Delay stochastic interest rate model with jump and strong convergence in Monte Carlo simulations

Abstract

In this paper, we study analytical properties of the solutions to the generalised delay Ait-Sahalia-type interest rate model with Poisson-driven jump. Since this model does not have explicit solution, we employ several new truncated Euler-Maruyama (EM) techniques to investigate finite time strong convergence theory of the numerical solutions under the local Lipschitz condition plus the Khasminskii-type condition. We justify the strong convergence result for Monte Carlo calibration and valuation of some debt and derivative instruments.

Key words: Stochastic interest rate model, delay volatility, Poisson jump, truncated EM scheme, strong convergence, Monte Carlo scheme.

1 Introduction

Despite of the popularity of several asset price stochastic models such as Black-Scholes (1973) [1], Merton (1973) [2], Vasicek (1977) [3], Dothan (1978) [4], Brennan and Schwartz (1980) [5], Cox, Ingersoll and Ross (CIR) (1985) [6] and Lewis (2000) [19], they may not be well-specified adequately to fully explain certain types of empirical phenomena in most financial markets. For instance, volatility ’skews’ and ’smiles’, and tail distribution of asset prices which have been observed empirically from various sources of financial data, may not be captured by these models (e.g., see [7, 10, 28]).

In recent times, several interesting research works have been directed towards adequate explanation of dynamical behaviours of financial variables against unexpected occurrences of these empirical phenomena. For instance, contrary to efficient market hypothesis, the delayed GBM [7], CIR [12] and CEV [13] models have been introduced as extensions of [1], [6] and [19] to incorporate volatility ’skews’ and ’smiles’ based on non-Markovian property to explain asset price dynamics. Similarly, a variety of jump diffusion models have also been proposed to explain jump behaviour or tails of distribution of asset prices. For references, see, for example, Merton (1976) [8], Lin and Yeh (1999) [9] , Kou (2002) [10] and Wu et al. (2008) [11].

Ait-Sahalia model proposed in [14] serves extensively as an indispensable tool for capturing dynamics of term structure of interest rates. This model is driven by a highly nonlinear stochastic differential equation (SDE)

| (1) |

, for any , where are positive constants and . Besides interest rates, it has also been considerably used to explain dynamics of asset price, volatility and other financial instruments. There have been several rich literature concerning with this model. For instance, Cheng (2009) in [16] studied this model and established weak convergence of EM scheme. Szpruch et al. (2011) in [15] generalised this model and established strong convergence of implicit EM method as well as preservation of positive approximate solutions of this method when a monotone condition is fulfilled. Dung (2016) in [17] derived explicit estimates for tail probabilities of solutions to the generalised form of this model. Deng et al. in [18] studied analytical properties of the generalised form of this model with Poisson-driven jump and revealed weak convergence of EM method.

While the SDE (1) enjoys significant patronage of both market participants and practitioners, it may also not be well specified to adequately explain interest rate dynamics in response to joint effects of extreme volatility and jump behaviour or information flows as observed empirically from most financial markets. This motivates the need to modify this model to help explain adequately these empirical phenomena more collectively. In modelling context, it is worthwhile to extend SDE (1) to incorporate delayed volatility function and Poisson-driven jump described by

| (2) |

on with initial data for . Here , denotes delay in , depends on with . Moreover, , , is a scalar Brownian motion and is a scalar Poisson process independent of with a scalar compensated Poisson process defined by , where is the jump intensity.

The SDDE (2) is characterised by two distinguished features. The delayed volatility function may explain volatility ’smiles’ and ’skews’ which are common in most financial markets. On the other hand, the Poisson-driven jump may account for responses of interest rates to discontinuous random effects generated in connection with unexpected catastrophic news or lack of information.

It is worth observing that the SDDE (2) is not analytically tractable and so there is a need to employ an efficient numerical scheme to estimate the exact solution. We cannot in this case employ classical explicit EM method which requires coefficients to be of linear growth (e.g., see [21]). Meanwhile, the truncated EM scheme recently developed in [23] serves as a useful explicit numerical tool for strong convergent approximation of SDEs with superlinear coefficients. In this work, we aim at investigating the finite time strong convergence of the truncated EM solutions of system of SDDE (2) under the local Lipschitz condition plus the Khasminskii-type condition. Essentially, this work extends results in [24] to cope with random jumps.

The rest of the paper is organised as follows: In section 2, we will study the existence of a unique global solution to SDDE (2) and show that the solution will always be positive. We will also establish moment bounds of the exact solution in section 2. In section 3, we will present the truncated EM approximation scheme for SDDE (2). Section 4 will be entirely devoted to explore numerical properties of the truncated EM scheme including finite time strong convergence of the truncated EM approximate solutions to the exact solution. In section 5, we will perform some numerical illustrations to support the findings. Finally, we will apply the strong convergence result within a Monte Carlo framework to value some debt and derivative instruments in section 6.

2 Analytical properties

In this section, we establish existence of uniqueness and moment bounds of the exact solution to SDDE (2). In sequel, let introduce the following mathematical notations and settings.

2.1 Mathematical preliminaries

Throughout this paper unless otherwise specified, we let be a complete probability space with filtration satisfying the usual conditions (i.e, it is increasing and right continuous while contains all -null sets), and let denote the expectation corresponding to . Let , be a scalar Brownian motion defined on the above probability space. Let be a scalar Poisson process independent of with compensated Poisson process , where is the jump intensity, also defined on the above probability space. If are real numbers, then denotes the maximum of , and denotes the minimum of . Let and . For , let denote the space of all continuous functions with the norm . For an empty set , we set . For a set , we denote its indication function by . Let the following dynamics

| (3) |

, on , denote equation of SDDE (2) such that , and , , with defined in . Let be the family of all real-valued functions defined on such that is twice continuously differentiable in and once in . For each , define the jump-diffusion operator by

| (4) |

for SDDE (3) associated with the -function , where

| (5) |

, is the diffusion operator, and are first-order partial derivatives with respect to and respectively, and , a second-order partial derivative with respect to . With the jump-diffusion operator defined, the Itô formula then yields

| (6) | ||||

almost surely. We refer the reader, for instance, to [29] for detailed coverage of (6).

2.2 Existence of nonnegative solution

Before we show existence of nonnegative solution to SDDE (3), we are required to assume the volatility function is locally Lipschitz continuous and bounded (see, e.g.,[7] for detailed accounts of these conditions). The following conditions are thus sufficient to establish existence of a unique positive global or nonexplosive solution to SDDE (3).

Assumption 2.1.

The volatility function of SDDE (3) is Borel-measurable and bounded by a positive constant , i.e.

| (7) |

.

Assumption 2.2.

Assumption 2.3.

The parameters of SDDE (3) satisfy

| (9) |

The following theorem reveals the SDDE (3) admits a pathwise-unique positive global solution on . Since SDDE (3) describes interest rate dynamics, the solution will always remain nonnegative almost surely.

Theorem 2.4.

Proof.

Since the coefficient terms of SDDE (3) are locally Lipschitz continuous in , then there exists a unique positive maximal local solution for any given initial data (10), where is the explosion time. Let be sufficiently large such that

For each integer , define the stopping time

| (11) |

Obviously, is increasing as . Set , whence almost surely. In other words, we need to show that almost surely to complete the proof. For any , define a -function by

| (12) |

Clearly as or . By Assumption 2.1, we get from the operator in (4) that

where

Since and by Assumption 2.3, we note leads and tends to for small and for large , leads and also tends to . Hence there exists a constant such that

| (13) |

So for , we derive from the Itô formula

. It then follows that

As , . This implies a.s. Also for , the Itô formula yields

and consequently,

As , we get a.s. Repeating this procedure for , we obtain by letting . This means a.s and hence a.s. The proof is now complete. ∎

2.3 Moment bound

The following lemmas show moments of the exact solution to SDDE (3) are upper bounded.

Lemma 2.5.

Proof.

Define the stopping time for every sufficiently large integer by

| (15) |

Define a function by . By Assumption 2.1, the jump-diffusion operator in (4) gives us

where

By Assumption 2.3, dominates and tends to for large . Hence we can find a constant such that

The Itô formula gives us

Applying the Fatou lemma and letting yields

and consequently,

as the required assertion in (14). ∎

Lemma 2.6.

Proof.

Let be the same as in (15). By applying (4) to , we compute

where Assumption 2.1 has been used and here, we have

By Assumption 2.3 and noting that , we observe leads and tends to for small and for large , dominates and tends to 0. Hence there exists a constant such that

We can now use the Itô formula, apply Fatou lemma and let to arrive at

and consequently the required assertion in (16). ∎

3 The truncated EM method

In this section, we present the truncated EM scheme for numerical approximation of SDDE (3). Meanwhile, we need the following assumption on the initial data which will be used later.

Assumption 3.1.

There is a pair of constant and such that for all , the initial data satisfies

| (17) |

In the sequel, we also need these lemmas below.

Lemma 3.2.

Lemma 3.3.

3.1 Numerical approximation

Before we proceed, let extend the volatility function and the jump term from to by setting and for . Apparently, Theorem 2.4 as well as conditions (7), (8), (18) and (19) are well maintained. Moreover, we need not truncate the jump term since it is of linear growth. To define the truncated EM scheme for SDDE (3), we first choose a strictly increasing continuous function such that as and

| (20) |

Denote by the inverse function of . We define a strictly decreasing function such that

| (21) |

Find such that and for . For a given step size , let us define the truncated functions

and

So for , we have

and

We easily observe that

| (22) |

That is, both truncated functions and are bounded although both and may not. The following lemma shows and maintain (19) nicely.

Lemma 3.4.

From now on, let be fixed arbitrarily and the step size be a fraction of . We define for some positive integer . Let now form the discrete-time truncated EM approximation of SDDE (3). Define for . Set for and then compute

| (24) |

for where and . Let now form two versions of the continuous-time truncated EM solutions. The first one is defined by

| (25) |

This is the continuous-time step-process on , where is the indicator function on . The other one is the continuous-time continuous process on defined conveniently by setting for while for

| (26) |

Obviously is an Itô process on satisfying Itô differential

| (27) |

For all , it is useful to see that .

4 Numerical properties

In this section, we establish moment bound and finite time strong convergence theory of the truncated EM solutions to SDDE (3).

4.1 Moment bound

To upper bound the moment of the truncated EM solution, let first define

for any , where denotes the integer part of . The following lemma shows and are close to each other in .

Lemma 4.1.

Let Assumption 2.1 hold. Then for any fixed , we have

| (28) |

and

| (29) |

for all , where and denote positive generic constants which depend only on and may change between occurrences.

Proof.

Fix any and . Then for , we derive

where Assumption 2.1 and (22) have been used and depends on . By the characteristic function’s argument (see [27]), we have

where is a positive constant independent of . We now obtain

This implies

where is independent of . We now have

which is (28), where . For , the Jensen inequality yields

which is the required assertion in (29), where . The proof is thus complete. ∎

We can now upper bound the moment of the truncated EM solution as follows.

Lemma 4.2.

Proof.

Fix any and . For , we obtain from (4), (20) and Lemma 3.4

where

Applying the Young inequality, we obtain

where . For , we note from the triangle inequality

This implies for , we obtain

where

By Lemma 4.1 and (22), we now have

| (31) |

where and , noting that and hence

Also by (22), we have

| (32) |

Do note for and , we have and then

| (33) |

So for and , we obtain from (32), Lemma 4.1, (33) and the Young’s inequality

where and . We now combine and to have

where and . Also we estimate as

where . Combining , and , we have

where and . As this holds for any , we then have

The Gronwall inequality yields

as the required assertion, where is independent of . ∎

4.2 Finite time strong convergence

We can now establish finite time strong convergence theory for the truncated EM solutions to SDDE (3). Before that, let first establish the following useful lemma.

Lemma 4.3.

Proof.

Let be the Lyapunov function in (12). Then for , the Itô formula gives us

By expansion, we obtain

Here,

is the operator (4) which is independent of with

and

By Assumption 2.3, there exists a constant such that for

Also by Lemma 3.2, we have

Meanwhile, for , we derive that

where (7), (17) and (18) have been used. Moreover, by the definition of (12), we have

where

and

Applying the mean value theorem, we obtain

Similarly, we also have

Substituting and back into , we have

We thus combine the , and to have

Therefore

where

and

By Lemma 4.1 and 4.2, we now have

where and . Hence,

| (36) |

For any , we may select sufficiently large such that

| (37) |

and sufficiently small of each step size such that

| (38) |

We can now reveal finite time strong convergence theory of the truncated EM scheme.

Lemma 4.4.

Proof.

By elementary inequality, it follows from (3) and (27) that for

where

| and | |||

By the Hölder inequality and Lemma 3.2, we have

| (41) |

Furthermore, the Hölder and Burkholder-Davis Gundy inequalities yield

where is a positive constant. For , we have . So by Assumption 3.1, Lemma 3.2 and (20), we now have

| (42) | ||||

| (43) |

Moreover, we obtain from elementary inequality

where

and

The Doob martingale inequality, martingale isometry and Lemma 3.2 give us

where is a positive constant. Moreover by the Hölder inequality and Lemma 3.2,

where Lemma 3.2 has been used. Substituting and into yields

| (44) |

We now combine (41), (42) and (44) to have

where

and

Meanwhile by elementary inequality and Lemma 4.1,

So by Lemma 4.2, we have

Noting from (21) that , we have

By the Gronwall inequality, we obtain

where with

and

Moreover, the required inequality (40) is deduced by setting . ∎

The following gives the strong convergence theory of the truncated EM scheme.

Theorem 4.5.

Proof.

We only need to prove the theorem for as for it follows from the case of and the Hölder inequality. Let , and be the same as before and set

For any arbitrarily , the Young inequality

yields

| (47) |

So for , Lemmas 2.5 and 4.2 give us

| (48) |

Also by Theorem 2.4 and Lemma 4.4,

| (49) |

Moreover, by Lemma 4.4

| (50) |

Therefore, we substitute (4.2), (49) and (50) into (4.2) to have

Given , we can select so that

| (51) |

Similarly, for any given , there exists so that for , we may select to have

| (52) |

and select such that for

| (53) |

Finally, we may select sufficiently small for such that

| (54) |

Combining (51), (52), (53) and (54), we establish

Therefore, we obtain (45) and clearly, by Lemma 4.1, also get (46) by letting . ∎

5 Numerical examples

In this section, we analyse the strong convergence result established in Theorem 4.5 by comparing the truncated Euler-Maruyama (TEM) scheme with backward Euler-Maruyama (BEM) scheme for SDDE (4) without term. It is already noted in [24] that the BEM scheme is not known to cope with term. Consider the following form of SDDE (3)

| (55) |

with initial data . Here is a sigmoid-type function defined by

| (56) |

Obviously, equation (56) meets all the conditions imposed on (see [24]). The coefficient terms and are locally Lipschitz continuous and hence fulfil Assumption 2.5. Moreover, we easily observe

where . We can now use with inverse .

5.1 Numerical results

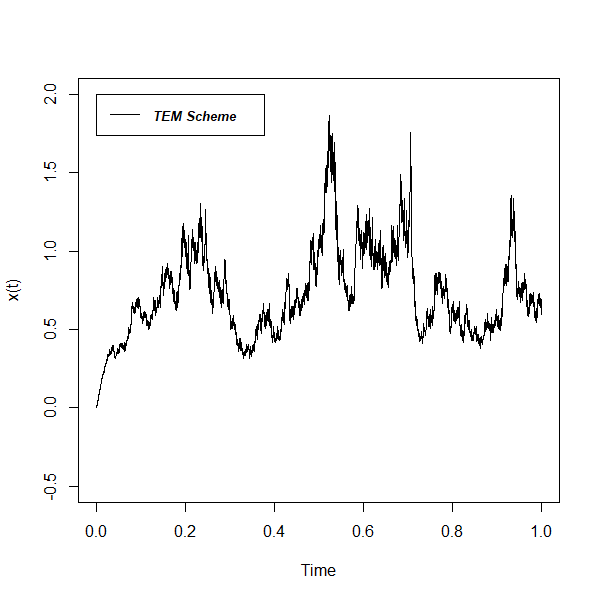

By choosing , step size and the following coefficient values in Table 1, we obtain Monte Carlo simulated sample path of to SDDE (55) in Figure 1 using the TEM scheme.

| 0.2 | 0.3 | 0.2 | 0.5 | 1 |

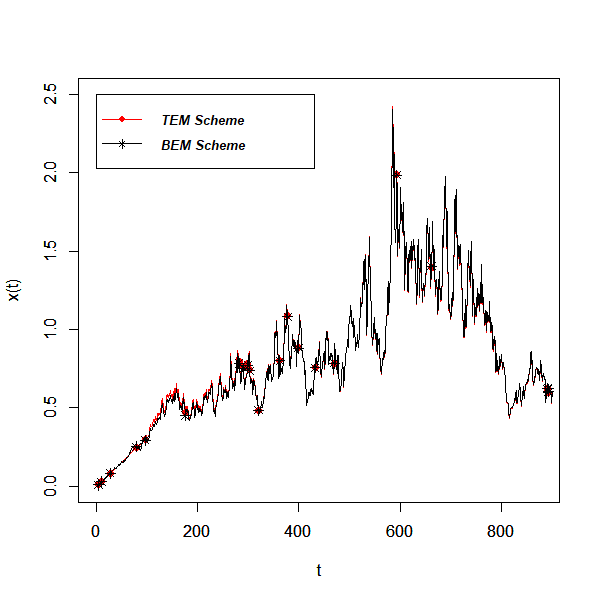

By similarly choosing , step size and the coefficient values in Table 2 below, we also obtain Monte Carlo simulated sample paths of to SDDE (55) in Figure 2 using the TEM and BEM schemes. We can clearly see the TEM scheme converges strongly to BEM scheme.

| 0.3 | 0.2 | 0.5 | 1 |

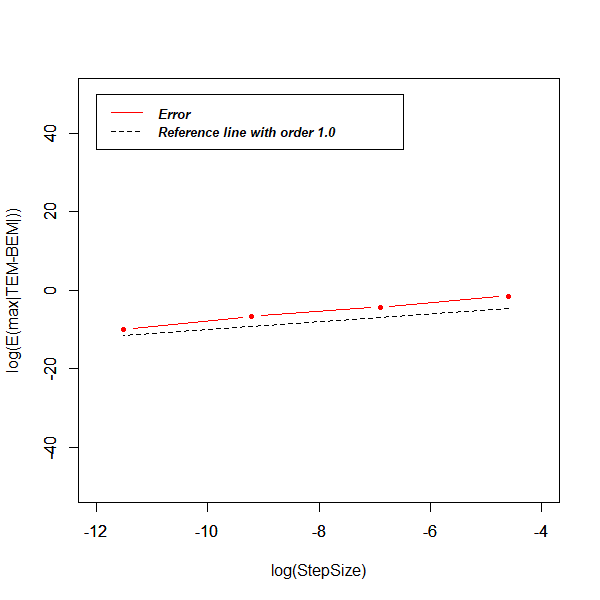

Finally, the plot of strong errors between these two numerical schemes is displayed in Figure 3 with reference line at 0. Do note this simulated result of strong errors is not yet established theoretically.

6 Financial applications

In this section, we apply Theorem 4.5 to justify numerical schemes within Monte Carlo framework that value the expected payoffs of a bond and a barrier option.

6.1 A bond

6.2 A barrier option

Acknowledgements

The Author would like to thank University of Strathclyde for the scholarship and his first PhD supervisor, Prof. Xuerong Mao.

References

- [1] Black, F. and Scholes, M., 1973. The pricing of options and corporate liabilities. Journal of political economy, 81(3), pp.637-654.

- [2] Merton, R.C., 1973. Theory of rational option pricing. Theory of Valuation, pp.229-288.

- [3] Vasicek, O., 1977. An equilibrium characterization of the term structure. Journal of financial economics, 5(2), pp.177-188.

- [4] Dothan, L.U., 1978. On the term structure of interest rates. Journal of Financial Economics, 6(1), pp.59-69.

- [5] Brennan, M.J. and Schwartz, E.S., 1980. Analyzing convertible bonds. Journal of Financial and Quantitative analysis, 15(4), pp.907-929.

- [6] Cox, J.C., Ingersoll Jr, J.E. and Ross, S.A., 2005. A theory of the term structure of interest rates. In Theory of Valuation (pp. 129-164).

- [7] Mao, X. and Sabanis, S., 2013. Delay geometric Brownian motion in financial option valuation. Stochastics An International Journal of Probability and Stochastic Processes, 85(2), pp.295-320.

- [8] Merton, R.C., 1976. Option pricing when underlying stock returns are discontinuous. Journal of financial economics, 3(1-2), pp.125-144.

- [9] Lin, B.H. and Yeh, S.K., 1999. Jump‐Diffusion Interest Rate Process: An Empirical Examination. Journal of Business Finance and Accounting, 26(7‐8), pp.967-995.

- [10] Kou, S.G., 2002. A jump-diffusion model for option pricing. Management science, 48(8), pp.1086-1101.

- [11] Wu, F., Mao, X. and Chen, K., 2008. Strong convergence of Monte Carlo simulations of the mean-reverting square root process with jump. Applied Mathematics and Computation, 206(1), pp.494-505.

- [12] Wu, F., Mao, X. and Chen, K., 2009. The Cox–Ingersoll–Ross model with delay and strong convergence of its Euler–Maruyama approximate solutions. Applied Numerical Mathematics, 59(10), pp.2641-2658.

- [13] Lee, M.K. and Kim, J.H., 2016. A delayed stochastic volatility correction to the constant elasticity of variance model. Acta Mathematicae Applicatae Sinica, English Series, 32(3), pp.611-622.

- [14] Ait-Sahalia, Y., 1996. Testing continuous-time models of the spot interest rate. The review of financial studies, 9(2), pp.385-426.

- [15] Szpruch, L., Mao, X., Higham, D.J. and Pan, J., 2011. Numerical simulation of a strongly nonlinear Ait-Sahalia-type interest rate model. BIT Numerical Mathematics, 51(2), pp.405-425.

- [16] Cheng, S.R., 2009. Highly nonlinear model in finance and convergence of Monte Carlo simulations. Journal of Mathematical Analysis and Applications, 353(2), pp.531-543.

- [17] Dung, N.T., 2016. Tail probabilities of solutions to a generalized Ait-Sahalia interest rate model. Statistics and Probability Letters, 112, pp.98-104.

- [18] Deng, S., Fei, C., Fei, W. and Mao, X., 2019. Generalized Ait-Sahalia-type interest rate model with Poisson jumps and convergence of the numerical approximation. Physica A: Statistical Mechanics and its Applications, 533, p.122057.

- [19] Lewis, A.L., 2009. Option Valuation Under Stochastic Volatility II. Finance Press, Newport Beach, CA.

- [20] Higham, D.J. and Kloeden, P.E., 2005. Numerical methods for nonlinear stochastic differential equations with jumps. Numerische Mathematik, 101(1), pp.101-119.

- [21] Mao, X., 2007. Stochastic differential equations and applications. 2nd ed. Chichester: Horwood Publishing Limited.

- [22] Higham, D.J. and Mao, X., 2005. Convergence of Monte Carlo simulations involving the mean-reverting square root process. Journal of Computational Finance, 8(3), pp.35-61.

- [23] Mao, X., 2015. The truncated Euler–Maruyama method for stochastic differential equations. Journal of Computational and Applied Mathematics, 290, pp.370-384.

- [24] Coffie, E. and Mao, X., Truncated EM numerical method for generalised Ait-Sahalia-type interest rate model with delay. Journal of Computational and Applied Mathematics, 383.

- [25] Guo, Q., Mao, X. and Yue, R., 2018. The truncated Euler–Maruyama method for stochastic differential delay equations. Numerical Algorithms, 78(2), pp.599-624.

- [26] Deng, S., Fei, W., Liu, W. and Mao, X., 2019. The truncated EM method for stochastic differential equations with Poisson jumps. Journal of Computational and Applied Mathematics, 355, pp.232-257.

- [27] Bao, J., Böttcher, B., Mao, X. and Yuan, C., 2011. Convergence rate of numerical solutions to SFDEs with jumps. Journal of Computational and Applied Mathematics, 236(2), pp.119-131.

- [28] Benth, F.E., 2003. Option theory with stochastic analysis: an introduction to mathematical finance. Berlin: Springer Science and Business Media.

- [29] Applebaum, D., 2009. Lévy processes and stochastic calculus. Cambridge university press.