalled in the following theorems (for details, see [18]).

In the case of Model A, the result is the following:

Theorem 1.

Then, for the optimal bid and ask quotes and in Model A are characterized by

| (7) | ||||

where the functions and are defined by

where for all and denote the first derivative of and , respectively.

For Model B, the result is the following:

Theorem 2.

Then, for the optimal bid and ask quotes and in Model B are characterized by

| (8) | ||||

where the functions and are defined by

where for all and denote the first derivative of and , respectively.

In the following two sections, we propose new methods to find approximations of the solution to the system of ordinary differential equations (ODEs) (2.3) with terminal condition (6). Eqs. (7) and (8) can then serve to go from approximations of (hereafter called – slightly abusively – the value function) to approximations of the optimal quotes. The resulting quotes correspond to what the reinforcement learning community calls the greedy quoting strategy associated with the proxy of the value function.999The true optimal quotes correspond to the greedy strategy with respect to the value function (in Model A) or (in Model B) deduced from the true .

3 A quadratic approximation of the value function and its applications

3.1 Introduction

In the field of (stochastic) optimal control, finding value functions and optimal controls in closed form is the exception rather than the rule. One important exception goes with the class of Linear-Quadratic (LQ) and Linear-Quadratic-Gaussian (LQG) problems. Of course, the above market making problem does not belong to this class of control problems, for instance because the control of point processes is nonlinear by nature. Nevertheless, we see that price risk appears in both Model A and Model B through the quadratic term in the Hamilton-Jacobi equation (2.3). The main idea of this paper consists in replacing the Hamiltonian functions associated with our market making problem by quadratic functions that approximate them. The interest of quadratic Hamiltonian functions lies in that the resulting Hamilton-Jacobi equations can be solved in closed-form using the same tools as for LQ/LQG problems, i.e. Riccati equations.

At first sight, approximating the Hamiltonian functions involved in Eq. (2.3) by quadratic functions seems inappropriate. For all , the functions and are indeed positive and decreasing and approximating them with U-shaped functions can only be valid locally. However, one has to bear in mind that our goal is to approximate the solution of the Hamilton-Jacobi equations and not the Hamiltonian functions. This remark is particularly important because the Hamiltonian terms involved in the Hamilton-Jacobi equations are (up to the indicator functions that we shall discard in what follows by considering the limit case where ) of the form

Assuming that , we clearly see that, with respect to asset , the function we need to approximate is rather than and themselves, and it is natural to approximate the former function with a U-shaped one!

Let us replace for all the Hamiltonian functions and by the quadratic functions101010We omit the subscript in the definition of and . In particular, although the subscript is not written, the coefficients , , , , , and do depend on .

Remark 1.

A natural choice for the functions and derives from Taylor expansions around . In that case,

We denote by the approximation of associated with the functions and , i.e. if we consider the limit case where , verifies

| (9) | |||||

and of course we consider the terminal condition

| (10) |

3.2 An approximation of the value function in closed form

Eq. (9) with terminal condition (10) can be solved in closed form. To prove this point, we start with the following proposition:

Proposition 1.

Let us introduce for ,

Let us consider three differentiable functions , , and solutions of the system of ordinary differential equations111111 (resp. ) stands throughout this paper the set of positive semi-definite (resp. definite) symmetric -by- matrices.

| (11) |

with terminal conditions

| (12) |

where is the linear operator mapping a matrix onto the vector of its diagonal coefficients.

Proof.

We have

where the last equality comes from the definitions of and the identification of the terms of degree , , and in .

As the terminal conditions are satisfied, the result is proved. ∎

Proposition 2.

Proof.

The system of ODEs (11) being triangular – though not linear – we tackle the equations one by one, in order.

Solution for

First, we observe that is a

positive diagonal matrix. Therefore is well defined. Then, since , is well defined and in .

Now, by introducing the change of variables

the terminal value problem for in (11) becomes

| (16) |

To solve (16) let us introduce the function defined by

that is a function verifying and .

We have

and . Therefore, by Cauchy-Lipschitz theorem, we have .

Wrapping up, we obtain

Solution for

Let us notice that, by definition of the exponential of a matrix, for all , the matrices , , , , and commute. Therefore

Therefore, we can apply the method of Variation of Parameters to the linear ODE characterizing to obtain

Solution for

We simply integrate the ODE characterizing to obtain .

∎

Proposition 3.

Then,

where and is the Moore-Penrose generalized inverse of .

Proof.

This proof is divided into three parts corresponding to the derivation of the asymptotic

expression for , , and , respectively.

Asymptotics for

Let us recall first that . Therefore, there exists an orthogonal matrix and there exists a diagonal matrix with nonnegative entries such that . From Eq. (13) we have

As , we clearly have

Asymptotics for

Using the spectral decomposition of introduced in the above paragraph, we see that

and therefore, after integration,

and

Wrapping up, we get that is equal to

where

Let us prove that . For that

purpose, let us consider and let us notice that there exists

such that , where

the norm used is the Euclidian norm on . Let us also denote by

the quantity .

Using the operator norm (still denoted by ) associated with the Euclidian norm on and its well-known link with the spectral radius, we see that for ,

By defining and , we have

Therefore,

which allows to conclude that .

Now, as converges toward the orthogonal projector on , which is also given by , we conclude that

Asymptotics for

The asymptotic behavior of is a straightforward consequence of that of and .

∎

3.3 From value functions to heuristics and quotes

3.3.1 Motivation for closed-form approximations

An approximation in closed form of the value function can be motivated by its numerous applications. In the following, we highlight three of them.

First, it can serve as a heuristic evaluation function in reinforcement learning algorithms. Indeed, in problems where the time horizon is too far away to consider full exploration in time, it is often useful, when using Monte-Carlo-based reinforcement learning techniques, to proxy the value of states in a tractable way – analogous to algorithms such as Deep Blue. The above closed-form approximations can be used for that purpose. Moreover, because the value of is irrelevant for comparing two states (it vanishes when computing the difference in the value function between two points), it is sometimes possible, especially when is large, to consider the asymptotic expression

instead of .

Second, a closed-form approximation of the value function can be used as a starting point in iterative methods designed to compute the value function (value iteration algorithm, actor-critic algorithms, etc.). Unlike for the above use, the value of matters in that case.

A third important application, and the one that initially motivated our paper, is for computing policies (quotes, in our case). Indeed, a policy can be deduced from an approximation of the value function by computing the greedy strategy associated with that approximation. In our market making problem, the quotes obtained in this way are not only easy to compute, but also have the advantage of being easily interpretable.

3.3.2 Quotes: the general case

The greedy quoting strategy associated with our closed-form proxy of the value function leads to the following quotes for all :

where and are given in Theorems 1 and 2 for and respectively (depending on whether one considers Model A or Model B).

The asymptotic regime exhibited in the above paragraphs can then serve to obtain the following simple closed-form approximations:

| (17) | |||||

| (18) |

It is interesting to notice here that the closed-form approximation of the optimal bid and ask quotes for asset depend on the current value of the inventory through the term . Since and the functions and are monotone, we have that, all else equal, the quotes for asset depend monotonically on the inventory in asset (the bid and ask prices decrease (resp. increase) when the inventory is positive (resp. negative)). The dependence on the inventory in other assets is more subtle as it is linked to the matrix which models the complex interplay between price risk and liquidity risk. Also, as already noted in [20] the influence of the risk aversion parameter is ambiguous and depends on the value of inventories.

In the case of symmetric intensities, i.e. when for all , the Hamiltonian functions and given in Eqs. (3) and (4) are identical and thus it is natural to set for all . In that case, (17) and (18) simplify into

| (19) | |||||

| (20) |

All these approximations of the optimal quotes can be used directly or as starting points in iterative methods designed to compute the optimal quotes (policy iteration algorithm, actor-critic algorithms, etc.).

3.3.3 Quotes: the case of symmetric exponential intensities

Exponential intensity functions play an important role in the optimal market making literature and more generally in the algorithmic trading literature. This shape of intensity functions, initially proposed by Avellaneda and Stoikov in [1], leads indeed to simplification because of the form of the associated Hamiltonian functions.

If we assume that the intensity functions are given, for all , by

then (see [18]) the Hamiltonian functions are given, for all , by

where

and the functions and are given, for all , by

Therefore, if we consider the quadratic approximation of the Hamiltonian functions based on their Taylor expansion around (see Remark 1), then (19) and (20) become

where and

It is noteworthy that these approximations of the optimal quotes are affine in the current inventory. In particular, in the case of Model A, when the number of assets is reduced to one (with unitary transaction size), they coincide with the affine closed-form approximations obtained in the paper [20] of Guéant, Lehalle, and Fernandez-Tapia. Their approximations, however, are obtained in a fundamentally different manner, by using spectral arguments and a continuous approximation of the initial discrete problem.

Another useful point of view on the above quoting strategy is by observing the resulting approximations of the optimal (half) bid-ask spread and skew. The approximations of the optimal (half) bid-ask spread and skew for asset are respectively given by

and

These approximations give us a constant bid-ask spread and a skew linear in the inventory. This translates well the intuition that the skew has the role of inventory risk management, whereas the spread balances the trade-off between frequency of transactions and profit per round-trip trade (the term in Model A, which reduces to in the case of Model B121212It is noteworthy that in the case of Model B the bid-ask spread is a nondecreasing function of the risk aversion parameter .), plus an additional risk aversion buffer (the term ).

On the parameter sensitivity analysis, beyond the above remarks, the reader is referred to [20] for a comprehensive analysis in the single-asset case. The complex interplay between price risk and liquidity risk expressed through makes the sensitivity analysis less obvious in the multi-asset case.

4 Beyond the quadratic approximation: towards a correction term

In Section 3, we approximated the Hamiltonian functions by quadratic functions in order to “approximate” the Hamilton-Jacobi equation characterizing the value function and then approximate the value function itself. To go further, we can consider a perturbative approach around our quadratic approximation. This means that we regard the real Hamiltonian functions as small perturbations of the quadratic functions used to approximate them and consider then a first order approximation (the zero-th order approximation being then that obtained in Section 3).

Formally, writing

and plugging these expressions in Eq. (2.3) in the limit case where for all , we obtain

Therefore,

and we have the terminal condition .

By Feynman-Kac representation theorem, we have

where under the process satisfies

with, for each , and constructed like and but with respective intensities given at time by

In practice, it means that we can approximate by plus a correction term that takes the form of an expectation:

Of course this new approximation is not a closed-form one. However, the correction term can be computed using a Monte-Carlo simulation for a specific . In particular, it means that upon receiving a request for quote from a client and if time permits (which depends on asset class and market conditions), a market maker can perform a Monte-Carlo simulation to obtain an approximation of the value function at the relevant points to compute a quote that might account more accurately for the liquidity of the requested asset than a quote computed using the closed forms of Section 3.3.2.

5 A multi-asset market making model with additional features

5.1 A more general model

In Section 2.1 we presented a multi-asset extension to the classical single-asset market making model of Avellaneda and Stoikov. This extension can itself be extended to encompass important features of OTC markets. In this section we extend our results to a more general multi-asset market making model with drift in prices to model the views of the market maker, client tiering, distributed requested sizes for each asset and each tier, and fixed transaction costs for each asset and each tier.

In terms of modeling, the addition of drifts to the price processes is straightforward. Formally, we assume that for each , the dynamics of the price process of asset is now given by

where and are defined as in Section 2.1 and where is a real constant. In what follows, we denote by the vector .

In OTC markets, market makers often divide their clients into groups, called tiers, for instance because they do not have the same commercial relationship with all clients or because the propensity to transact given a quote differs across clients. In particular, they can answer/stream different quotes to clients from different tiers.131313There can also be tiers to proxy the existence of trading platforms with different clients and/or different costs. Let us denote here by the number of such tiers.

In addition to introducing tiers, we can drop the assumption of constant request size per asset and consider instead that, for each asset and each tier, the size of the requests at the bid and at the ask are distributed according to known distributions.

Mathematically, the bid and ask quotes that the market maker propose are then modeled by the maps

where is the index of the asset, is the index of the tier, and is the size of the request (in number of assets). In the same vein as in Section 2.1, we introduce141414 is omitted in what follows.

and the maps and are assumed to be -predictable and bounded from below by a given constant .151515This additional constraint of a fixed lower bound is just a technical one to be able to state theorems in the general case where request sizes are distributed (see [5]).

With these new features in mind, we introduce for each asset and for each tier the processes and modeling the number of transactions in asset with clients from tier at the bid and at the ask, respectively. They are -marked point processes, with respective intensity kernels and given by

where and are the two probability measures representing the distribution of the requested sizes at the bid and at the ask respectively, for asset and tier , and where and satisfy the same assumptions as those satisfied by the intensity functions of Section 2.1.

For asset , the resulting inventory has dynamics

where for each tier and are the random measures associated with the processes and , respectively.

Finally, we consider the addition of fixed transaction costs.161616Proportional transaction costs can be considered in the initial model through shifts in the intensity functions. For that purpose, we introduce for each asset and for each tier two real numbers and modelling the fixed cost of a transaction in asset with a client from tier , at the bid and at the ask, respectively.

The resulting cash process has, consequently, the following dynamics:

5.2 The Hamilton-Jacobi equation

In this new setting, one can again show that the two optimization problems introduced in Section 2.1 boil down to the resolution of a Hamilton-Jacobi equation of the form

| (21) | ||||

with terminal condition

| (22) |

where in the case of Model A and in the case of Model B, and where the functions and are defined by

and

Remark 2.

When , the dependence in of the Hamiltonian functions vanishes. Nevertheless, we keep the variable for the sake of consistency.

Following a method similar to that developed in [5], we can show that, for a given there exists a unique bounded function , in time, solution of Eq. (21) with terminal condition (22).

Moreover, under the (mild) assumption that the measures and have moments of order , a classical verification argument enables to go from to optimal controls for both Model A and Model B. The optimal quotes as functions of are given by the two theorems that follow.

In the case of Model A, the result is the following:

Theorem 3.

Then, for and , the optimal bid and ask quotes as functions of the trade size , and in Model A are characterized by

where the functions and are defined by

For Model B, the result is the following:

5.3 Quadratic approximation

As before, let us replace for all and , the Hamiltonian functions and by the functions

Remark 3.

Here, and (for ) are functions of A natural choice for the functions and derives from Taylor expansions around . In that case,

If we consider the limit case where for all , Eq. (21) then becomes

| (23) |

with terminal condition

| (24) |

Using the same ansatz as in Section 3, we obtain the following result (we omit the proof as it follows the same logic as for that of Proposition 1):

Proposition 4.

Let us introduce for all , the following constants:

and

Let us consider three differentiable functions , , and solutions of the system of ordinary differential equations

| (25) |

with terminal conditions

| (26) |

We can now solve (25) with terminal conditions (26) in closed form. This is the purpose of the following proposition whose proof is omitted (see Proposition 2 for a similar proof).

Proposition 5.

Now, using the same method as in Section 3, we get the following asymptotic results:

Proposition 6.

If , then,

where and is the Moore-Penrose generalized inverse of

.

Remark 4.

The assumption is satisfied when or when is invertible. If this assumption is not satisfied, then it can be shown that . In particular, there is no constant asymptotic approximation of the quotes. In fact, if the assumption is not satisfied, the market maker may have an incentive to propose very good quotes to clients in order to build portfolios bearing positive return at no risk.

5.4 From value functions to heuristics and quotes

5.4.1 Quotes: the general case

The greedy quoting strategy associated with our closed-form proxy of the value function leads to the following quotes for all and :

where and are given in Theorems 3 and 4 for and respectively (depending on whether one considers Model A or Model B).

The asymptotic regime exhibited in the above paragraphs can then serve to obtain the following simple closed-form approximations:

| (27) | ||||

| (28) | ||||

If we assume that for all and for all we have and , then , and it is thus natural to chose symmetric approximations of the Hamiltonian functions, i.e. . In that case, (27) and (28) simplify into

| (29) | |||||

| (30) |

All these approximations of the quotes can be used directly or as a starting point in iterative methods designed to compute the optimal quotes (policy iteration algorithms, actor-critic algorithms, etc.).

5.4.2 Quotes: the case of symmetric exponential intensities

If we assume that for all and for all we have and intensity functions given by

then (see [18]), in the limit case where the Hamiltonian functions are given, for all and , by

where

and the functions and are given, for all and , by

Therefore, if we consider the quadratic approximation of the Hamiltonian functions based on their Taylor expansion around (see Remark 3), then (29) and (30) become

where and

6 Numerical results

To assess the quality of our approximations, we consider a two-asset example for which we can approximate numerically the true function and the optimal quotes. By using a Euler scheme in dimension 3 (one dimension for time and two dimensions for inventory) it is indeed possible to approximate numerically the solution of Hamilton-Jacobi equations on a grid.

6.1 Characteristics of our example with two assets

We consider the following characteristics for the two assets:

-

1.

Asset prices: .

-

2.

Drifts: , .

-

3.

Volatilities: , .

-

4.

Correlation:

This corresponds to a covariance matrix given by

We consider Model B171717The results would be similar for Model A. with time horizon and risk aversion parameter .

We consider a framework with one tier only and no transaction costs.

The intensity functions are given for all by:

with , , and . This corresponds to requests per day, a probability of to trade when the answered quote is the reference price and a probability of to trade when the answered quote is the reference price improved by 1 cent.

Request sizes are distributed according to a Gamma distribution with and This corresponds to an average request size of assets (i.e. approximately ) and a standard deviation equal to half the average.

6.2 Value function and optimal quotes

In order to discretize the problem, we first approximate the Gamma distribution of sizes with sizes: , , , and assets – thereafter refered to by very small, small, large, and very large size – with respective probability , , and . We impose risk limits and , i.e. no trade that would result in an inventory for asset 1 such that is accepted, and similarly no trade that would result in an inventory for asset 2 such that is accepted.

The solution to Eq. (21) with terminal condition (22) can then be approximated numerically using a monotone implicit Euler scheme on a grid of size ( points in time, points for the inventory of asset , and points for the inventory of asset 2).

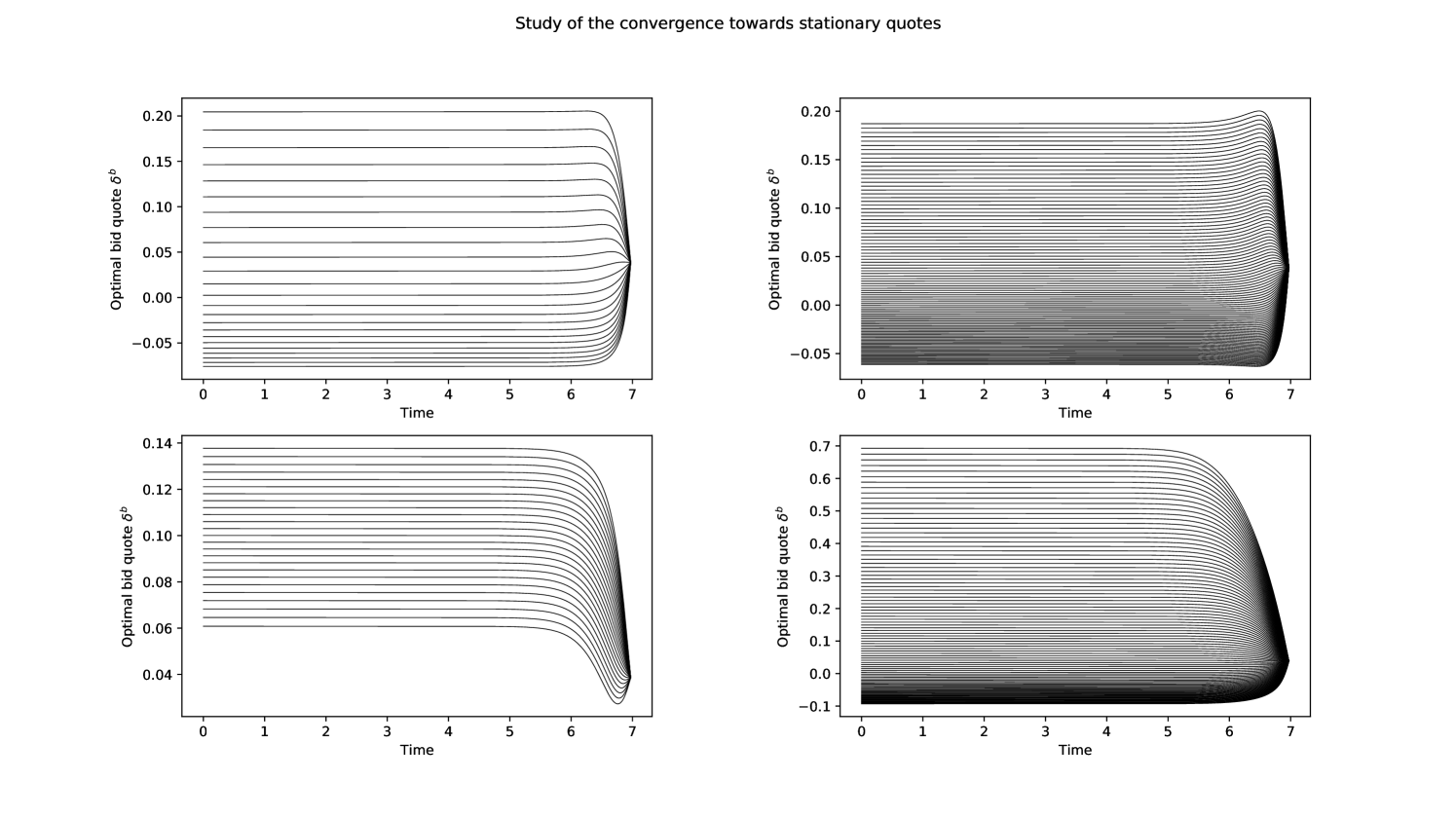

Because we are mainly interested in asymptotic quotes, it is important to check that the time horizon chosen is sufficienty long. For that purpose, we plot in Figure 1 the optimal bid quotes for asset 1 and asset 2 at time for different values of the inventory. We see that the asymptotic regime is clearly reached and, from now on, we will only consider the value function and the optimal quotes at time .

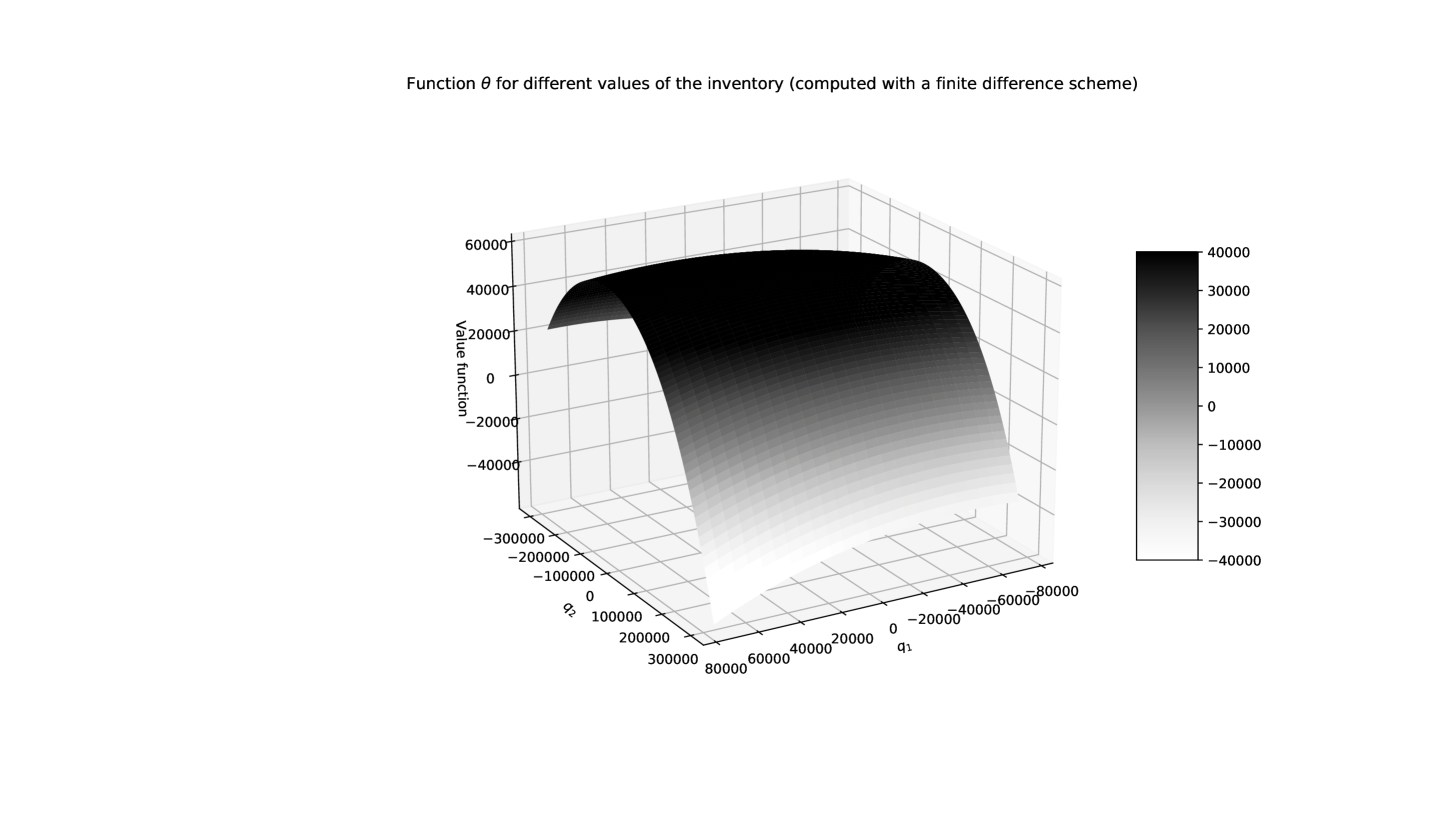

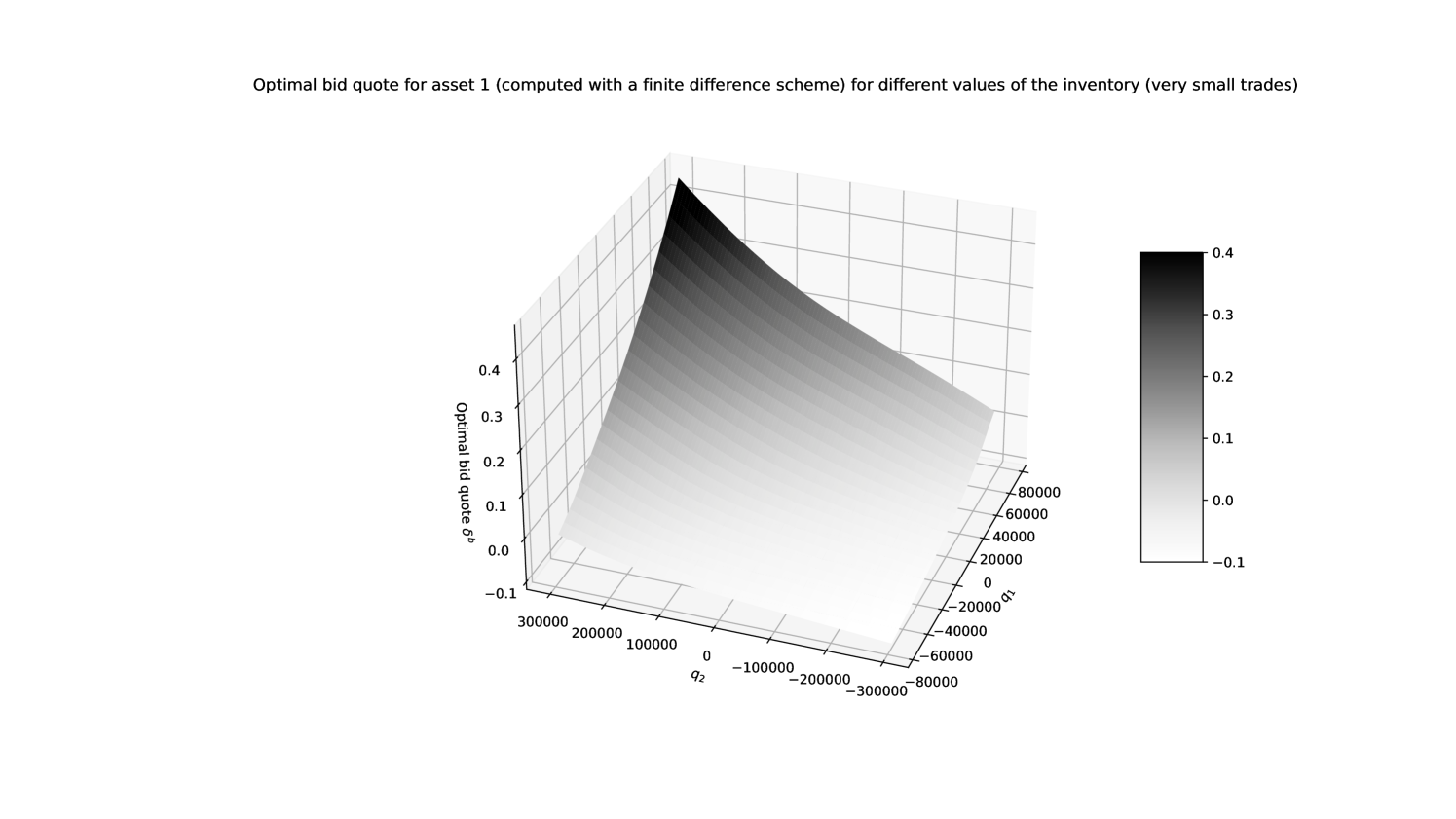

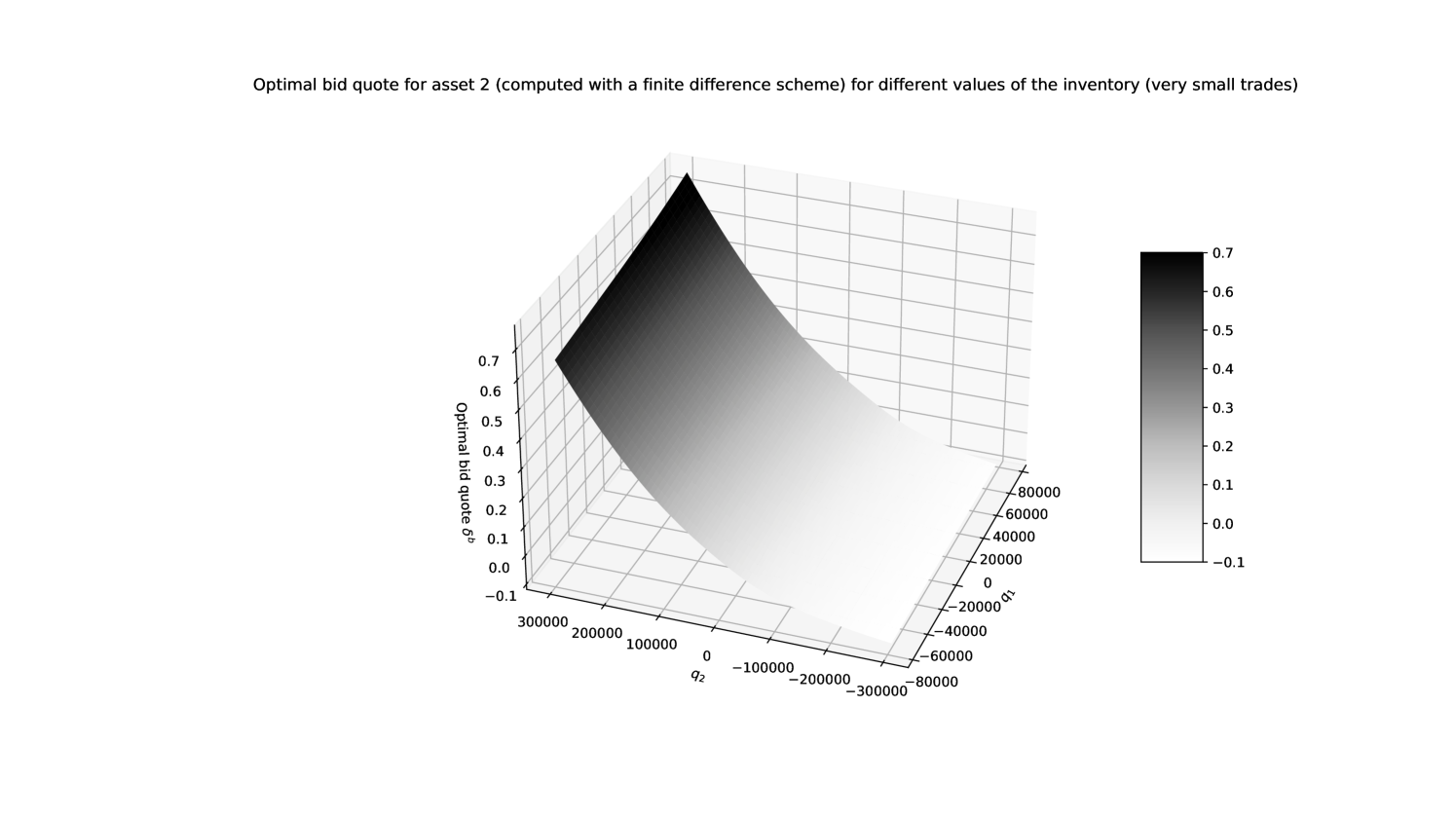

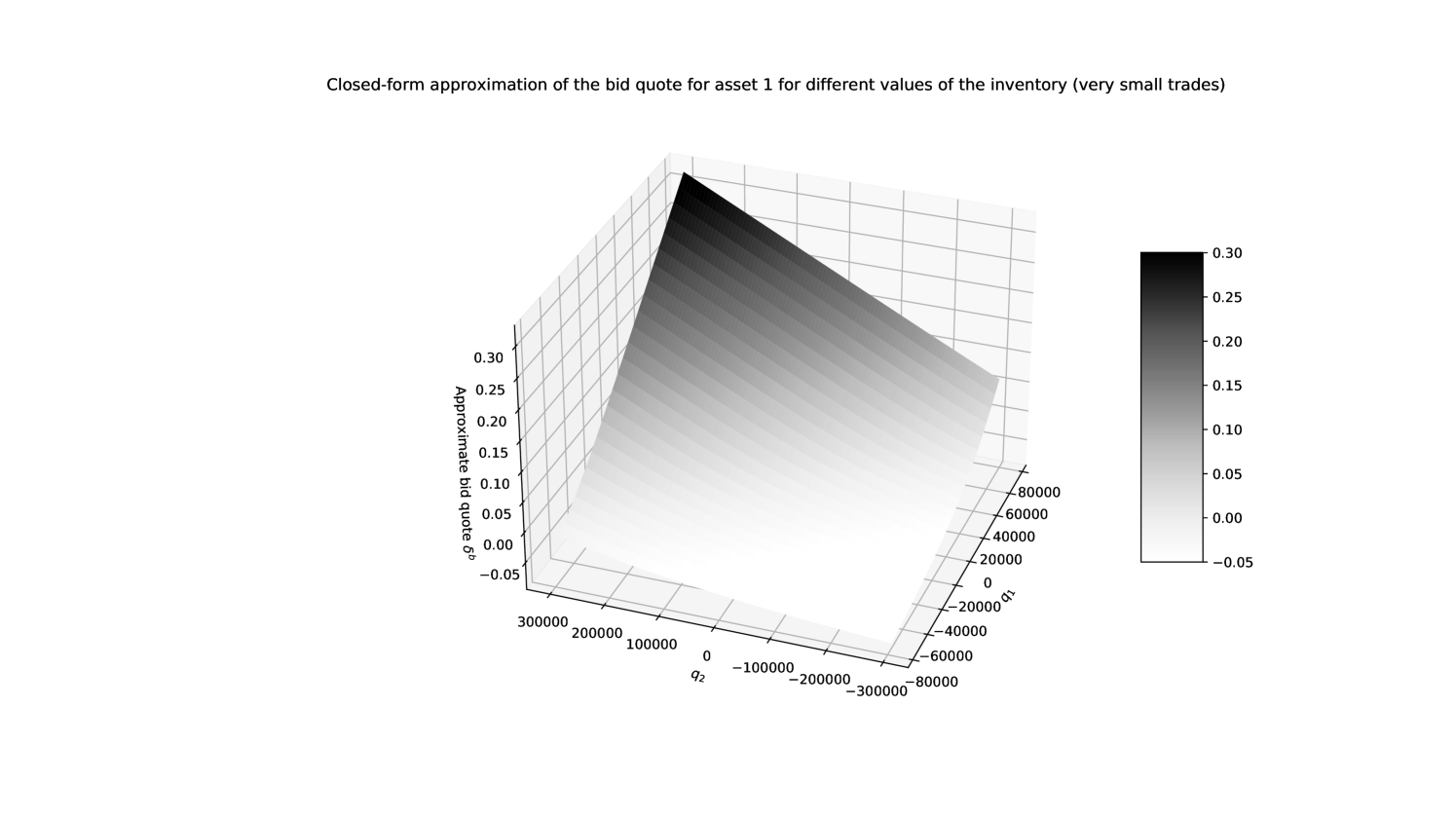

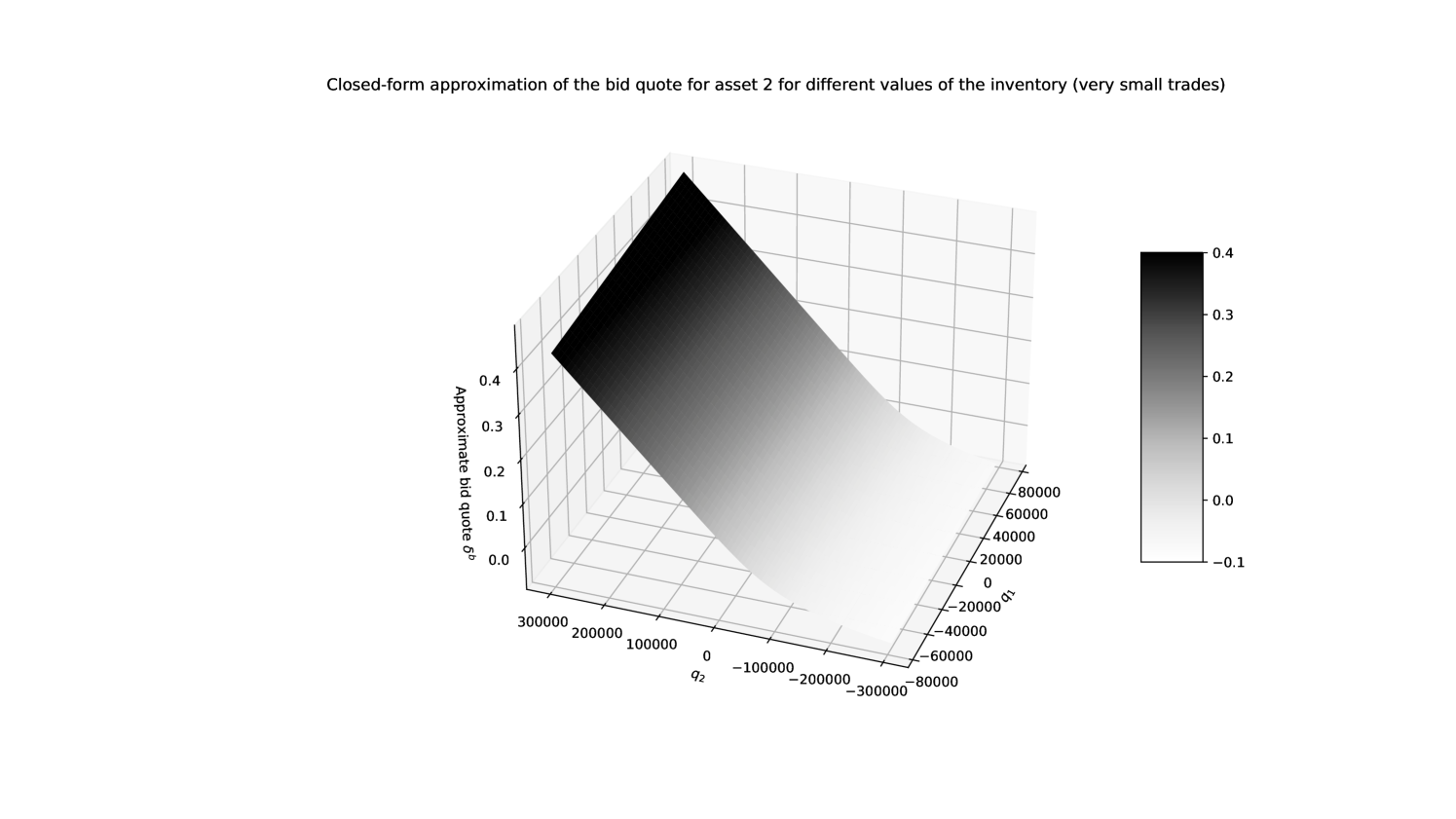

The numerical approximation of the value function (at time ) is plotted in Figure 2. The shape of the function is as expected given the risk penalty, the positive drift in the prices of asset 1 and the negative drift in the prices of asset 2. The associated bid quotes are plotted in Figures 3 and 4 respectively. The shape of the quote surfaces is as expected given the positive correlation coefficient (see [5] or [18] for a deeper discussion about the effect of the different parameters).

6.3 Comparison with closed-form approximations

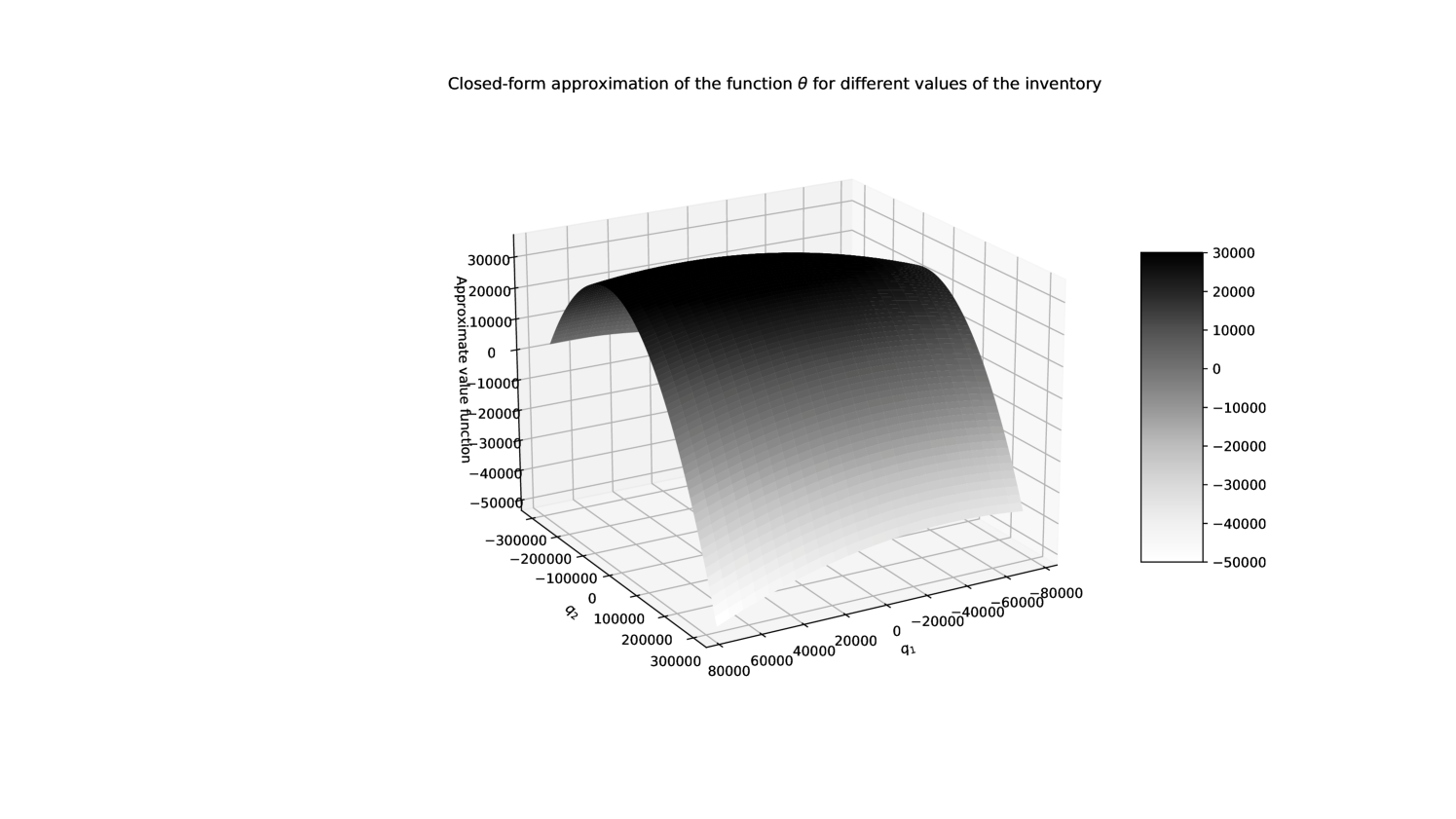

We now move on to our closed-form approximations. We first plot in Figure 5 the closed-form approximation given by Proposition 4.

We clearly see that, in spite of differences in level between the true value function aproximated numerically and the closed-form approximation, the shape is the same. Therefore, the finite differences involved in the computation of the associated quotes should be similar. This is roughly confirmed in Figures 6 and 7 that are the closed-form counterparts of Figures 3 and 4.

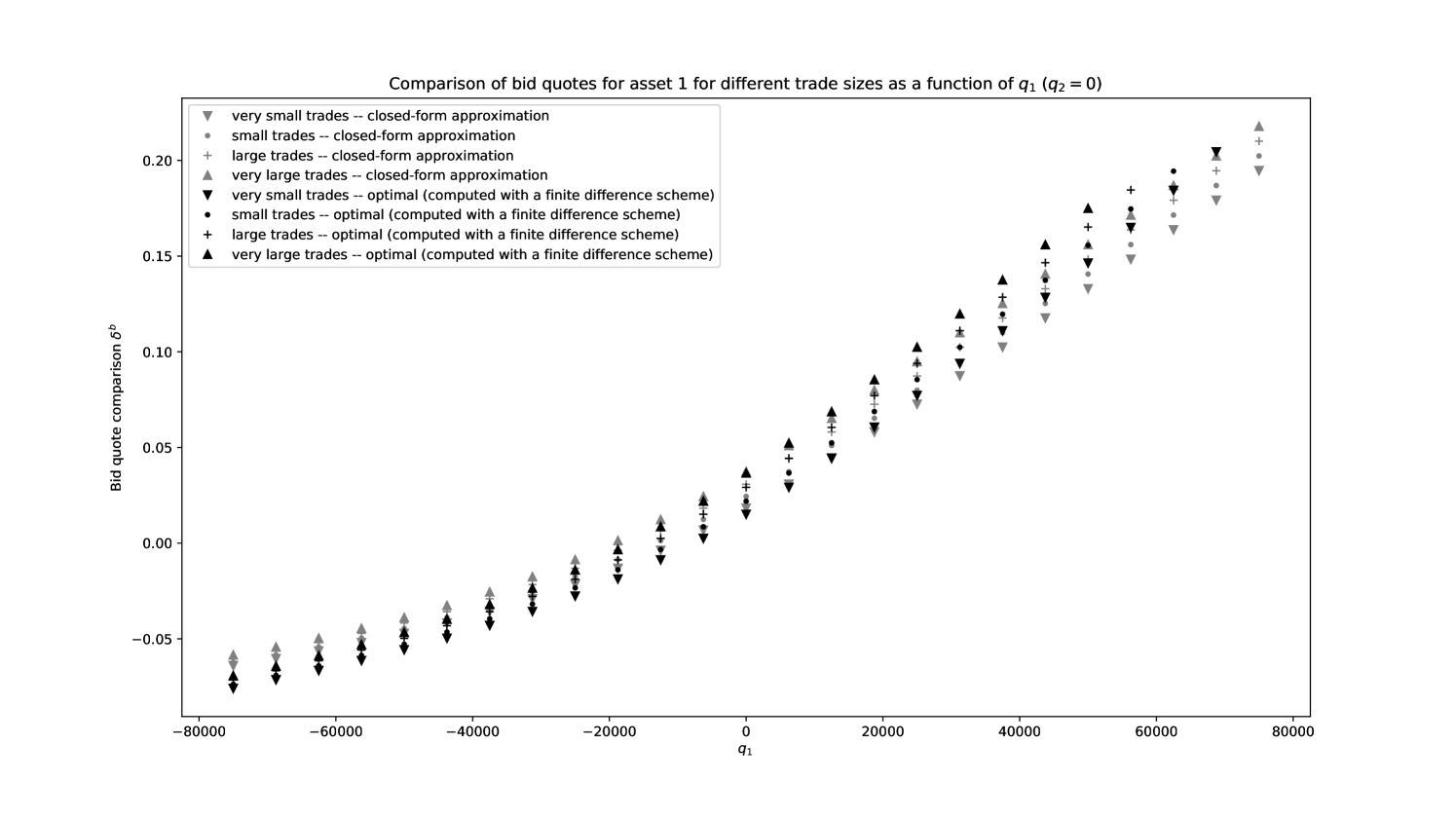

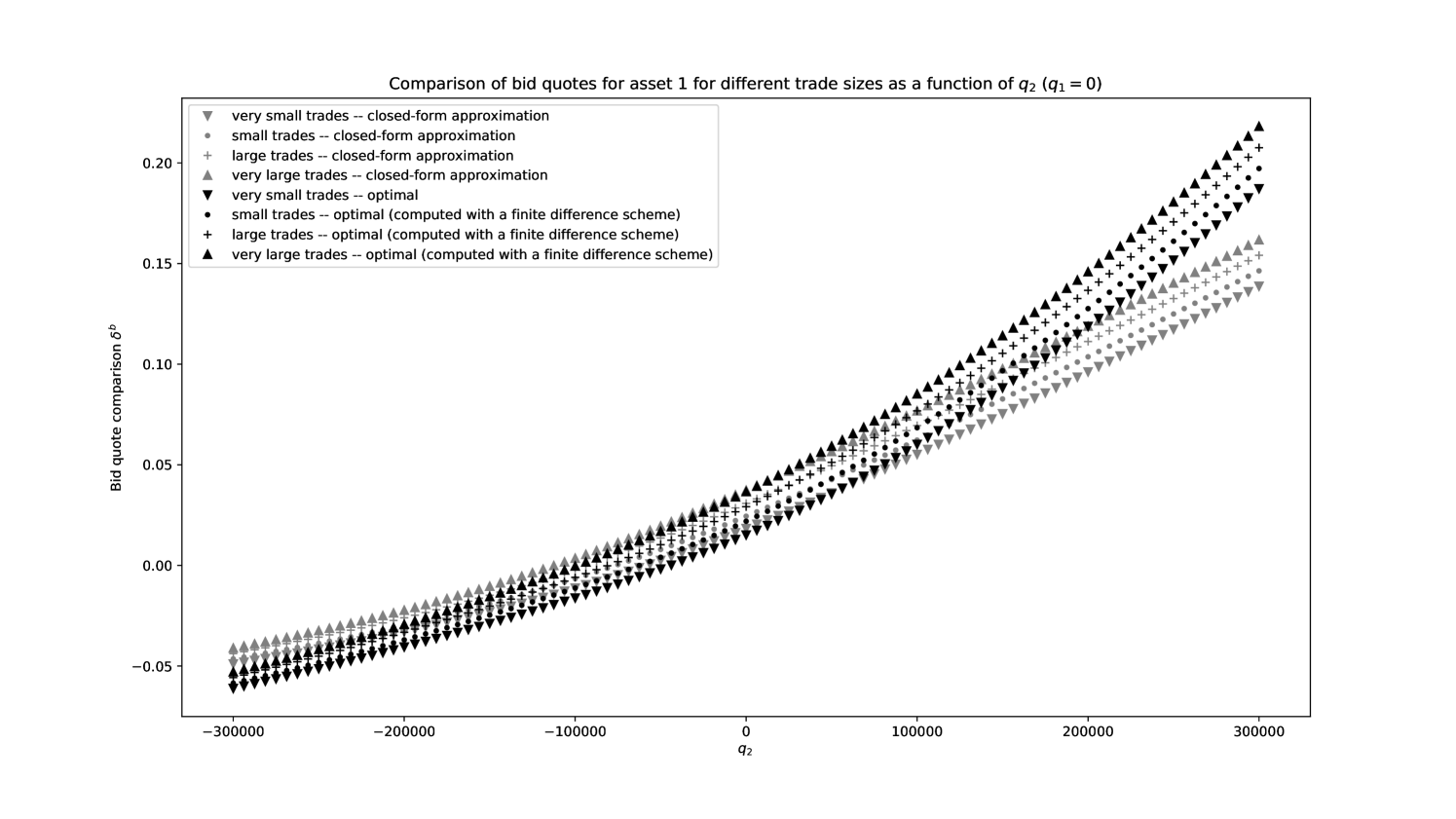

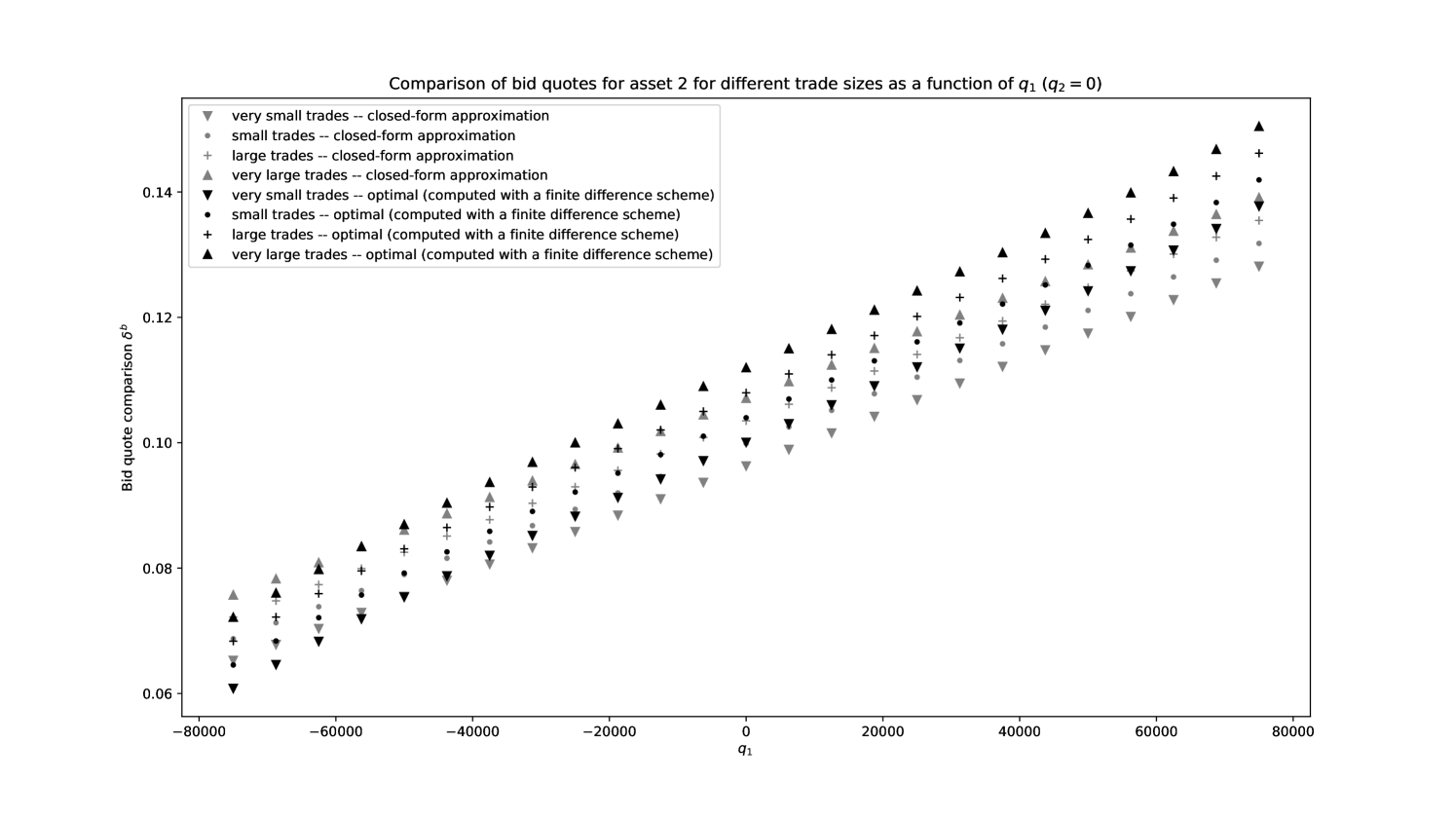

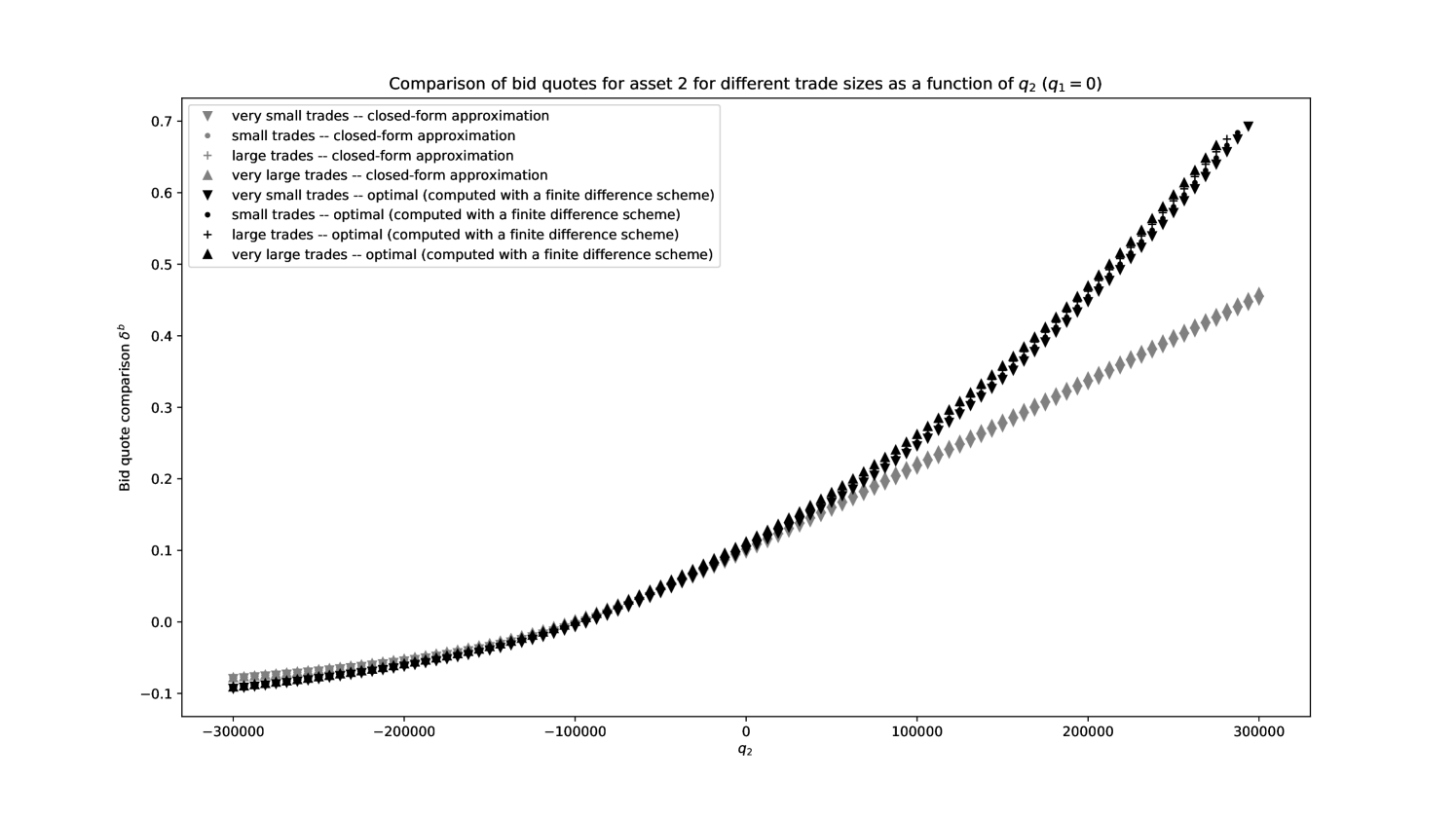

In order to assess more precisely the quality of our closed-form approximations, we plot in Figures 8, 9, 10, and 11 the functions

where is the optimal bid quote for asset as a function of time, inventory, and size of request and is the closed-form approximation of the optimal bid quote for asset as a function of inventory and size of request.

We clearly see that our closed-form approximations are close to the true optimal quotes, except for large values of the inventory in asset 2.

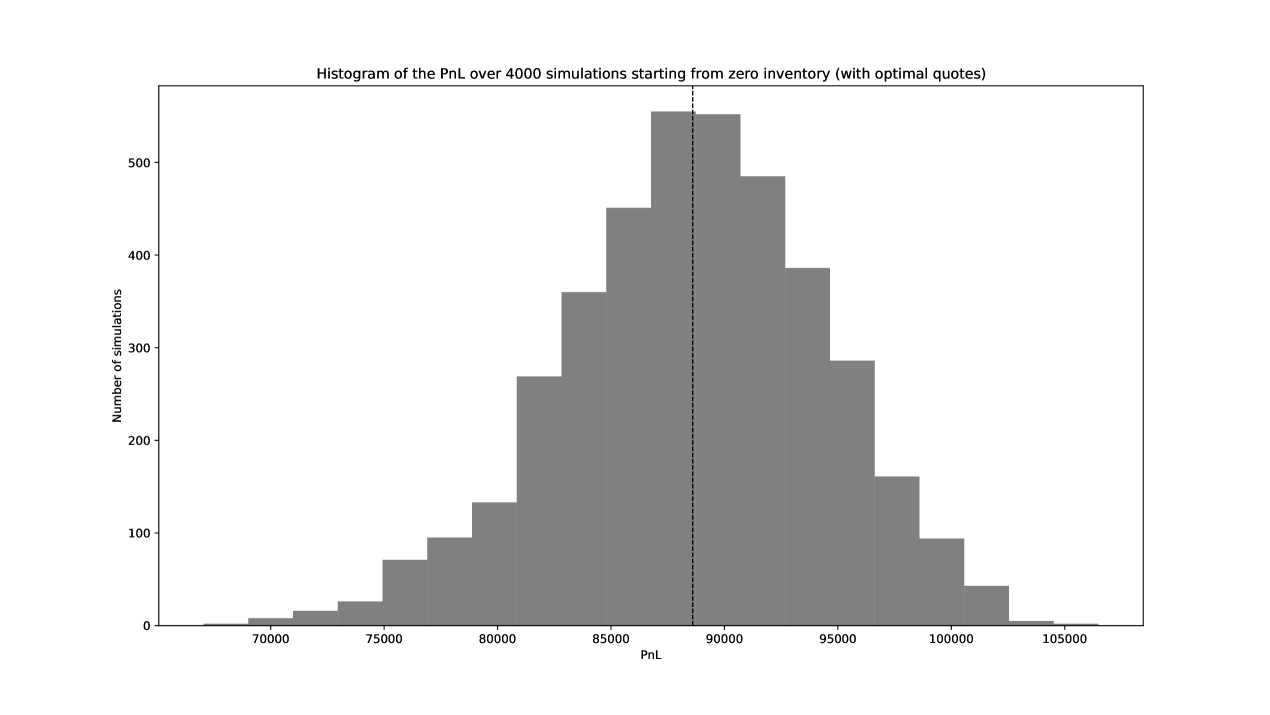

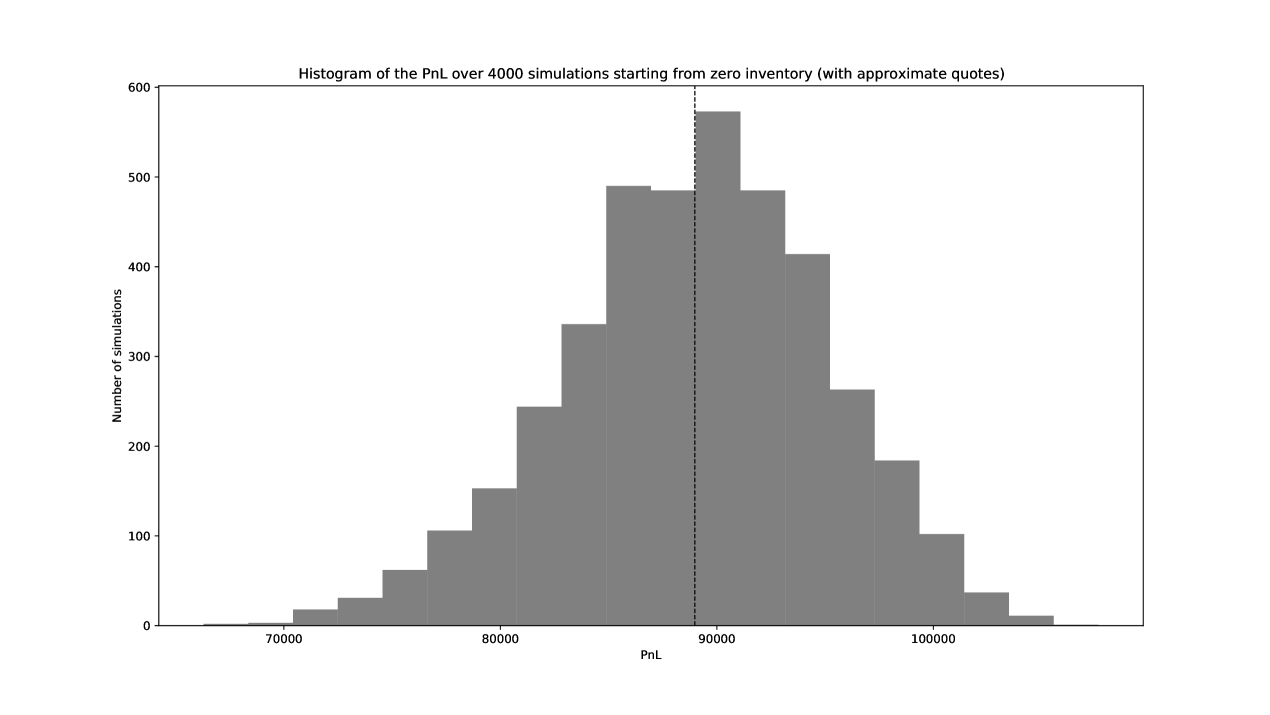

In order to confirm the quality of our closed-form approximations, we compare the performance of a market maker, when quoting the true optimal quotes versus their closed-form approximations. The respective distributions of PnL after 4000 Monte-Carlo simulations are plotted in Figures 12 and 13.

When using the optimal quotes, the market maker gets an average PnL of with a standard deviation of . When using the closed-form approximation, the performance is very similar, as she gets an average PnL of with a standard deviation of .

These results are really satisfying in terms of performance. We see that, although the closed-form approximation of optimal quotes may be inaccurate for large values of the inventory, such large inventory are seldom reached and therefore the gap between quotes does not really impact the distribution of the PnL.

We believe that what we observe here in this two-asset example is general. In particular, the results in higher dimensions should be just as good.

Conclusion

We proposed closed-form approximations for the value functions associated with many multi-asset extensions of the market making models available in the literature. These closed-form approximations have been obtained through the “approximation” of a Hamilton-Jacobi equation by another Hamilton-Jacobi equation that can be simplified into a Riccati equation and two linear ordinary differential equations, all solvable in closed form. These closed-form approximations can be used for various purposes, in particular to design quoting strategies through a greedy approach. The resulting closed-form approximations of the optimal quotes generalize those obtained by Guéant, Lehalle, and Fernandez-Tapia in [20] to a general framework suitable for practical use.

Acknowledgements

The authors would like to thank Bastien Baldacci (Ecole Polytechnique) and Iuliia Manziuk (Ecole Polytechnique) for their careful reading of an initial version of the paper. Olivier Guéant would like to thank the Research Initiative “Nouveaux traitements pour les données lacunaires issues des activités de crédit” financed by BNP Paribas under the aegis of the Europlace Institute of Finance for its support. A special thank goes to Laurent Carlier (BNP Paribas) for his vivid interest in academic questions around market making throughout the years.

Appendix A On the construction of the processes and

Let us consider a new filtered probability space . For the sake of simplicity, assume that there is only one asset with size of transactions denoted by and risk limit (the generalization is straightforward). Let us assume that the reference price of that asset is driven by a Brownian motion as in Section 2.1. Let us introduce and two independent Poisson processes of intensity , independent of . Let and be two processes, starting at 0, solutions of the coupled stochastic differential equation:

Then, under and are two point processes with respective intensities

where For each , we introduce the probability measure given by the Radon-Nikodym derivative

| (31) |

where is the unique solution of the stochastic differential equation

with , where and are the compensated processes associated with and , respectively.

We then know from the Brémaud-Jacod version of Girsanov theorem (see [6]) that under , the jump processes and have respective intensities

as in Section 2.1 of the paper. Since is still a Brownian motion under , our optimal control problem can be seen as the choice of an optimal probability measure .

References

- [1] Marco Avellaneda and Sasha Stoikov. High-frequency trading in a limit order book. Quantitative Finance, 8(3):217–224, 2008.

- [2] Bastien Baldacci, Philippe Bergault and Olivier Guéant. Algorithmic market making for options. Quantitative Finance, 21(1):85–97, 2021.

- [3] Nicolas Baradel, Bruno Bouchard, David Evangelista, and Othmane Mounjid. Optimal inventory management and order book modeling. ESAIM: Proceedings and Surveys, 65:145–181, 2018.

- [4] Alexander Barzykin, Philippe Bergault, and Olivier Guéant. Algorithmic market making in FX cash markets. arXiv preprint arXiv:2106.06974, 2021.

- [5] Philippe Bergault and Olivier Guéant. Size matters for OTC market makers: general results and dimensionality reduction technique. Mathematical Finance, 31(1):279–322 2020.

- [6] Pierre Brémaud and Jean Jacod. Processus ponctuels et martingales: résultats récents sur la modélisation et le filtrage. Advances in Applied Probability, 9(2), 362–416, 1977.

- [7] Luciano Campi and Diego Zabaljauregui Optimal market making under partial information with general intensities. Applied Mathematical Finance–27, 2020.

- [8] Álvaro Cartea, Ryan Donnelly, and Sebastian Jaimungal. Algorithmic trading with model uncertainty. SIAM Journal on Financial Mathematics, 8(1):635–671, 2017.

- [9] Álvaro Cartea, Sebastian Jaimungal, and José Penalva. Algorithmic and high-frequency trading. Cambridge University Press, 2015.

- [10] Álvaro Cartea, Sebastian Jaimungal, and Jason Ricci. Buy low, sell high: A high frequency trading perspective. SIAM Journal on Financial Mathematics, 5(1):415–444, 2014.

- [11] Álvaro Cartea, Sebastian Jaimungal, and Jason Ricci. Algorithmic trading, stochastic control, and mutually exciting processes. SIAM Review, 60(3):673–703, 2018.

- [12] Sofiene El Aoud and Frédéric Abergel. A stochastic control approach to option market making. Market microstructure and liquidity, 1(01):1550006, 2015.

- [13] Omar El Euch, Thibaut Mastrolia, Mathieu Rosenbaum, and Nizar Touzi. Optimal make-take fees for market making regulation. Mathematical Finance, 31(1):109–148, 2021.

- [14] Pietro Fodra and Mauricio Labadie. High-frequency market-making with inventory constraints and directional bets. arXiv preprint arXiv:1206.4810, 2012.

- [15] Pietro Fodra and Huyên Pham. High frequency trading and asymptotics for small risk aversion in a Markov renewal model. SIAM Journal on Financial Mathematics, 6(1):656–684, 2015.

- [16] Sanford J Grossman and Merton H Miller. Liquidity and market structure. the Journal of Finance, 43(3):617–633, 1988.

- [17] Olivier Guéant. The Financial Mathematics of Market Liquidity: From optimal execution to market making, volume 33. CRC Press, 2016.

- [18] Olivier Guéant. Optimal market making. Applied Mathematical Finance, 24(2):112–154, 2017.

- [19] Olivier Guéant and Charles-Albert Lehalle. General intensity shapes in optimal liquidation. Mathematical Finance, 25(3):457–495, 2015.

- [20] Olivier Guéant, Charles-Albert Lehalle, and Joaquin Fernandez-Tapia. Dealing with the inventory risk: a solution to the market making problem. Mathematics and financial economics, 7(4):477–507, 2013.

- [21] Olivier Guéant and Iuliia Manziuk. Deep reinforcement learning for market making in corporate bonds: beating the curse of dimensionality. Applied Mathematical Finance, 26(5):387–452, 2019.

- [22] Fabien Guilbaud and Huyên Pham. Optimal high-frequency trading with limit and market orders. Quantitative Finance, 13(1):79–94, 2013.

- [23] Fabien Guilbaud and Huyên Pham. Optimal high-frequency trading in a pro rata microstructure with predictive information. Mathematical Finance, 25(3):545–575, 2015.

- [24] Thomas Ho and Hans R Stoll. Optimal dealer pricing under transactions and return uncertainty. Journal of Financial economics, 9(1):47–73, 1981.

- [25] Thomas Ho and Hans R Stoll. The dynamics of dealer markets under competition. The Journal of finance, 38(4):1053–1074, 1983.

- [26] Paul Jusselin. Optimal market making with persistent order flow. arXiv preprint arXiv:2003.05958, 2020.

- [27] Christoph Kühn and Johannes Muhle-Karbe. Optimal liquidity provision in limit order markets. Swiss Finance Inst., 2013.

- [28] Xiaofei Lu and Frédéric Abergel. Order-book modelling and market making strategies. Market Microstructure and Liquidity, 2018.

- [29] Sasha Stoikov and Mehmet Sağlam. Option market making under inventory risk. Review of Derivatives Research, 12(1):55–79, 2009.

- [30] Richard S. Sutton and Andrew G. Barto. Reinforcement Learning: An Introduction. The MIT Press, 2018.

- [31] Csaba Szepesvári. Algorithms for reinforcement learning. Synthesis lectures on artificial intelligence and machine learning 4.1:1–103, 2010.