Sensitivity of Optimal Retirement Problem to Liquidity Constraints

Guodong Ding1, Daniele Marazzina1,2 1 Department of Mathematics, Politecnico di Milano

Piazza Leonardo da Vinci 32, I-20133, Milano, Italy

2 Corresponding Author, daniele.marazzina@polimi.it

Abstract:

In this work we analytically solve an optimal retirement problem, in which the agent optimally allocates the risky investment, consumption and leisure rate to maximise a gain function characterised by a power utility function of consumption and leisure, through the duality method. We impose different liquidity constraints over different time spans and conduct a sensitivity analysis to discover the effect of this kind of constraint.

We study a stochastic control problem involving the consumption-portfolio-leisure policy and the optimal stopping time of retirement. By determining the continuous and stopping regions of the corresponding optimal stopping time problem, we prove that the optimal retirement time is the first hitting time of the wealth process upward to a critical wealth boundary. We implement different liquidity constraints over different time spans, which are and separately for pre- and post-retirement periods. The numerical analysis shows that the wealth boundary triggering the retirement is decreasing to but increasing to . The additional retirement option impels the agent to consume less and invest more as the wealth approaches the retirement boundary, and this incentive becomes weaker as decreases.

The considered retirement mechanism is directly referred to [1, 2]. More precisely, [1] studied the optimal retirement model regarding the consumption-portfolio-leisure strategy, in which the leisure rate is limited to the binomial choice. [2] investigated a more complex optimization problem that endows the agent the flexibility in labour supply in the context of retirement planning. We extend their research and adopt a different utility function, a power utility function, as in [3], instead of the Constant Elasticity of Substitution (CES) function. Additionally, compared to [2], other extensions are i) the introduction of a continuous debt repayment the agent should face, ii) the different liquidity constraints before and after retirement, which is the main contribution of this work.

2 Problem Formulation

We deal with a financial market in which two kinds of investment are provided: the money market, concerning a fixed risk-free rate , and a risky asset, which dynamics is described by the stochastic differential equation , with and representing the constant drift and diffusion coefficients. represents a standard Brownian motion on the filtered probability space , and is the augmented natural filtration on . Moreover, by introducing the market price of risk as , we can define the state-price density process as following [4], where and indicate the discount process and an exponential martingale, respectively. Then we define the equivalent martingale measure by , . Based on the Girsanov Theorem, a standard Brownian motion under measure can be defined as , .

We now describe the optimization problem. The agent needs to optimally allocate the consumption , the amount of money for the risky investment and the leisure rate . The sum of labour and leisure rates equals the constant . Furthermore, denoting the retirement time as , the retirement mechanism can be elaborated as: on , i.e., the leisure rate, as the complement of labour rate, is upper bounded for keeping the employment state; and on , since the agent enjoys the entire leisure after declaring retirement. Then the dynamics of the wealth process , i.e., the state variable of the optimization, is

and are the constant debt repayment and the wage rate, respectively. The initial wealth is .

The considered optimal retirement problem is

()

in which is the subjective discount rate, and the utility is characterized by a power function

The admissible control set follows the standard definition, e.g., [5, Definition 2.1], imposing liquidity constraints: for , , and for a.s.. Notice that we must impose and to have the existence of an admissible solution, where represents the discounted value of the full debt repayment minus the maximum amount to borrow against the future labour income (in the pre-retirement period).

3 Solution of Optimization Problem

Defining , the gain function of Problem can be rewritten as the expectation of two separated terms representing the pre- and post-retirement part

where the subscript indicates that the corresponding variables and functions are related to the post-retirement problem.

The solutions of the pre- and post-retirement part are based on similar techniques, therefore in this letter we only report the solution of the post-retirement part, referring to the Online Appendix, Section A, for details. Depending on the value of , the solution of the post-retirement problem is divided into two different cases: one is , in which the liquidity constraint has no restriction on the optimization, and the other is , with the optimal solution being binded by the liquidity constraint.

Lemma 3.1.

The post-retirement value function

for , is given by:

The Legendre-Fenchel transform of , , is:

•

, , if ;

•

if .

Proof.

See the Online Appendix A for the proof and the definition of the constants and .

∎

3.1 Pre-retirement Part

Based on the dynamic programming principle, we can only consider a subset of the admissible control set of Problem , that is , in which any policy achieves the maximum of the post-retirement problem’s gain function. Hence we have

where is given in the previous lemma.

We first define an admissible control set corresponding to a fixed stopping time , with representing the set of -stopping times, as

,

and the utility maximization problem

()

Then, Problem is converted into an optimal stopping time problem, that is

Similar to the post-retirement problem, the primal optimization problem’s solution depends on the value of , which prompts us to solve it in two different cases. Before the discussion, we follow [5, Proposition 2.1] to provide the pre-retirement budget constraint, that is:

(3.1)

Additionally, we define the Legendre-Fenchel transform of by

3.1.1 Duality Approach with

Following the method from [6, Section 6], we first deduce an inequality of by introducing a Lagrange multiplier and using the budget constraint (3.1),

The inequality turns to equality if and only if the conditions

and hold.

Additionally, Lemma 3.1 implies

.

Then the following lemma shows that under the above conditions, there always exists a portfolio policy to ensure , , which implies the liquidity constraint is satisfied automatically.

Lemma 3.2.

For any given initial wealth , any fixed stopping time , any -measurable random variable with under the measure, and any given progressively measurable consumption and leisure processes , , , satisfying

,

there exists a portfolio process making , , and hold almost surely.

Moreover, the Lagrange method indicates that with introducing

and the value function of Problem can be transformed as

Defining , [6, Section 8, Theorem 8.5] shows that

holds under the condition that the function exists and it is differentiable for any . Then, the process to solve Problem is divided into two steps: the first is involved in the pure optimal stopping time problem of , and the second step mainly concerns finding the optimal Lagrange multiplier. We begin with the first step and introduce a new process, . Then can be rewritten as

We proceed with a generalized optimal stopping time problem

(3.2)

which shows that . The following lemma gives the continuous region and stopping region of the above optimal stopping time problem.

Lemma 3.3.

Considering the optimal stopping time problem (3.2) with the state variable , the continuous region is , the stopping region is , where denotes the boundary that separates and .

Straight follows, with the operator ,

the optimal stopping time problem (3.2) is equivalent to solving the free boundary problem below.

Variational Inequalities: Find a free boundary (Retirement level), and a function satisfying

(3.3)

for any , with the smooth fit conditions and .

The analytical solution of the above inequalities is presented in Online Appendix D.

Once is computed, we recover , and the value function is given by

being the initial wealth. The retirement time is the first time the process touches the barrier from above. The optimal strategies are reported at the end of the Online Appendix D.

Remark 3.1.

The optimal retirement time is the first time the process touches the lower barrier . The same can be obtained with respect to the wealth level . In fact, the optimal process is connected to the optimal wealth by the relation , being see the online appendix. The convex property of , see [4, Section 3.4, Lemma 4.3], indicates that is a decreasing function of , therefore, in this case the optimal retirement time is the first time the process touches an upper barrier .

3.1.2 Duality Approach with

Before proceeding to solve the problem, we present the following proposition to construct expectation form of the liquidity constraint related to , .

Proposition 3.1.

The liquidity constraint of the considered problem is

Considering the budget and liquidity constraints, (3.1) and (3.4), and introducing a Lagrange multiplier and a non-increasing process [6, 7], the following inequality is obtained:

which inspires us to define the dual individual’s shadow price problem

()

where is the set of non-negative, non-increasing and progressively measurable processes. Then we establish the duality between Problem and .

Theorem 3.1.

(Duality Theorem)

Suppose is the optimal solution to Problem , then and coincide with the optimal solution of Problem , and there exists

, . Here , where and are the parameters and giving the infimum.

This duality theorem allows us to link Problem with the shadow price problem through

Defining

, [6, Section 8, Theorem 8.5] indicates that the last inequality takes the equal sign with the condition that exists and is differentiable for any . Thereafter, the objective optimization problem can be divided into two parts:

We now consider the technique of [8] and insert an assumption on the process for acquiring a closed-form solution.

Assumption 3.1.

The non-increasing process is absolutely continuous with respect to . Hence, there is a non-negative process such that .

Then, by means of a new defined process , the value function of the individual’s shadow price problem can be written as

where is the control variable, and is the state variable. Introducing a generalized problem

the solution of is turned to with . We first handle the infimum part by defining

The corresponding Bellman equation is

The optimum has the following characterization,

•

and .

•

, then switches to a pure optimal stopping time problem,

which has the same form as (3.2) but applies to the interval .

Lemma 3.3 can be easily extended also in this case, therefore the optimal retirement time is the first time the process touches the lower barrier . Therefore, we need to compare the value of and , and split the discussion into two cases: the first one is , which corresponds to the case where the liquidity constraint boundary, , is lower than the retirement threshold.

Variational Inequalities assuming :

Find the free boundaries (retirement), (-wealth level), and a function satisfying

(3.5)

for any , with the smooth fit conditions

The analytical solution of the variational equation (3.5) is reported in Online Appendix E. Once and are computed, the value function and the optimal retirement decision can be recovered as in Section 3.1.1. The optimal strategies are reported at the end of the Online Appendix E.

If the first case does not admit a solution, that is, the liquidity constraint boundary is high enough (and larger than ) to make the agent declare retirement at time 0 for any admissible initial wealth, we deal with an immediate retirement, and therefore , and all the optimal strategies are the ones of the post-retirement problem.

4 Numerical Analysis

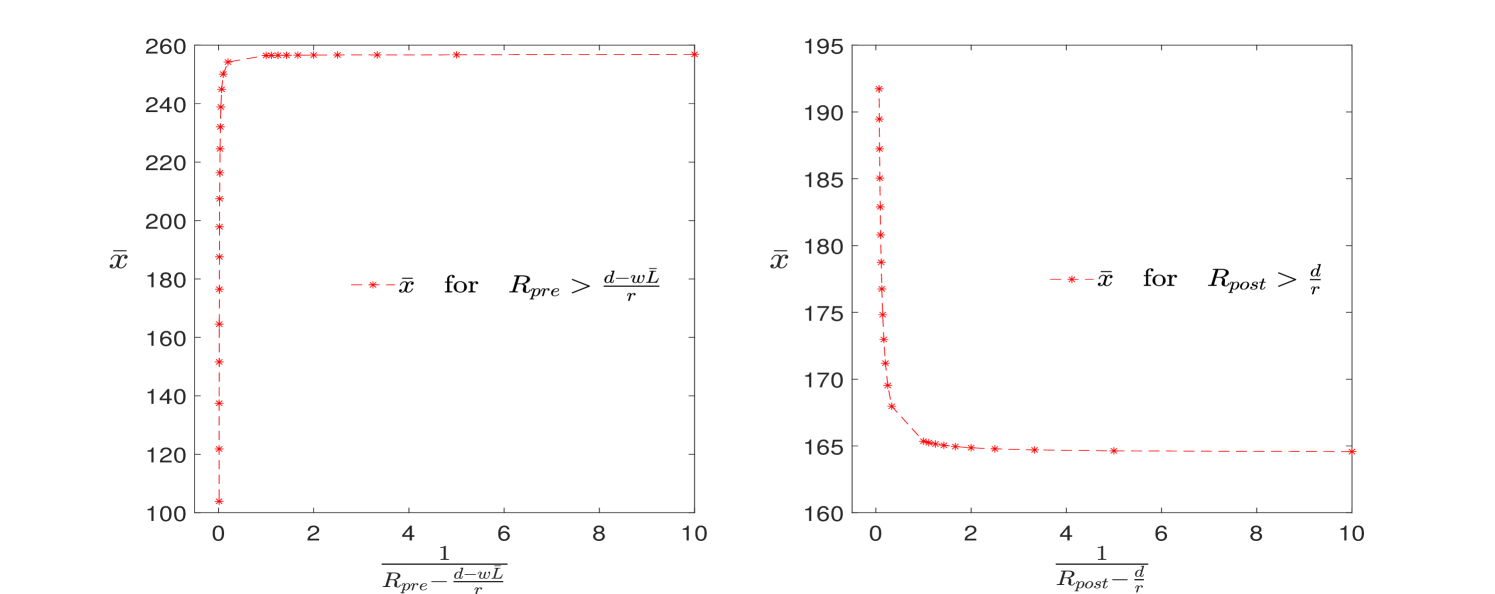

We now perform the sensitivity analysis to the liquidity constraint boundaries. All the input parameters are reported in Table 4.1. We change the values of , and keep all other input parameters consistent with Table 4.1 to discover the different convergence phenomena of retirement wealth threshold concerning the pre- and post-retirement liquidity constraints.

Table 4.1: Input Parameters

0.6

3

0.02

0.07

0.15

0.1

0.3

1.5

0

15

1

0.8

Figure 4.1 shows that the retirement wealth threshold is a decreasing function of due to the fact that the agent with higher values prefers to set a lower wealth threshold to make sure entering in retirement ahead of schedule such that getting rid of the restriction caused by . Whereas, the critical wealth level of retirement is increasing with respect to . Since the pre-retirement restriction keeps constant, a higher value of , which implies a more rigorous circumstance for the post-retirement period, impels the agent to step into retirement with a higher wealth level.

Figure 4.1: Convergence w.r.t. Liquidity Constraint Boundary of Pre- and Post-Retirement Part

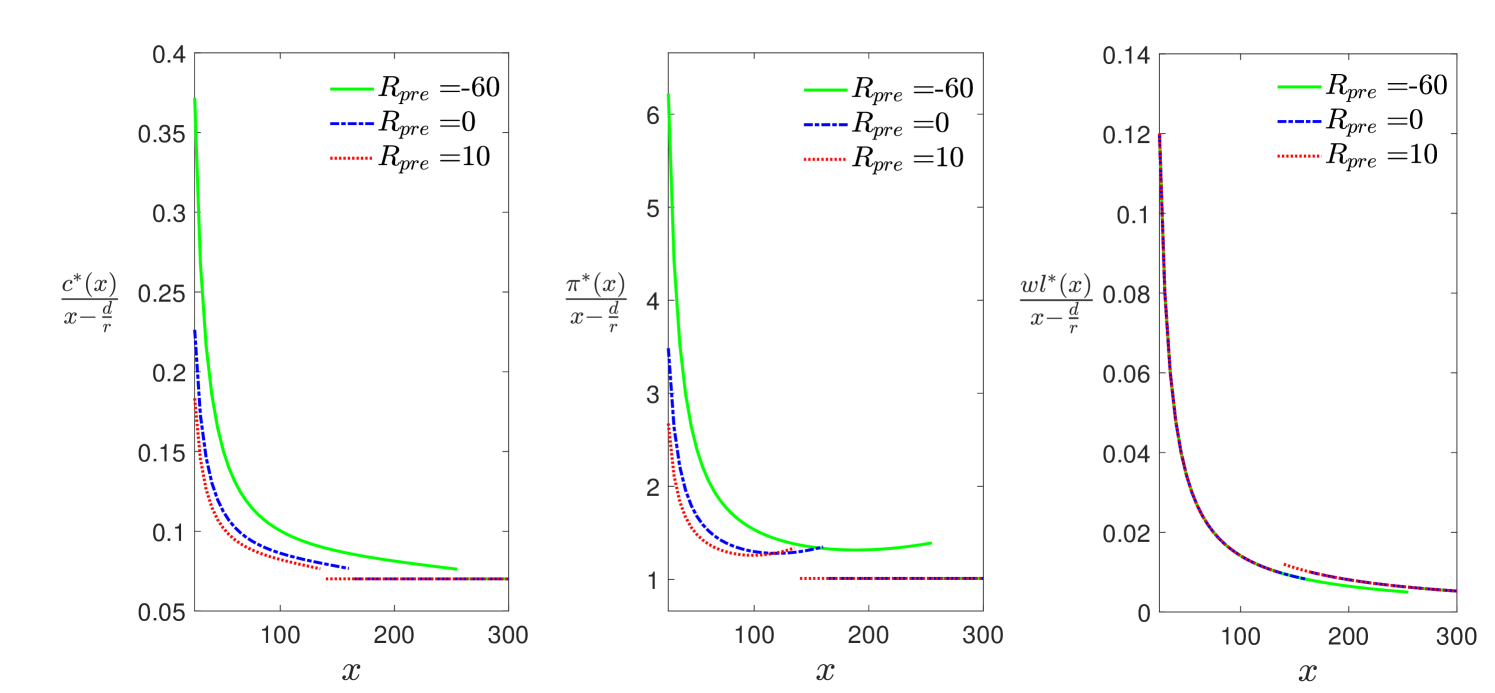

Moreover, we provide figures to illustrate the sensitivity of optimal consumption, portfolio and leisure fractions in terms of with respect to different values of and . We begin this kind of analysis fixing the value of and arranging three values to . The optimal control strategies for different cases are presented in Proposition A.3, Proposition D.1 and Proposition E.1 in the online appendix.

Figure 4.2: Optimal Control Fractions w.r.t. Liquidity Constraint Boundary of Pre-Retirement Part

In Figure 4.2, is set equal to , which implies that the post-retirement part is not restricted by the liquidity constraint. We can observe that the optimal consumption and portfolio fractions suffer a downward jump for various values. This is due to the discontinuity of the leisure rate at the retirement time, which leads to a shrinkage of labour income and reduces the resources allocated to the consumption and investment. In fact, if , , , i.e., the initial wealth is larger than the retirement threshold , the agent is facing the post-retirement region, with (full leisure). In addition, it should be noted that for different values, the jump happens at different wealth levels. As also shown in the left plot of Figure 4.1, the agent with a higher value experiences the jump at a lower wealth threshold of retirement . Moreover, since the value of keeps identical, the optimal consumption and portfolio fractions of different curves are coincident for the post-retirement part and equal to a constant, in line with the Merton classical problem.

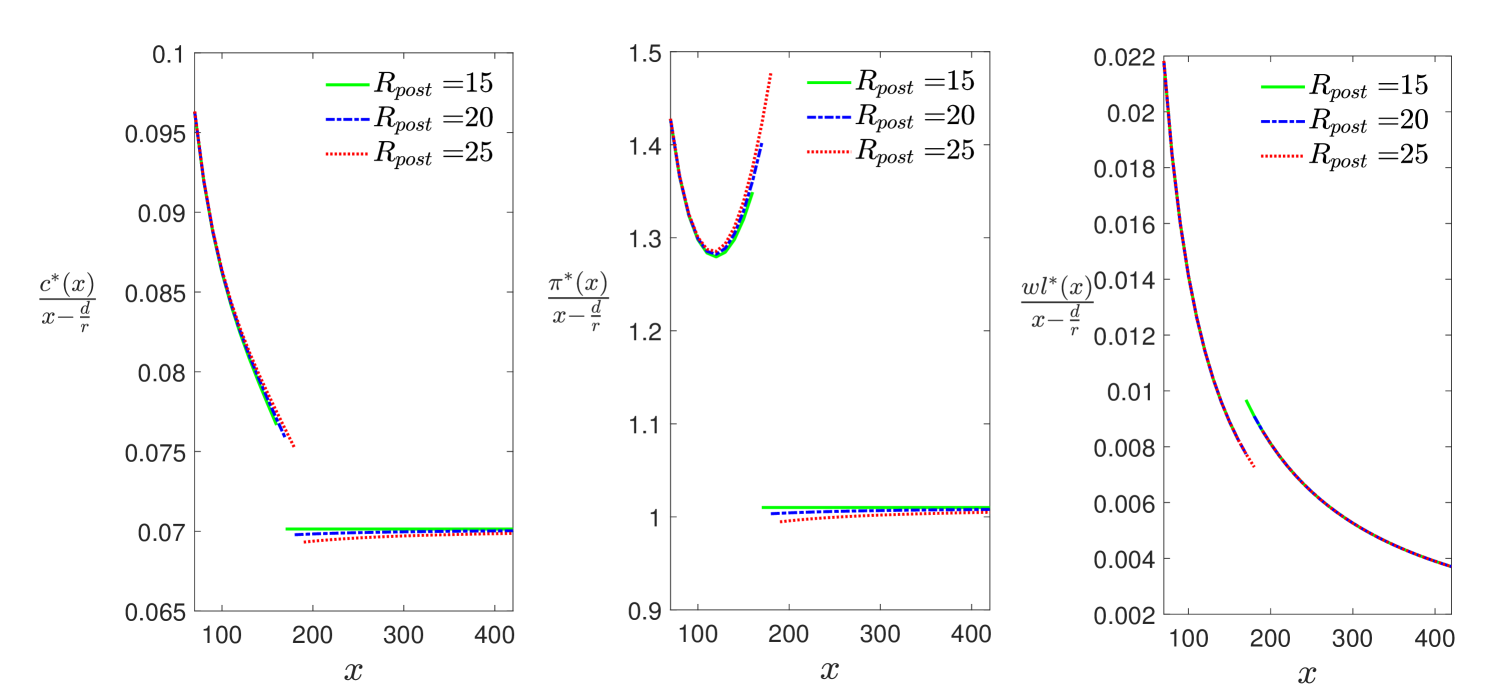

Then we conduct a similar sensitivity analysis with respect to . Figure 4.3 shows that the retirement threshold is increasing with the value of ( for , for , for ), in line with the right plot of Figure 4.1, and describes that the optimal control fractions for the post-retirement part of blue dashed and red dotted curves, whose values are greater than the boundary , i.e., the liquidity constraints impose restrictions on optimal solutions, converge to the ones of the green curve ( ) as increases. It can be explained by the fact that the liquidity constraint plays a slighter role as the wealth becomes comparably larger and imposes a weaker restriction on the admissible control set. Moreover, we also notice that a high liquidity constraint for the post-retirement part induces the agent to take a large risk (high value of ) when the retirement threshold is close.

Figure 4.3: Optimal Control Fractions w.r.t. Liquidity Constraint Boundary of Post-Retirement Part

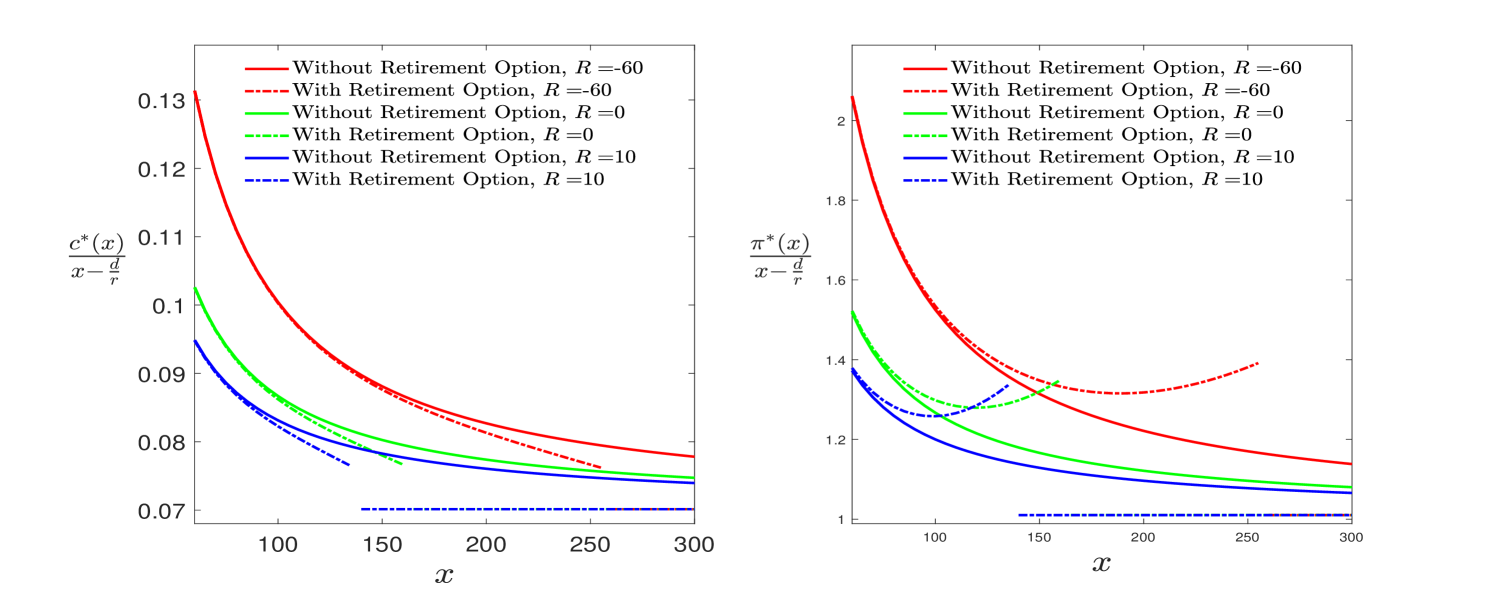

Finally, we conduct the sensitivity analysis of optimal control strategies to both the liquidity constraint boundary and the retirement option. In Figure 4.4, we fix the value of to and plot the curves of optimal consumption and portfolio fractions in terms of under different situations. The dashed lines represent the optimal control fractions of different values with retirement option, while the solid lines represent the corresponding optimal control fractions without retirement option (and therefore with fixed liquidity constraint ).111The theoretical solutions of optimal consumption-portfolio problem without retirement comes from [5, Section 5] by replacing the liquidity constraint boundary with . From all the dashed lines, we can see that the optimal consumption and portfolio fractions suffer a downward jump for various values. This is due to the discontinuity of the leisure rate at the retirement time, which leads to a shrinkage of labour income and reduces the resources allocated to the consumption and investment. Comparing the solid and dashed lines with the same colour, the agent with the additional retirement option tends to consume less and invest more in the risky asset for the motivation of arriving at the retirement wealth threshold and enjoying the full leisure rate faster. This kind of difference becomes more significant as the wealth approaches the critical level. Furthermore, the degree of this motivation is related to the liquidity constraint boundary. Observing the convexity of the pre-retirement part of different dashed lines, the optimal control fraction with a higher value takes a larger convexity, which is because stricter liquidity constraints give the agent a stronger motivation to achieve the critical wealth level to get rid of this restriction.

Figure 4.4: Optimal Control Fractions w.r.t. Liquidity Constraint Boundary and Retirement Option.

References

[1]

E. Farhi and S. Panageas, “Saving and investing for early retirement: A

theoretical analysis,” Journal of Financial Economics, vol. 83, no. 1,

pp. 87–121, 2007.

[2]

K. J. Choi, G. Shim, and Y. H. Shin, “Optimal portfolio, consumption-leisure

and retirement choice problem with CES utility,” Mathematical

Finance: An International Journal of Mathematics, Statistics and Financial

Economics, vol. 18, no. 3, pp. 445–472, 2008.

[3]

G. Shim and Y. H. Shin, “An optimal job, consumption/leisure, and investment

policy,” Operations Research Letters, vol. 42, no. 2, pp. 145–149,

2014.

[4]

I. Karatzas and S. E. Shreve, Methods of mathematical finance, vol. 39.

Springer, 1998.

[5]

G. Ding and D. Marazzina, “Effect of Labour Income on the Optimal

Bankruptcy Problem,” arXiv e-prints, p. arXiv:2106.15426, June 2021.

[6]

I. Karatzas and H. Wang, “Utility maximization with discretionary stopping,”

SIAM Journal on Control and Optimization, vol. 39, no. 1, pp. 306–329,

2000.

[7]

H. He and H. F. Pages, “Labor income, borrowing constraints, and equilibrium

asset prices,” Economic Theory, vol. 3, no. 4, pp. 663–696, 1993.

[8]

M. H. Davis and A. R. Norman, “Portfolio selection with transaction costs,”

Mathematics of operations research, vol. 15, no. 4, pp. 676–713, 1990.

Sensitivity of Optimal Retirement Problem to Liquidity Constraints - Online Appendix

Guodong Ding1, Daniele Marazzina1,2 1 Department of Mathematics, Politecnico di Milano

Piazza Leonardo da Vinci 32, I-20133, Milano, Italy

2 Corresponding Author, daniele.marazzina@polimi.it

Appendix A Post Retirement Part

Assuming , we deal with the post-retirement problem, which is an infinite-time optimization problem with two control variables, the consumption and portfolio processes. Introducing , the corresponding value function, denoted as , is

()

The admissible control set takes the compatible definition with , except that the condition for stopping time is abolished, and the condition for liquidity constraint is given by , a.s., . Then we derive the derivative function

,

which is positive and strictly decreasing and has the inverse function

. Furthermore, referring to [4, Section 3, Definition 4.2], we define the Legendre-Fenchel transform of as

, which has the explicit expression

Proposition A.1.

The infinite horizon budget constraint of the post-retirement problem is

(A.1)

Proof.

The proof can be accomplished directly by replacing in [5, Proposition 3.1] with the constant , meanwhile inserting a constant term in the integral.

∎

Depending on the value of , the solution of Problem is divided into two different cases. One is , in which the liquidity constraint has no restriction on the optimization, and the other is , with the optimal solution being binded by the liquidity constraint.

As in [4, Chapter 3, Example 9.22], the optimal wealth process under the condition is

. The optimal consumption-portfolio polices are and , with . And the value function of Problem can be obtained as

(A.2)

Remark A.1.

Analogous to the solution of the Merton problem, under the infinite time horizon, the optimal fraction invested in the risky asset in terms of the wealth minus the debt, i.e., keeps constant as , and the optimal fractional consumption takes a constant ratio as .

Hereafter, we impose a stricter liquidity constraint on the wealth process, . The following proposition provides the expectation form of the liquidity constraint, which will be accessible to deduce the duality problem subsequently.

Proposition A.2.

The infinite horizon liquidity constraint of the post-retirement problem is

Referring to [6, 7], we introduce a real number , the Lagrange multiplier, and a non-increasing process , then rewrite the post-retirement gain function as

The derivation of this inequality involves the budget constraint (A.1) and the liquidity constraint (A.3). In line with [7, Section 4], the post-retirement individual’s dual shadow price problem, labelled , can be defined as

()

where is the set of non-negative, non-increasing and progressively measurable processes. Then the duality between Problem and Problem is put forward.

Theorem A.1.

(Duality Theorem)

Suppose is the optimal solution to the dual shadow price problem , then is the optimal consumption solution to the problem . And we have the relation

, with attaining the infimum.

The Duality Theorem enables us to transform the solution of Problem to its duality, . Besides, adopting the technique from [8], the subsequent assumption should be imposed for solving the problem explicitly.

Assumption A.1.

The non-increasing process is absolutely continuous with respect to t. Hence, there exists a process such that

.

Introducing , the value function of Problem is converted into

Then we define

and observe that . The associated Bellman equation to follows

with the operator

.

From the characterization of optimum :

the Bellman equation is equivalent to

which results in the consequent modified variational inequalities: Find a free boundary , which makes -wealth level, and a function satisfying

(A.4)

for any , with the smooth fit conditions

and .

Proposition A.3.

Under the assumption , the variational inequalities (A.4) takes the solution

with

and

Furthermore, for a given initial wealth , the value function of the post-retirement problem is

(A.5)

with . Taking , the optimal wealth process follows

and the corresponding optimal consumption and portfolio strategies are

Then based on the dynamic programming principle, we can only consider a subset of the admissible control set of Problem , that is , in which any policy achieves the maximum of the post-retirement problem’s gain function. Hence, for any , we have

.

Afterwards, the whole optimization problem can be rewritten as

denoting .

Finally, we summarize the two different forms of and introduce its Legendre-Fenchel transform under the definition , following [4, Chapter 3, Definition 4.2].

Lemma A.1.

The post-retirement value function , for , is given in two separate cases, the partition being based on the value of threshold in the liquidity constraint, i.e., .

Furthermore, the Legendre-Fenchel transform of is:

For any given initial wealth , and any given progressively measurable consumption process satisfying , with standing for the set of -stopping times, there exists a portfolio process making , , holds almost surely.

Proof.

Adopting the technique of [7, Appendix, Lemma 1], we introduce and show that is uniformly integrable from the fact . Then, Dellacherie & Meyer (1982), Appendix I,111C. Dellacherie and P. Meyer, Probabilities and potential b, theory of martingales, North–Holland Mathematics Studies, 1982. indicates that there exists a Snell envelope of denoted as , which is a super-martingale under the measure and satisfies , . The Doob-Meyer Decomposition Theorem of Karatzas & Shreve (1998), Section 1.4, Theorem 4.10,222I. Karatzas and S. E. Shreve, Brownian Motion and Stochastic Calculus. Second edition. Springer-Verlag, 1998. enables us to represent the super-martingale as ,

with a uniformly integrable martingale under the measure satisfying and a strictly increasing process satisfying . Moreover, the Martingale Representation Theorem from Bjork (2009), Chapter 11, Theorem 11.2,333T. Bjork, Arbitrage theory in continuous time. Oxford university press, 2009. makes take expression ,

where is an -adapted process satisfying a.s..

Defining a new process , it can be observed that is a non-negative process with the initial wealth ,

because of

Then can be expressed with as

Applying the Itô’s formula to , we can get

Considering the portfolio strategy , the wealth process takes

which indicates that , a.s..

The non-negativity of makes clear that , a.s.,

∎

Now we turn back to the proof of Theorem A.1. Following [7, Section 4, Theorem 1], the proof mainly contains two aspects: the first part is to show the admissibility of , and the second part is to claim that is the optimal consumption strategy to Problem .

(1) We first prove that is an admissible consumption policy. Taking any stopping time from and a positive constant , we can introduce , which evidently satisfies . Then defining a function

an inequality, , is obtained from the facts that is the optimal solution of Problem and .

This inequality gives us

considering , . The decreasing property of and the Fatou’s lemma endows us with

Then indicates that .

Since can be any stopping time in the set , Lemma A.2 claims that there exists a portfolio strategy making the related wealth process satisfying , .

(2) We move to show the optimality of to Problem . The proof of Lemma A.2 indicates that for an arbitrary consumption strategy , there exists a process satisfying

(A.6)

The property a.s. gives us the subsequent inequality with any process ,

where is any time meeting . Since is bounded variational, integrating by parts gives us

Then we can take the expectation under the measure on both sides and replace Equation (A.6) to get . Then the Lebesgue’s Monotone Convergence Theorem indicates that

which holds for any admissible consumption policy and any non-negative, non-increasing process . Furthermore, it will be proved that the above inequality becomes equalized with the given and . Introducing with a small enough constant and defining a new function as

we get . Following the same argument with the first part, we apply the Fatou’s lemma to obtain separately

which claims .

Afterwards, we define a new optimization problem named as

()

The Lagrange method implies that the optimal consumption solution of the above problem, denoted as , satisfies , with as the Lagrange multiplier. The condition makes the constraint of Problem takes equality. And the condition implies that ,

which shows that is the optimal consumption policy of Problem . Finally, since the maximum utility of Problem is upper bounded by the maximum utility of , we can conclude that is also the optimal consumption solution of the primal problem .

Referring to [2, Appendix A], the function is assumed to be time-independent, that is, . Then the condition of (A.4) leads to a differential equation

(A.7)

which has the solution

and are the roots of the second-order equation

,

and satisfy

Since , the term will suffer the explosion as goes to 0. Therefore, we set the coefficient by the boundedness assumption. Considering the smooth conditions at , we can construct a two-equations system to determine the parameters and .

•

condition at :

•

condition at :

By multiplying the condition with and then adding with the condition, we have

Then, substituting the above expression into the condition, we get the exact value of as

and can also be solved by bringing into the expression ,

Moreover, the piecewise function of is completely determined as

Since is a piecewise polynomial function with smoothing merging conditions and differentiable everywhere, [6, Section 8, Theorem 8.5] indicates that keeps true for any given initial wealth . Thereafter, the closed-form of is

with , . is the critical wealth level corresponding to and follows

Moreover, the optimal wealth process takes the form

and the related optimal consumption-portfolio strategies are

the optimal portfolio strategy is obtained from [7, Section 5, Theorem 3].

The form of function is directly summarized from Equation (A.2) and (A.5), hence the proof here only focuses on the derivation of the Legendre-Fenchel transform of , which is also divided into two cases. We first extend the supremum in the definition of Legendre-Fenchel transform by enlarging the range of to , that is, , for .

Moreover, it can be proved the optimal solution attaining the supremum automatically satisfies .

(1) : From the first-order condition, we have

which entails that . Then is obviously satisfied for . Taking the above relationship back to the dual transform definition, is directly acquired after elementary calculation,

(2) : Considering the fact , it can be obtained that is the Legendre-Fenchel transform of from [4, Chapter 3, Lemma 4.3]. Then the identical forms of functions and enable us to deduce the solution as . The last step is to claim , which can be resorted to the condition .

Following [6, Section 6, Lemma 6.3], we first define a new continuous process as

where representing the expectation under measure. From the property of the random variable , this process satisfies

, a.s..

Then, making use of the condition , we get and

the above derivation involves changing the measure from the measure with the pricing kernel as to the measure with the pricing kernel as .

Meanwhile, we define a new process

Based on the fact

is a -martingale. According to the Martingale Representation Theorem from Bjork (2009), Chapter 11, Theorem 11.2, it can be expressed as , , with an -adapted process satisfying a.s.. Furthermore, adopting the portfolio strategy , the wealth process becomes

the second equality also comes from changing the measure by . We can observe that a.s. on , which concludes the proof of this lemma.

In this section we prove Lemma 3.3. Moreover, we also show that the conditions defined below, and hold true.

The proof here refers to Oksendal (2013) Section 10, Example 10.3.1.444B. Oksendal, Stochastic differential equations: an introduction with applications. Springer Science & Business Media, 2013. First of all, [5, Lemma 2.1] shows that

with , , and .

Introducing two functions

and an operator , we can determine the continuous region as

. Moreover, since

defining a new function , the continuous region can be rewritten as . Since the function takes two different forms based on the value of , we split the remaining discussion also into two cases: and .

(1) For , we have . After the basic calculation, we get

(C.1)

inherits the piecewise form from the function . Afterwards, determining the continuous region corresponds to characterize the features of the zero of . We begin claiming its convexity by the second derivative function. On the interval , we can directly determine the sign of with

. As for the interval , the corresponding second derivative function is

By solving the inequality, , we get

Since

keeps true for . Besides, considering the condition , we can conclude that the function is strictly convex on the interval . Then we move to claim : before this, a new function is introduced as

and its derivative functions are

Defining , it can be obtained that

For the second derivative, is equivalent to . Since , we have , which results in for . Then the fact indicates that for , which means is strictly increasing on the corresponding interval. Considering the relationship , we can observe the positive value of through

(C.2)

Finally, in view of the limitations

and the properties for , , we can conclude that there is a unique zero of , which is denoted as , satisfying and

. Hence, the continuous region is

.

(2) For , we have

then the function on the interval is obtained as

From and , we can deduce . Hence, the function is reduced as

Compared to Equation (C.1), we can observe that adopts the same form but applies to the different intervals. As for the interval , considering that

,

and the condition (A.7) is applicable at the point , we get

shows that is strictly convex on . Then a contradiction is constructed to prove . We first use and to derive the condition

which gives us

Assuming , we can observe the contradiction through

Then the condition implies and

Afterwards, we have

which indicates that is strictly increasing for regarding the convex property already shown. Therefore, is the unique zero of function , and satisfies . The last step is to claim under this case, which is equivalent to and discussed in two different situations. If , using the result (C.2), we have

otherwise, if , we use the increasing property of on to directly obtain .

Appendix D Calculation of Variational Inequalities (3.3)

The solution of (3.3) is split into two different cases based on the value of , namely and . Following [2, Appendix A], we take the time-separated form of function for solving the above variational inequalities explicitly.

We recall that [5, Lemma 2.1] shows that ,

with , , and . Moreover, and are the roots of the second-order equation

,

and satisfy

Case 1.

From the condition of (3.3), the following differential equation holds in the region ,

(D.1)

whose solution takes a form as

Since , for the sake of avoiding the explosion of the term as goes to , we set .

Then, the condition of (3.3) enables us to obtain

the second equality results from the condition . Furthermore, combining with the smooth condition at the point , we can construct a four-equations system to determine the parameters , , and .

•

condition at

•

condition at

•

condition at

•

condition at

Case 2.

Then we move to the second case with a different condition compared to Case 1, which mainly affects the post-retirement part and leads to a different form of . Lemma 3.1 shows that the corresponding Legendre-Fenchel transform of post-retirement value function is

Meanwhile, the dual transform involving the pre-retirement part stays the same; hence Equation from (3.3) takes the identical solution.

Afterwards, using the smooth fit conditions at and , we construct a four-equations system to achieve the unknowns, , , and .

•

condition at

•

condition at

•

condition at

•

condition at

After obtaining the closed forms of separately in Case 1 and Case 2, and given the initial wealth , the optimal Lagrange multiplier can be acquired through solving the equation , due to the fact that

holds under the differentiable property of . Then the optimal dual process of wealth follows .

Proposition D.1.

For Case 1 and Case 2, the optimal retirement time is , the optimal consumption-portfolio-leisure plan before retirement is given by

Proof.

The optimal consumption and leisure strategies come from [5, Lemma 2.1], and the optimal portfolio strategy is derived by from [7, Section 5, Theorem 3].

∎

Appendix E Calculation of Variational Inequalities (3.5)

Recalling the condition in Lemma 3.3, the problem to be solved is split into four different cases depending on the relationship between with , and with . We provide a diagram for a clear classification.

Additionally, we assume that takes the time-separated form, , as in [2, Appendix A].

Case 3. ,

We begin with the condition in (3.5), the following differential equation is obtained,

which is identical with Equation (D.1), hence shares the same solution as

(E.1)

As follows, a six-equations system is established to obtain the unknown parameters , , , , and .

•

condition at

•

condition at

•

condition at

•

condition at

•

condition at

•

condition at

Case 4. ,

The only difference between this case and the previous

one occurs in . Since , Lemma 3.1 shows that the Legendre-Fenchel transform of post-retirement value function is

As the same before, we set up a six-equation system to achieve the unknowns, , , , , and . Compared with the first case, only and conditions at change, whereas all the others keep true.

•

condition at

•

condition at

Case 5. ,

Firstly, the interval , where the condition of (3.5) holds, is considered. Also adopting the time-independent form of , the following differential equation is obtained .

The dual transform of is in the considered interval; therefore, the above differential equation takes the identical form of the one in of Case 3. The solution of is given directly from (E.1), only changing the parameters’ notations from to and to respectively,

Next, a four-equations system is set up to derive the desired parameters , , , . The same arguments with Case 3, only and conditions in changes.

•

condition at

•

condition at

•

condition at

•

condition at

Case 6. ,

We now move to Case 6. The only difference from the previous case happens on the condition , which is mainly involved in the post-retirement part; hence, the solution of the partial differential equation corresponding to Condition in (3.5) remains unchanged, that is,

Considering the smooth fit conditions at and , we construct a four-equations system to deduce the values of unknown parameters , , and .

•

condition at

•

condition at

•

condition at

•

condition at

Same argument with Case 1 and Case 2 in Appendix D, given the initial wealth and solving , we can obtain the optimal Lagrange multiplier and then the optimal process .

Proposition E.1.

Under the condition , corresponding to Case 3 and Case 4, the optimal consumption-portfolio-leisure plan before retirement is given by

Meanwhile, under the condition , corresponding to Case 5 and Case 6, the optimal consumption-portfolio-leisure plan before retirement is given by