On the stationary solutions

of random polymer models

and their zero-temperature limits

Abstract.

We derive stationary measures for certain zero-temperature random polymer models, which we believe are new in the case of the zero-temperature limit of the beta random polymer (that has been called the river delta model). To do this, we apply techniques developed for understanding the stationary measures of the corresponding positive-temperature random polymer models (and some deterministic integrable systems). More specifically, the article starts with a survey of results for the four basic beta-gamma models (i.e. the inverse-gamma, gamma, inverse-beta and beta random polymers), highlighting how the maps underlying the systems in question can each be reduced to one of two basic bijections, and that through an ‘independence preservation’ property, these bijections characterise the associated stationary measures. We then derive similar descriptions for the corresponding zero-temperature maps, whereby each is written in terms of one of two bijections. One issue with this picture is that, unlike in the positive-temperature case, the change of variables required is degenerate in general, and so whilst the argument yields stationary solutions, it does not provide a complete characterisation of them. On the other hand, this degeneracy does allow us to explain the appearance of atoms in the stationary measures of certain zero-temperature models. We also derive from our viewpoint various links between random polymer models, some of which recover known results, some of which are novel, and some of which lead to further questions.

Data sharing not applicable to this article as no datasets were generated or analysed during the current study.

Key words and phrases:

Detailed balance, random polymer, stationary measure, zero-temperature limit2010 Mathematics Subject Classification:

82D60 (primary), 37K60, 37L40, 60E05, 60K35, 82B231. Introduction

In the recent work [17], a general approach for identifying the spatially independent and identically distributed stationary measures of various classical discrete integrable systems, namely the discrete and ultra-discrete KdV equations, and the discrete and ultra-discrete Toda lattice, was presented. Moreover, parallels were drawn between the argument of [17] and the techniques of [7], which characterised the stationary measures of a class of random polymer models. In particular, in both [17] and [7] appeals were made to particular decompositions of the recursive maps that define the models of interest. After presenting an extended introduction to what is known in the positive-temperature random polymer context, the aim of this article is to highlight the use of similar decompositions in understanding zero-temperature limits of the models in question. Whilst the results we present were for the most part previously known (including all those relevant to the positive-temperature systems), the stationary solutions we derive for the zero-temperature limit of the beta random polymer are apparently new. We further believe that the systematic approach set out here helps clarify why particular stationary measures arise for the different random polymer models considered, and the connections between them. Indeed, in both the positive- and zero-temperature settings, each of the systems is related to one of two basic bijections (which are themselves related), and each of these is naturally connected to certain distributions via an ‘independence preservation’ property. Moreover, the appearance in atoms in the stationary measures of various zero-temperature polymer models is explained in terms of a collapse of part of the domain from the positive- to zero-temperature regime.

Let us start by introducing the central ideas of [17] in the context of two-dimensional stochastic lattice models. In the latter setting we commonly have that the input to a system is provided by an array of random variables, and the behavior of the partition function , as determined by , is the main object of interest; see Section 2 for the concrete random polymer examples that will be our primary focus. Writing and for the ‘derivative’ (in a suitable sense) of in the first- and second-coordinate directions, respectively, one then typically has a recursive relation of the form:

| (1.1) |

where for some subsets (usually intervals or discrete subsets thereof). In the ‘upper-right corner’-version of such a model, one takes independent random variables , and , and from these inputs determines the remaining variables and by applying (1.1) repeatedly. Given this structure, if there exists a triplet of probability measures on , and such that

| (1.2) |

where an expression of the form means a product of measures, then the stochastic lattice model has a stationary measure; see the discussion in [17], for example. (NB. For a measurable map and measure , we write for the push-forward of by .) Hence it is important to find such a collection of measures.

It transpires that for the random polymer models studied in [7] the map can be usefully decomposed into two maps, each with two inputs and two outputs. More precisely, one can find a bijection , where , such that can be reconstructed from and . To this end, one first defines an involution by setting

| (1.3) |

where we write . That is, can be computed by first applying to to give , and then applying to to give . If is chosen appropriately, one then finds that , i.e.

| (1.4) |

Pictorially, keeping track of the lattice variables, this situation can be represented as follows:

| (1.5) |

We will recall below explicitly the decomposition of for the random polymer models of [7]. Moreover, we note that in [17, Section 6], it was observed that if is the map arising for a certain directed polymer with site weights, then the map is that associated with the discrete Toda lattice, and, similarly, the of directed last passage percolation corresponds to the associated with the ultra-discrete Toda lattice. (Precisely, up to a simple change of variables, discrete Toda corresponds to the given by , and ultra-discrete Toda corresponds to the given by , using the notation introduced subsequently at (1.7) and (1.9).) As will become clear in what follows, these connections explain why the systems admit related stationary measures.

The advantage of the above picture is that it gives a route to understanding the stationary measures of , i.e. those satisfying (1.2), via the solutions of a certain ‘detailed balance condition’ for . In particular, we say that a quadruplet on , , and satisfies the detailed balance condition for if

| (1.6) |

This condition was called the ‘detailed balance condition for a type II model’ in [17], wherein it was shown to be equivalent to the temporal invariance in distribution of the corresponding bi-infinite dynamical system started from . Whilst this usage of the terminology detailed balance is different to the standard one for reversible Markov chains, it similarly provides, in the setting of [17], a local condition for the global invariance of a system. Notice also that the detailed balance condition of (1.6) can be seen as the aforementioned independence preservation property for the bijection . A key result in [17] is the following proposition, which shows that solutions of the detailed balance condition for precisely correspond to triplets of measures whose product is invariant under . Subsequently, applying the link between and from (1.4), one sees that invariant product measures for yield solutions of (1.2), and vice versa. Thus we have the desired connection between the detailed balance condition for and stationary measures for .

Proposition 1.1 ([17, Proposition 2.8]).

Let be a bijection, where are measurable subsets of , and define as at (1.3). For a triplet of probability measures on , and , the following three conditions are equivalent:

-

(a)

;

-

(b)

;

-

(c)

there exists a probability measure on such that the quadruplet of probability measures satisfies the detailed balance condition for .

We now proceed to become more specific in our discussion. For the random polymer models of interest in [7], as we will outline in more detail in Section 2, the maps that arise take the form

| (1.7) |

for some satisfying . One can readily check that a corresponding is given by

| (1.8) |

(Note that the choice of is not unique, but the flexibility that it admits is essentially only a change of scale in the second coordinate of its output, and the above form will be convenient for us.) Consequently, if one can characterise detailed balance solutions for the maps , then one obtains all the stationary measures of the polymer models. In fact, by scaling and symmetry, there are only essentially four choices of that are relevant in the setting of [7]:

- •

- •

-

•

, which corresponds to the inverse-beta model of [27];

- •

Moreover, after some additional rescaling, one can check that solving the detailed balance equation for the corresponding is equivalent to solving it for one of the following bijections on :

which has inverse

and the involution

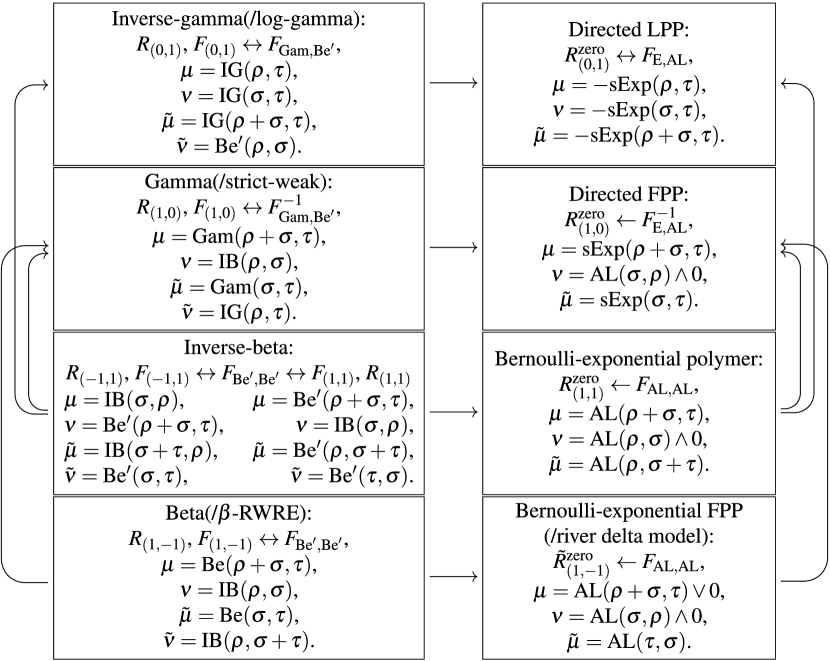

Precisely, we will explain how to relate to , to , and both and to . (See Proposition 3.1 below.) In the course of the study, it will also be convenient to consider , which is essentially equivalent to and also relates to (see Remark 3.4 for the connection between and , and [7, Lemma 4.1] and Proposition 3.1 again for the link with ). Importantly, the solutions of the detailed balance condition for both and are completely described in classical results, see Proposition 4.1 below. As indicated by the notation, the distributions appearing in these statements are either a gamma distribution or a beta prime distribution. (See Appendix A for a list of the various parametric families that appear in this article.) As a result, one is able to characterise the stationary measures for the original polymer models. We summarise the results in Figure 1; for precise claims, see Theorem 4.2 (and also [7]). As further background, we note that [8] contains an application of the stationarity property of the above polymer models to the understanding of their fluctuation exponents.

Towards describing the zero-temperature limits of the above-mentioned polymer models, we define, for each , a map by setting

Moreover, slightly abusing notation, we write . The zero-temperature limit of the map at (1.7) is then given by the piecewise linear function , as defined formally by

| (1.9) |

We highlight that whilst in this article we view the term ‘zero-temperature limit’ purely as a mathematical operation, it is naturally motivated by statistical physics considerations. Indeed, the polymer models described above will typically incorporate a temperature parameter in their definition, and the limit of (1.9) represents taking this parameter to 0 in the sense that, just as the map gives a recursion equation for the partition function in the relevant positive-temperature case, the map describes an analogous recursion for the corresponding zero-temperature model. (See Section 2 for some concrete examples of polymer models and their zero-temperature limits.) We further note that the limiting procedure described at (1.9) is commonly referred to as ultra-discretisation in the discrete integrable systems literature.

The domain upon which the limit at (1.9) is defined will vary depending on the particular choice of , and, in the case, we will make a change of scale before taking the zero-temperature limit (see Subsection 2.2 for details). For the special cases of polymer models listed above, these limits again correspond to models that have been studied hitherto. Specifically:

-

•

corresponds to directed last passage percolation (LPP) with exponential/geometric waiting times, which essentially appeared in [20];

-

•

corresponds to directed first passage percolation (FPP) with exponential/geometric waiting times, as studied in the language of queuing systems in [18];

-

•

or corresponds to the Bernoulli-exponential/geometric polymer of [28];

- •

(See [27, Sections V.B.1, V.B.2 and V.B.3] for further background on the first three models, respectively.) Unlike in the positive-temperature case, the maps in these classes can not always be decomposed as per the picture at (1.5) directly, even by taking the map to be the zero-temperature limit of . (See Remark 2.2 and the preceding discussion below.) However, by making certain changes of scale corresponding to those of the positive-temperature case, one can nonetheless identify a family of both continuous and discrete stationary measures for each by considering the detailed balance condition for one of the following bijections on :

which has inverse

and the involution

where we use the notation (and later also ). Note that and , with these zero-temperature limits being defined as at (1.9). See Proposition 3.5 for the links between maps, and Theorem 4.7 for our main result on the stationary measures of zero-temperature random polymer models, which we believe is new for the case in particular111In [6, Section 1.3], it was written that the stationary measure of Bernoulli-exponential FPP, which is the zero-temperature limit of the beta polymer, was computed in [27]. However, this seems to stem from a conflation of Bernoulli-exponential FPP and the Bernoulli-exponential polymer, which was studied in [27]. We highlight that these models are not the same; whereas the first is a zero-temperature limit of the beta polymer, the second is a zero-temperature limit of the inverse-beta polymer. Moreover, in [27], it is stressed that the beta polymer is not present in the framework of that article, and ‘somehow lives in a different class’.. (See Figure 1 again.) Similarly to the positive-temperature case, as indicated by the notation, the distributions appearing in the latter result are either an exponential(/geometric) distribution or an asymmetric Laplace(/discrete asymmetric Laplace) distribution.

Two outstanding issues with the argument of the previous paragraph are as follows. Firstly, whilst we believe the detailed balance solutions that we present for are the only ones, we do not yet have a proof of this. (For , characterisation of solutions of the detailed balance equation is classical.) Secondly, since the links between the zero-temperature polymer setting and the basic bijections and are in general not bijective, it is not possible to conclude that the stationary measures we identify for the polymer ones provide a complete characterisation of such. See Section 6 for more detailed comments in this direction.

As well as identifying the stationary measures of random polymer models, we investigate how these are related. To this end, we start by considering the connections between our basic maps, showing how each of (and its inverse), and (and its inverse) can be obtained through certain limiting operations from , see Figure 2. (Cf. The centrality of the inverse-beta model in [27, Figure 1].) Furthermore, applying the same changes of variables, we can relate (some of the continuous) solutions of the detailed balance condition for these maps. Such observations naturally translate to the maps underlying the positive- and zero-temperature random polymer models considered in this article, and in some instances transfer to convergence of the partition function of the models in question. The latter links are shown by arrows on Figure 1, and discussed in more detail in Remarks 5.6, 5.8 and 5.13. Whilst we do give a new connection between the bijection and detailed balance solutions in the beta random polymer setting and those in the inverse-gamma setting (see Propositions 5.3(d) and 5.5(d)), we highlight that there remains a question concerning the relation of the partition function of these two models (and similarly in the zero-temperature setting).

The remainder of the article is organised as follows. Section 2 contains precise definitions of the random polymer models studied in this article. In Section 3, we explain how the underlying recursion maps relate to one of the bijections , , and . In Section 4, we then apply the preceding results to obtain descriptions of stationary measures for the random polymer models. Following this, Section 5 features a discussion of various relations between the detailed balance solutions identified for the basic bijections, and between the stationary measures for the random polymer maps , as well as some remarks on connections between the partition functions of the corresponding polymer models. We conclude in Section 6 with some conjectures and problems left open by this work. As noted above, we also include an appendix in which definitions of the various parametric families appearing in the discussion are collated.

2. Polymer models

2.1. Positive-temperature versions

We start by considering a directed random polymer model with edge weights, which will naturally include a corresponding version with site weights. The key quantity of interest here will be the partition function

where , the sum is taken over up-right paths from to on , and the edge weights are defined by setting

with being an array of i.i.d. -valued random variables, and and being positive functions on . For this model, we have the following recursive equation for the partition function:

| (2.1) |

Moreover, by setting

the recursive equation at (2.1) can be rewritten as at (1.1), or more specifically,

where

Note that if , then the model reduces to a directed random polymer model with site weights, namely the partition function can be written

In this case, simplifies to

We next explain formally how the map can be decomposed as at (1.5). First, let be given by

| (2.2) |

and observe . Now, if is invertible on a suitable interval for each , then one can check that the function defined by

satisfies on a certain subset of . Consequently, we have that (1.4) holds for this choice of , i.e. . By Proposition 1.1, to find solutions of (1.2), it is thus enough to solve the detailed balance equation for .

In [7], the authors carefully study the detailed balance problem for under the conditions that , is suitably differentiable, satisfies the necessary invertibility, and some further technical assumptions on the measures. In this setting, the authors establish that there exists a solution of (1.6) only when for some such that . Note that in these cases, the maps and are given by the and appearing at (1.7) and (1.8), respectively. Moreover, in [7], the solutions of (1.6) are characterised explicitly. By making simple changes of variables, it is shown that these can be reduced to the four cases listed in the introduction, with being given by , , or . (The map is equal to .) For convenience, we summarise the maps , and the domains/co-domains that we consider in Table 1.

Remark 2.1.

The random walk in a beta-distributed random environment of [5] can also be described within the above framework. Specifically, let be i.i.d. -valued random variables. Let be the position of a random walk in a random environment given by

where is the distribution of the random walk given the environment . If we define

then one can check that

Making the change of variables and , we arrive at (2.1) with and .

2.2. Zero-temperature limits

We next consider the zero-temperature directed random polymer models with edge weights, which includes directed last/first passage percolation with site weights. In this case, the partition function is given by

with the minimum being taken over up-right paths from to on , and the weights being defined from i.i.d. random variables similarly to the previous subsection. The difference is that now we allow the latter random variables to be -valued, and we suppose and are functions on . The recursive equation for the partition function now becomes:

| (2.3) |

Moreover, by setting

the recursive equation (2.3) can be rewritten as

where

We note that if the above and are the zero-temperature limits of the and defining (i.e. analogously to (1.9), are given by limits of and for the positive temperature version of and , respectively), then the function is the zero-temperature limit of in the sense of (1.9). As noted in the introduction, the domains upon which we can do this will vary on the specific form of the functions and . In particular, amongst the special cases of of interest here, we have:

-

•

is given by taking , i.e.

-

•

is given by taking , , i.e.

-

•

is given by , , i.e.

Note that we choose to consider the zero-temperature limit of rather than the equivalent map to avoid the negative terms that appear in the latter map, since these lead to complications in defining the zero-temperature limit; in particular, one has to be more careful about the domain upon which the limit at (1.9) is defined. To deal with the same issue in the remaining case, that is , it will be convenient to make a change of variables before taking a limit. In particular, we take the zero-temperature limit of the map given by

| (2.4) |

to obtain the following:

-

•

is given by the expression for above with , , i.e.

(See (3.1) for the precise connection between and , and Remark 3.7 for discussion of a link between the zero-temperature versions of these maps.)

Now, suppose we want to decompose the maps as at (1.5) by following the argument of the previous subsection. Analogously to (2.2), one might then start by considering the map given by

so that . If was invertible on a suitable interval for each , then would satisfy and . Characterising the solutions of (1.2) for would then reduce to characterising the solutions of the detailed balance equation for . However, in the particular examples of considered here, the desired invertibility hardly holds, see Remark 2.2. To handle this issue, as is detailed in the next section, we make changes of variables to write the maps in terms of the more convenient, invertible maps and .

Remark 2.2.

With regards to the four zero-temperature polymer models considered here, the invertibility of the map only holds in general for . In this case, one can compute that

where , as defined by

| (2.5) |

is the zero-temperature limit of .

Remark 2.3.

The case when , i.e. , clearly corresponds to a directed first passage percolation model with site weights. Moreover, when , then by letting and , we have

which is a directed last passage percolation partition function that satisfies

| (2.6) |

By letting

the recursive equation (2.6) can be rewritten

where

which is essentially the same map as for the case of first passage percolation.

3. Reduction to basic bijections

As we commented in the introduction, there are four basic bijections that appear in this study: , , and . The aim of this section is to explain how the bijections , , (or ) and arising in the positive-temperature polymer models can each be transformed to one of , or by a bijective transformation of the state space. We will further present corresponding links between the zero-temperature maps , , and and the bijections , or .

3.1. Positive-temperature versions

To describe the change of scales of interest in the positive-temperature case, we introduce a number of bijections. Firstly, we let be the identity map on ; clearly this is a bijection on any subset of . Next, define by setting

We note that this is also a bijection between and , and vice versa. Moreover, let be the bijection given by

the corresponding inverse is given by

We note that satisfies . Finally, we suppose is the coordinate transposition map, i.e.

Given this notation, it is an elementary exercise to check the following proposition. In the statement of this, we write for the product of maps and , i.e. the map given by . We recall that the maps and are considered to be bijections on .

Proposition 3.1 (cf.[7]).

(a) The bijection satisfies

(b) The bijection satisfies

(c)(i) The bijection satisfies

(ii) The bijection satisfies

(d) The bijection satisfies

Remark 3.2.

Applying the relation , parts (c)(i) and (c)(ii) of the above result are readily deduced from each other.

For understanding the zero-temperature versions of the models, the following straightforward corollary of Proposition 3.1 will be useful. For establishing the result, we note that the map defined at (2.4) satisfies

| (3.1) |

on the relevant domain. Moreover, it is maybe helpful to have in mind that for bijections and whose domains and codomains are subsets of , if , where are real-valued functions defined on appropriate subsets of with a bijection and an injection, then

Corollary 3.3.

(a) The map satisfies

(b) The map satisfies

(c)(i) The map satisfies

(ii) The map satisfies

(d) The map satisfies

3.2. Zero-temperature limits

To transfer the corresponding changes of scale to the zero-temperature regime, we first observe that, by a simple calculation,

where we define the zero-temperature limit similarly to (1.9) in each case. Importantly, whilst the first and second of these maps are bijections on (or indeed between suitable subsets of ), the third map loses injectivity on the positive real axis. Moreover, for the third map, the image of the map is not an open interval, but a closed one, since . In particular, , which has as a consequence that the image under of an absolutely continuous probability measure on may have an atom. More precisely, one can check that , and further

Hence, even though is not in the image of for any , the image of includes and the inverse image of is . As we will describe in Subsection 4.2, this will have implications when it comes to characterising stationary solutions of the random polymer models of interest. Nonetheless, since the operation of composition is consistent with taking zero-temperature limits (in the sense that, when all the relevant limits are defined, ), we readily read off the following result from Corollary 3.3. Of course, it is also possible to check the relations by direct computation.

Proposition 3.5.

(a) The map satisfies

(b) The map satisfies

(c) The map satisfies

(d) The map satisfies

Remark 3.6.

4. Detailed balance solutions and stationary measures

In the probability literature, the following kind of problem is classical. Let and be independent - (or -)valued random variables such that the distribution of is non-trivial. Given a bijection from to itself (or to itself), define

For what distributions of and are and independent? Of course, one might equivalently ask: what are the non-trivial solutions of the detailed balance condition for ? Work on such questions originate in the work of Kac, who considered the case where is given by , which turns out to characterise the normal distribution [21]. (See also related discussion in [17, Subsection 8.2].) In Subsection 4.1, we recall how known results concerning the solutions of the detailed balance condition for and can be used to characterise solutions of the detailed balance conditions for , , (or ) and , and also stationary measures for the corresponding . Moreover, in Subsection 4.2, we explain how solutions of the detailed balance condition for and yield stationary measures for , , and , although we do not provide a complete characterisation of stationary measures in these zero-temperature cases. We recall that definitions of the distributions appearing in our results can be found in Appendix A.

4.1. Positive-temperature versions

We start by setting out the solutions of the detailed balance condition for and , which are direct consequences of classical results.

Proposition 4.1 ([22, 26]).

(a) The only non-trivial solutions of the detailed balance condition for the map are given by

where .

(b) The only non-trivial solutions of the detailed balance condition for are given by

where .

Proof.

The proof of the form of and in (a) is contained in [22]. By considering the characteristic function of where as on the final page of [22], the form of the distributions and is readily deduced from this. As for part (b), on transforming to by the bijection , this is equivalent to the characterisation of the beta distribution given in [26]. ∎

Combining the above result with Proposition 3.1 (noting that all the transformations in the statement of the latter result are bijections) readily yields the following. In checking this, it is useful to note the following relations between distributions:

(We do not need to use it here, but it also informative to note that .)

Theorem 4.2.

(a) The only non-trivial solutions of the detailed balance condition for are given by

(b) The only non-trivial solutions of the detailed balance condition for are given by

(c)(i) The only non-trivial solutions of the detailed balance condition for are given by

(ii) The only non-trivial solutions of the detailed balance condition for are given by

(d) The only non-trivial solutions of the detailed balance condition for are given by

To complete the discussion in the positive-temperature case we note that, by applying this result together with Proposition 1.1, one thus obtains a characterisation of the stationary measures of the maps , , (or ) and , as desired. (We recall that this was already done in [7], and point to Figure 1 for a summary.)

Remark 4.3.

We note that the names of the models are taken from what is in our notation, that is, the distribution of the random variables . To help relate our results to the literature, we recall parameterizations of that are often used (see, for example, [7], [27]).

-

•

For the inverse-gamma model, , with , :

-

•

For the gamma model, , with :

-

•

For the inverse-beta model, , with , :

or , with , :

-

•

For the beta model, , with :

Remark 4.4.

From the point of view of polymer models, as is explained in the discussion surrounding [7, Theorem 1.2], it is natural to consider with . As mathematical objects, one might also ask what transpires when this restriction on parameters is dropped. In this direction, we note that

which further implies

Thus Theorem 4.2 gives stationary measures with supported on negative values for , and , for example. As defined in this article, zero-temperature limits are not defined for functions supported on negative domains, and so this observation does not extend to the zero-temperature case.

4.2. Zero-temperature limits

In the zero-temperature setting, the analogue of Proposition 4.1 is the following. We highlight that part (b) does not provide a complete characterisation of detailed balance solutions for ; see Section 6 for a conjecture on this case.

Proposition 4.5.

(a) The only non-trivial solutions of the detailed balance condition for are given by

where and , and

where , and .

(b) Non-trivial solutions of the detailed balance condition for are given by

where , and

where and .

Proof.

The forms of and in part (a) were established in [16]. Deducing the forms of and is straightforward. For part (b), checking the claimed implication is also straightforward, and so we only sketch the proof of the continuous version of the result. Suppose for and . This joint distribution has density given by

where is a normalizing constant. Now, since the Jacobian of has absolute value 1 Lebesgue-almost-everywhere, the density of is given by

By breaking into five regions (i.e. ; ; ; ; ), it is an elementary exercise to check that the above expression is equal to

which confirms that if and , then is a solution of the detailed balance condition for , as desired. ∎

To transfer this proposition to the maps , , and , we will apply the following conclusion concerning changes of variables. Given Proposition 1.1, the result is obvious in the case where the change of variables is bijective. The purpose of including it is to clarify the implication that holds when this is not the case.

Lemma 4.6.

Let be a bijection and suppose there are functions , , such that

on . If is a quadruplet of probability measures on that satisfy the detailed balance condition for , then (1.2) holds with

Moreover, if and are all bijections, then the reverse implication is also true with .

Proof.

From Propositions 3.5 and 4.5, Lemma 4.6 and the fact that , one may read off the following conclusion concerning the stationary measures of our zero-temperature models. Note that only for do we have a complete characterisation of stationary measures, since it is only in this case that we have both a complete characterization of the basic bijection, and a bijective change of scale linking the basic bijection to the original dynamics. Whilst the solutions presented in parts (a)-(c) have essentially been presented previously (albeit without the shifted versions of the exponential/geometric distributions that appear in our result, see Remark 4.9), part (d) is apparently new.

Theorem 4.7.

Remark 4.8.

Remark 4.9.

(a) For , the following stationary solutions are presented in the literature: for ,

see [27, (V.12)] (but note there is a typo in that the distributions of and are exchanged).

(b) For , [27, (V.13)] gives the stationary solutions: for ,

(c) For , [27, (V.11)] gives the stationary solutions: for , ,

Discrete versions of these solutions are also presented in [27].

To put our approach into greater context, let us note that in identifying the stationary measures of a zero-temperature model, a common starting point is to take appropriate zero-temperature limits of the stationary measures of the corresponding positive-temperature model. In general, such an approach only identifies continuous stationary measures (cf. Proposition 5.7 below), and misses the discrete ones, which then have to be found in an ad hoc fashion. For instance, as is commented in [27], the definition of the Bernoulli-geometric polymer was found by ‘trial and error’. An advantage of our first step of relating each of the zero-temperature polymer models to one of two basic bijections, albeit non-bijectively, is that it readily allows us to read off both discrete and continuous stationary measures. For example, the expression for (and its discrete version) in Theorem 4.7(b), which is new, readily follows from Propositions 3.5 and 4.5. Indeed, putting the latter results together gives that the relevant is, in the continuous case, given as:

and, in particular, we clearly see that the atom in the distribution at 0 arises from the cut-off of the asymmetric Laplace distribution by the non-bijective map . As we discuss in the next section, in both the positive- and zero-temperature cases, the picture in terms of basic bijections also helps to clarify the connections between the stationary measures of different polymer models.

To finish this section, we further note that one can obtain solvable polymer models as limits of stochastic vertex models, such as the six vertex model and higher-spin vertex models, for which stationary versions have been studied; for background, see [1, 14, 13, 19]. Moreover, the beta polymer arises as a limit of the -Hahn Boson process, a stationary version of which is discussed in [12]. Thus, another potential route for deriving the stationary measures of polymer models is via their connections with these other models. As far as we are aware, such limits have not yet been explored systematically in the literature.

5. Relationships between models

In this section, we explore relationships between the basic bijections , , and , and also the associated detailed balance solutions. We break the discussion into three parts. Firstly, in the positive-temperature setting, we start by describing how both and can be deduced as suitable limits of , and also derive relationships between the various detailed balance solutions; see Subsection 5.1. Secondly, in Subsection 5.2, we present both bijection and detailed balance solution versions of zero-temperature limits for , and . Thirdly, in Subsection 5.3, we set out zero-temperature versions of the results of Subsection 5.1, which include links between and both and . These results are summarised in Figure 2. We also discuss how, by making suitable changes of variables, corresponding links for the random polymer models and their stationary measures can be obtained in certain cases, see Subsection 5.1.1, as well as Remarks 5.8 and 5.13. Note that the links we present essentially recover those illustrated in [27, Figure 1] (see also [28, Figure 2]), and also include a novel one between the zero temperature limits of the stationary beta and gamma random polymers (see Remark 5.13 in particular).

5.1. Relationships between positive-temperature models

For the positive-temperature versions of our basic bijections, we have the following result.

Proposition 5.1.

Uniformly on compact subsets of , it holds that

and also

Proof.

Since

the first statement is clear. Checking the second statement is similarly straightforward. ∎

Using the changes of scale in the above proposition, we have a corresponding connection between the detailed balance solutions of the bijections in question. The limits should be interpreted as those given by convergence in distribution.

Proposition 5.2.

With for some , we have

and also

Proof.

Suppose , and set . An elementary change of variables yields that the density of is given by

where is the beta function. Using that (where is the gamma function), one readily obtains that the above formula converges (uniformly on compacts) to the density of a distribution. Dealing with the other marginals is similar. ∎

To complete our discussion of the links between the positive-temperature bijections and , we explain how the preceding two statements can be used to connect their detailed balance solutions in a rigourous way. In particular, from Proposition 5.1, we have that

| (5.1) |

as , where and are bijective changes of scale on . Moreover, Proposition 5.2 tells us that if

| (5.2) |

then

| (5.3) |

where

| (5.4) |

Since from Proposition 4.1(b) we know that, for each , the measures at (5.2) solve the detailed balance condition for , one readily obtains from (5.1) and (5.3) that the measures at (5.4) solve the detailed balance condition for , thus giving an alternative proof of one of the directions of implication of Proposition 4.1(a). One may similarly use the second statement of Proposition 5.1 to connect to the detailed balance solutions for .

5.1.1. Relations between positive-temperature random polymer models

Applying the above arguments, one can further obtain a number of connections between random polymer models. Specifically, it is possible to explain how the maps describing the gamma/inverse-gamma random polymer models, and their stationary solutions, can be deduced from the maps and measures arising in the inverse-beta model. The convergence of maps in particular illuminates previous results connecting the partition functions of the models (which also follow from our conclusions). On the other hand, although it is also possible to connect the beta model to the gamma model in a way that yields convergence of the partition function, the relation we describe between the beta and inverse-gamma cases is such that we can not link the partition functions of the two models.

We start by combining Propositions 3.1 and 5.1 to deduce the following limiting results for the underlying bijections . For parts (a)-(b), we use that as (uniformly on compacts) to simplify some of the changes of variables to linear ones, and also choose between and in order to avoid the appearance of the coordinate transposition . Part (c) involves the non-linear transformation (where we recall that ) and , but somewhat remarkably (as we discuss in Remark 5.6 below), these operations fit perfectly with the invariant measures, so that we can still obtain convergence of the partition functions. Finally, in part (d), we require a second order term to obtain the relevant limit (clearly the first order term in the change of variables is degenerate); this difference seems to be a fundamental issue when it comes to linking the beta and inverse-gamma models.

Proposition 5.3.

The following limits hold uniformly on compact subsets of the domain of the limiting bijection.

(a) (Inverse-beta to inverse-gamma.)

(b) (Inverse-beta to gamma.)

(c) (Beta to gamma.)

(d) (Beta to inverse-gamma.)

where is the function taking the value everywhere.

As a simple corollary of the first two cases of the preceding result, one is able to deduce the corresponding limit for the maps . The presence of the transposition operator means that it is not possible to read off the analogous results for cases (c) and (d).

Corollary 5.4.

The following limits hold uniformly on compact subsets of the domain of the limiting map.

(a) (Inverse-beta to inverse-gamma.)

(b) (Inverse-beta to gamma.)

With respect to the changes of variables identified in Proposition 5.3, we have the following relationships between invariant measures. The proof is similar to that of Proposition 5.2 and is omitted. (The limits of measures are weak limits as .)

Proposition 5.5.

(a) (Inverse-beta to inverse-gamma.) Suppose are defined as in Theorem 4.2(c)(i) with parameters given by . It then holds that

where are defined as in Theorem 4.2(a).

(b) (Inverse-beta to gamma.) Suppose are defined as in Theorem 4.2(c)(ii) with parameters given by . It then holds that

where are defined as in Theorem 4.2(b).

(c) (Beta to gamma.) Suppose are defined as in Theorem 4.2(d) with parameters given by . It then holds that

where are defined as in Theorem 4.2(b).

(d) (Beta to inverse-gamma.) Suppose are defined as in Theorem 4.2(d) with parameters given by . It then holds that

where are defined as in Theorem 4.2(a).

Remark 5.6.

We now discuss case-by-case the implications of Proposition 5.5 for the partition functions of the random polymer models.

(a) For each , let , and be defined as in Proposition 5.5(a). Consider the stationary inverse-beta random polymer corresponding to with being i.i.d. random variables, and boundary condition being given by independent random variables and with marginals and , respectively, and . It then immediately follows from Corollary 5.4 and Proposition 5.5 that the associated partition function satisfies

in distribution as , where is the partition function of the stationary inverse-gamma model corresponding to , as defined from the limiting measures , and . We note that the stationary model with is simply a reflection in the line of the stationary inverse-beta random polymer corresponding to with

(Cf. [7, Lemma 4.1(f)].) Hence the above partition function limit, which stems from the divergence of second parameter of the inverse-beta distribution, matches that described in [27, Section IV.D.1] (see also [28]).

(b) A similar argument applies in case (b), where is the partition function of the stationary inverse-beta random polymer corresponding to and is the partition function of the stationary inverse-gamma model corresponding to . However, since in this case we only have scaling in one-direction, the appropriate form of the result is as follows:

in distribution as . Now,

and so we can see the above limit arises from the divergence of the first parameter of the inverse-beta distribution. Thus we recover the discussion of [27, Section IV.D.2] (see also [28]).

(c) Due to the non-linearity of the change of variables and the appearance of the transposition map in Proposition 5.5(c), one can not adopt the same approach to deduce that the partition function of the stationary beta random polymer converges under an associated scaling to that of the stationary gamma model. However, applying the symmetries of the distributions in question, it turns out that if are defined as in Proposition 5.5(c), i.e. with parameters , and are defined similarly with parameters , then (surprisingly to us)

where are defined as in Theorem 4.2(b) and we use the symbol to simply mean that the distributions share the same limit as . Moreover, considering the changes of variables in the left-hand sides above, one finds that

which in turn implies

| (5.5) |

In particular, it follows that

in distribution as , where is the partition function of the stationary beta random polymer corresponding to , as defined from , and , and is the partition function of the limiting stationary gamma random polymer corresponding to . The latter link between the beta and gamma models, as corresponding to the divergence of the second beta parameter, was previously observed in [5] (see [5, Remark 1.5] in particular).

(d) The relation between the beta and inverse-gamma models that is stated as Proposition 5.5(d) is apparently novel. Unlike in the previous case, however, we do not see a way to deduce from this the convergence of partition functions, if indeed this is possible.

5.2. Zero-temperature limits

Connecting positive- and zero-temperature bijections and detailed balance solutions, we have the following analogue of Propositions 5.1 and 5.2.

Proposition 5.7.

(a) It holds that

with the convergence at (1.9) holding uniformly on compact subsets of .

(b)(i) For , it holds that

(ii) For , it holds that

Proof.

As per the comments around (5.1)-(5.4), together with Proposition 4.1, the above result can be used to deduce that the limiting measures in parts (b)(i) and (b)(ii) are solutions of the detailed balance equation for and , respectively (cf. Proposition 4.5). In the same way, one can also make a statement about the detailed balance solutions of . Note that this procedure misses the discrete solutions of the zero-temperature detailed balance equations.

Remark 5.8.

Either directly or by applying Corollary 3.3, Proposition 3.5 and Proposition 5.7 (and equation (3.1)), it is possible to obtain the continuous zero-temperature random polymer stationary measures of Theorem 4.7 from the positive-temperature ones of Theorem 4.2. Although we omit details here, we note that the truncated asymmetric Laplace distribution emerges in the following way:

Similarly to Remark 5.6, the connections between maps and stationary measures also allow us to relate the partition functions of the positive-temperature models to those of the zero-temperature models, and thereby recover known zero-temperature limits for each of the inverse-gamma, gamma, inverse-beta and beta random polymers. For further background, one can find discussion of zero-temperature limits relating to the inverse-beta, the gamma, and inverse-gamma polymers in [27], and for the beta polymer in [5, Section 4].

5.3. Relationships between zero-temperature models

The results corresponding to Propositions 5.1 and 5.2 in the zero-temperature case are the following. Since the proofs of both are straightforward, they are omitted.

Proposition 5.9.

On , it holds that

and also

Proposition 5.10.

For , it holds that

Also, with for some , it holds that

Again, similarly to the comments around (5.1)-(5.4), together with Proposition 4.5(b), Propositions 5.9 and 5.10 imply that the limiting measures are solutions of the detailed balance equation for . Moreover, one can make a corresponding statement about the detailed balance solutions of . Note that this procedure misses the shifts permitted in the distributions of Proposition 4.5(a). Hence, unlike the other links shown in Figure 2, which all preserve the three distributional parameters of the detailed balance solutions in question, the limits from to or its inverse see a reduction from three to two parameters (cf. comment below Figure 1, and also [27, Sections V.B.1,2]).

5.3.1. Relations between zero-temperature random polymer models

We now consider how the discussion of Subsection 5.1.1 applies in the zero-temperature case. Firstly, in view of Corollary 5.4, one conjectures part (a) and (b) of the following statement. Moreover, from (3.1) and (5.5), one reasonably anticipates part (c). Since a direct proof of the claims is straightforward, we omit it.

Proposition 5.11.

(a) On , it holds that .

(b) On , it holds that .

(c) On , it holds that .

Towards connecting the stationary measures of the maps in question, we have the following statements. (As in the previous subsection, the limiting procedure does not yield the shifted exponential stationary solutions as limits.) Similar statements are possible for the discrete measures, but are omitted for brevity.

Proposition 5.12.

(a) For , as :

where we note that the limit measure is supported on .

(b) For , as :

where we note that the limit measure is supported on .

(c) For , as :

where we note that the limit measure is supported on .

Remark 5.13.

(a) As in Remark 5.6, the links between maps and stationary measures of Propositions 5.11 and 5.12 allow us to connect the partition functions of the models in question. We note that the divergence of parameters corresponds with the positive-temperature results discussed in Remark 5.6(a)-(c). (In case (c), is it useful to note that on , the map is equal to the linear map .) Results of a similar nature connecting the Bernoulli-exponential polymer (that is, the zero-temperature limit of the inverse-beta polymer) or its discrete counterpart, the Bernoulli-geometric polymer, to exponential/geometric FPP/LPP have previously been described in [27]. We believe the conclusion for the Bernoulli-exponential/geometric FPP (that is, the zero-temperature limit of the beta polymer) that links this to the exponential/geometric FPP model, is new. Thus we choose to describe this explicitly: let be the partition function of the zero-temperature random polymer corresponding to with being i.i.d. random variables, and boundary condition being given by independent random variables and with marginal distributions and , respectively, and , then

in distribution as , where is the partition function of the zero-temperature model corresponding to , as defined from the limiting measures , and . As in the positive-temperature case, it does not seem possible to relate the zero-temperature limits of the beta and inverse-gamma models (i.e. Bernoulli-exponential/geometric FPP and exponential/geometric LPP, respectively) in a similarly convenient way.

(b) For each of the four zero-temperature models (i.e. , , , ), it is possible to show that the continuous stationary measures arise as limits of discrete versions of the stationary measures, and it follows that the corresponding partition functions also converge (cf. [27]).

6. Open problems/conjectures

We finish by listing a number of open problems and conjectures that arise from our study.

-

(1)

As we noted in the introduction, the discrete and ultra-discrete Toda lattice equations are related to and , respectively. Thus they are also connected to and . Are there any natural discrete integrable systems linked to and ?

-

(2)

The characterisations of solutions to the detailed balance condition for the basic bijections , and are complete (recall Propositions 4.1 and 4.5(a)). We conjecture that all the non-trivial solutions to the detailed balance condition for are given in the statement of Proposition 4.5(b). We note that, amongst absolutely continuous distributions satisfying certain technical conditions, this has recently been shown to be the case in [4].

-

(3)

The characterisation of stationary solutions for the four positive-temperature random polymer models considered in this article is complete (recall Theorem 4.2). In the zero-temperature case, it is only for that we are able to make the same claim. Apart from the issue raised in the previous question, we also have the problem that the changes of scale in Proposition 3.5 are not bijective (for maps other than ). Consequently, even establishing the conjecture concerning Proposition 4.5(b) will not be enough to complete the story for , and . Whilst it is tempting to conjecture that for these models, there are no other non-trivial stationary solutions than those given in Theorem 4.7(b),(c),(d), this is apparently not the case. Indeed, [9, Lemma 2.4] yields another stationary measure for given by, for some parameters ,

where represents a Bernoulli distribution and a geometric one, that does not appear to correspond to a detailed balance solution for .

-

(4)

Related to the previous question, there are polymer models in the literature that do not fit into our framework, such as the discrete Hammersley process studied in [10]. If one is able to develop general techniques for characterising the stationary solutions of maps of the form , then it would be of interest to explore whether these apply in other settings.

-

(5)

As discussed in Section 5, connections between partition functions of random polymer models have been established in all the ways shown by the arrows on Figure 1. A notable omission here is a link between the partition functions of the beta and inverse-gamma models, in both the positive- and zero-temperature cases. (This point was also discussed in [28, Section III.B].) Even though we do not see such ourselves, we wonder whether there are any implications in this direction of the non-linear relationship between the maps and stationary measures of the two models made precise in Propositions 5.3(d) and 5.5(d).

-

(6)

A stronger form of stationarity that is known to hold for the positive-temperature beta-gamma models is ‘Burke’s property’, see [24, Theorem 3.3] for an explicit example and the discussion after [7, Definition 2.2] for a more general comment. For such models, Burke’s property can be understood as a consequence of the equivalence between the stationary measures for and those that are invariant under (i.e. Proposition 1.1). The fact that one can not express in the same way in general means that further work is required to check whether the stationary measures we present in the zero-temperature case satisfy a version of Burke’s property. Note we do know that has a characterisation as , and so in this case we can recover the Burke’s property of [2]. On the other hand, whilst we do not have such a description for , it is known that the stationary measure for of [9] nonetheless satisfies a version of Burke’s property.

-

(7)

For random polymer models, there are different notions of solvability. As well the computability of stationary measures, these include Bethe ansatz integrability and presence of the Robinson-Schensted-Knuth correspondence. A summary of what is known for some of the models considered here appears in [27, Figure 1]. One is naturally led to consider whether any of the connections between models described in this article offer insight into links between other solvability properties. Moreover, an important aspect of current research on random polymers concerns their place in the KPZ universality class, see [11] for an introduction to this area and [6] and the references therein for a description of some more recent developments regarding random polymers. It would of course be worthwhile to consider whether our results provide any further insight in this direction.

Acknowledgements

This research was supported by JSPS Grant-in-Aid for Scientific Research (B), 19H01792. The research of DC was also supported by JSPS Grant-in-Aid for Scientific Research (C), 19K03540, and the Research Institute for Mathematical Sciences, an International Joint Usage/Research Center located in Kyoto University. The authors thank Kevin Bao and Christian Noack for sharing a preliminary version of their results from [4], and Ivan Corwin and Mark Rychnovsky for helpful comments. This work was completed while MS was kindly being hosted by the Courant Institute, New York University. MS is further grateful to Ivan Corwin for arranging space to work in Columbia University during this extended visit to New York. Finally, we thank the referees who commented on earlier versions of this work, as their insightful comments helped improve the article and contributed to several of the open problems.

Appendix A Probability distributions

In the following list, we give definitions of the various probability distributions that appear within this article.

- Shifted exponential distribution:

-

For , , the shifted exponential distribution with parameters , which we denote , has density

where is a normalizing constant. We further write for the standard exponential distribution.

- Shifted scaled geometric distribution:

-

For , and , we say a random variable has shifted scaled geometric distribution with parameters , and if

where is a normalising constant; in this case we write . We further write for the scaled geometric distribution with parameters and .

- Asymmetric Laplace distribution:

-

For , the asymmetric Laplace distribution with parameters , which we denote , has density

where is a normalizing constant.

- Scaled discrete asymmetric Laplace distribution:

-

For and , we say a random variable has scaled discrete asymmetric Laplace distribution with parameters if

where is a normalizing constant; in this case we write .

- Gamma distribution:

-

For , the gamma distribution with parameters , which we denote , has density

where is a normalizing constant.

- Inverse-gamma distribution:

-

For , the inverse-gamma distribution with parameters , which we denote , has density

where is a normalizing constant.

- Beta distribution:

-

For , the beta distribution with parameters , which we denote , has density

where is a normalizing constant.

- Inverse-beta distribution:

-

For , the inverse-beta distribution with parameters , which we denote , has density

where is a normalizing constant.

- Beta prime distribution:

-

For , the beta prime distribution with parameters, which we denote , has density

where is a normalizing constant.

References

- [1] A. Aggarwal, Current fluctuations of the stationary ASEP and six-vertex model, Duke Math. J. 167 (2018), no. 2, 269–384.

- [2] M. Balázs, E. Cator, and T. Seppäläinen, Cube root fluctuations for the corner growth model associated to the exclusion process, Electron. J. Probab. 11 (2006), no. 42, 1094–1132.

- [3] M. Balázs, F. Rassoul-Agha, and T. Seppäläinen, Large deviations and wandering exponent for random walk in a dynamic beta environment, Ann. Probab. 47 (2019), no. 4, 2186–2229.

- [4] K. B. Bao and C. Noack, Characterizations of the generalized inverse Gaussian, asymmetric Laplace, and shifted (truncated) exponential laws via independence properties, preprint appears at arXiv:2107.01394, 2021.

- [5] G. Barraquand and I. Corwin, Random-walk in beta-distributed random environment, Probab. Theory Related Fields 167 (2017), no. 3-4, 1057–1116.

- [6] G. Barraquand and M. Rychnovsky, Tracy-Widom asymptotics for a river delta model, Stochastic dynamics out of equilibrium, Springer Proc. Math. Stat., vol. 282, Springer, Cham, 2019, pp. 483–522.

- [7] H. Chaumont and C. Noack, Characterizing stationary dimensional lattice polymer models, Electron. J. Probab. 23 (2018), Paper No. 38, 19.

- [8] by same author, Fluctuation exponents for stationary exactly solvable lattice polymer models via a Mellin transform framework, ALEA Lat. Am. J. Probab. Math. Stat. 15 (2018), no. 1, 509–547.

- [9] F. Ciech and N. Georgiou, A large deviation principle for last passage times in an asymmetric Bernoulli potential, preprint appears at arXiv:1810.11377, 2018.

- [10] by same author, Order of the variance in the discrete Hammersley process with boundaries, J. Stat. Phys. 176 (2019), no. 3, 591–638.

- [11] I. Corwin, The Kardar-Parisi-Zhang equation and universality class, Random Matrices Theory Appl. 1 (2012), no. 1, 1130001, 76.

- [12] by same author, The -Hahn boson process and -Hahn TASEP, Int. Math. Res. Not. IMRN (2015), no. 14, 5577–5603.

- [13] I. Corwin and L. Petrov, Stochastic higher spin vertex models on the line, Comm. Math. Phys. 343 (2016), no. 2, 651–700.

- [14] by same author, Correction to: Stochastic higher spin vertex models on the line, Comm. Math. Phys. 371 (2019), no. 1, 353–355.

- [15] I. Corwin, T. Seppäläinen, and H. Shen, The strict-weak lattice polymer, J. Stat. Phys. 160 (2015), no. 4, 1027–1053.

- [16] G. B. Crawford, Characterization of geometric and exponential distributions, Ann. Math. Statist. 37 (1966), 1790–1795.

- [17] D. A. Croydon and M. Sasada, Detailed balance and invariant measures for discrete KdV- and Toda-type systems, preprint appears at arXiv:2007.06203, 2020.

- [18] M. Draief, J. Mairesse, and N. O’Connell, Queues, stores, and tableaux, J. Appl. Probab. 42 (2005), no. 4, 1145–1167.

- [19] T. Imamura, M. Mucciconi, and T. Sasamoto, Stationary stochastic Higher Spin Six Vertex Model and -Whittaker measure, Probab. Theory Related Fields 177 (2020), no. 3-4, 923–1042.

- [20] K. Johansson, Shape fluctuations and random matrices, Comm. Math. Phys. 209 (2000), no. 2, 437–476.

- [21] M. Kac, On a characterization of the normal distribution, Amer. J. Math. 61 (1939), 726–728.

- [22] E. Lukacs, A characterization of the gamma distribution, Ann. Math. Statist. 26 (1955), 319–324.

- [23] N. O’Connell and J. Ortmann, Tracy-Widom asymptotics for a random polymer model with gamma-distributed weights, Electron. J. Probab. 20 (2015), no. 25, 18.

- [24] T. Seppäläinen, Scaling for a one-dimensional directed polymer with boundary conditions, Ann. Probab. 40 (2012), no. 1, 19–73.

- [25] by same author, Erratum to “Scaling for a one-dimensional directed polymer with boundary conditions”, Ann. Probab. 45 (2017), no. 3, 2056–2058.

- [26] V. Seshadri and J. Wesołowski, Constancy of regressions for beta distributions, Sankhyā 65 (2003), no. 2, 284–291.

- [27] T. Thiery, Stationary measures for two dual families of finite and zero temperature models of directed polymers on the square lattice, J. Stat. Phys. 165 (2016), no. 1, 44–85.

- [28] T. Thiery and P. Le Doussal, On integrable directed polymer models on the square lattice, J. Phys. A 48 (2015), no. 46, 465001, 41.